SK Hynix brings a $29 billion AI memory test to Wall Street

SK Hynix’s ADR is a vote of confidence in AI memory demand, but also a major test of whether global investors can absorb another $29 billion of fresh AI supply.

The company has earned its place at the table through HBM leadership, Nvidia exposure and record earnings, not through narrative alone.

The risk is not that demand suddenly disappears tomorrow; it is that investors begin treating cyclical capacity expansion as permanent scarcity.

In a market already financing SpaceX, hyperscaler capex and potentially more AI IPOs, the next marginal buyer may matter more than the next impressive earnings print.

$29 billion AI memory test

The AI trade has spent the past year acting like a crowded theatre with only one exit sign, and now SK Hynix is asking investors to make room for another $29.4 billion worth of seats.

The South Korean memory champion is preparing a landmark US ADR listing, expected to begin trading on July 10 under the ticker SKHY, in what would rank among the three largest first-time share sales on record depending on the exchange rate. That puts it in the same rarified air as Saudi Aramco’s 2019 flotation and comes only weeks after SpaceX absorbed an enormous share of the market’s appetite for blockbuster technology issuance.

From the company’s perspective, the timing makes perfect sense. SK Hynix has become one of the central toll collectors on the AI highway, supplying high-bandwidth memory to Nvidia and riding the shift from conventional memory cycles toward the much tighter, more specialized HBM market. Its Seoul-listed shares have risen roughly 850% over the past 12 months, pushing its market value beyond $1 trillion, while first-quarter operating profit hit a record 37.61 trillion won and sales nearly tripled to 52.58 trillion won.

This is not simply a story about a company selling stock into strength. The proceeds are earmarked for additional manufacturing capacity and EUV lithography equipment, the industrial machinery required to keep feeding the AI buildout. In that sense, the offering is another reminder that the AI boom is no longer confined to software promises and data-centre sketches. It is increasingly becoming a capital-expenditure arms race, where the winners need to spend heavily just to remain winners.

SK Hynix’s rise is also a sharp reversal of fortune. The company emerged from the wreckage of South Korea’s post-Asian-crisis restructuring, survived years of losses and failed ownership discussions, and eventually found a lifeline when SK Group acquired it in 2011. Its early embrace of HBM proved to be the decisive turn. While Samsung was slower to respond, SK Hynix captured the lead in the most valuable corner of the memory market, holding 57% of global HBM revenue share in the fourth quarter of 2025, according to Counterpoint Research.

That leadership has helped change the way investors view memory. For decades, the sector was treated as one of technology’s most reliable boom-and-bust machines, rising with PC and smartphone demand before collapsing under the weight of too much capacity. AI has encouraged investors to believe that this time the cycle has acquired a structural floor. The evidence is not imaginary: supply remains tight, Korean companies dominate the market, and demand from AI accelerators is outstripping what producers can currently deliver.

But the market is beginning to ask a different question. Not whether demand is strong today, but how much of tomorrow’s demand has already been pulled forward and priced in.

That is where this listing becomes more than a corporate-finance event. It is a test of whether investors still have the balance sheet, appetite and patience to fund the next leg of the AI capital cycle. SpaceX was reportedly heavily oversubscribed. Alphabet is planning to raise $85 billion for its own AI ambitions. Anthropic and OpenAI may also come to market this year. The queue outside the capital markets is getting longer, and every new issuance asks whether the same pool of buyers can keep filling the bucket without eventually sloshing water over the side.

The volatility in semiconductor stocks suggests investors are already wrestling with that question. The Philadelphia Semiconductor Index fell 7.9% in one session this week and has recorded daily moves of more than 5% nine times over the past month. Micron, SanDisk, Western Digital and Seagate have all produced extraordinary gains this year, but those gains have come with the sort of air pockets usually seen when momentum becomes both powerful and fragile.

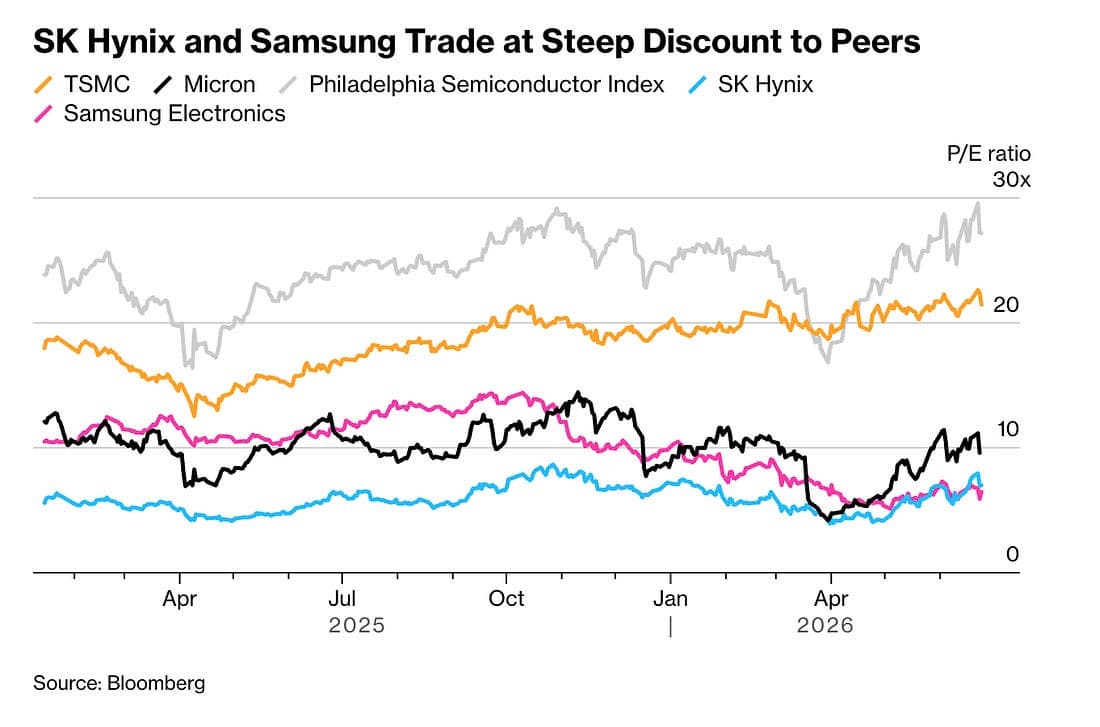

SK Hynix itself sits right at the centre of that tension. A US ADR could broaden its investor base, improve liquidity and potentially narrow the valuation gap with global peers, particularly given the success of TSMC’s US-listed shares. Yet the same listing also places a fresh supply of AI exposure into a market already debating whether the sector’s best outcomes are now consensus rather than surprise.

The company’s demand picture remains formidable. HBM shortages are expected to persist for years, and the expansion of AI computing requires far more advanced memory than the old PC and handset cycles ever did. But memory remains memory. It is a business where extraordinary profitability eventually attracts capacity, where customers eventually question returns, and where the market often realises too late that the cycle did not disappear; it merely learned how to wear a more expensive suit.

For now, SK Hynix is selling a powerful story backed by real earnings, real shortages and real technological leadership. The more uncomfortable question is whether Wall Street is buying future scarcity, or simply paying top dollar for proof that scarcity existed yesterday.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.