Nasdaq 100 (USTEC) outlook for July: AI earnings season to test momentum at key resistance

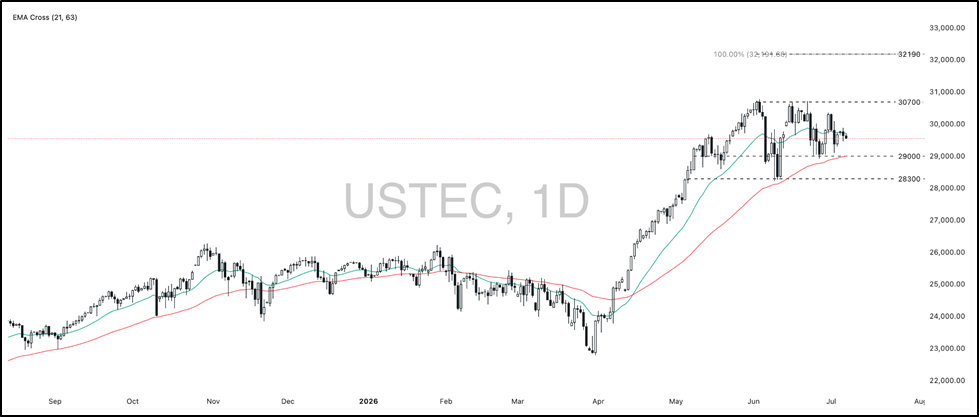

After surging above 30,000 for the first time earlier this year, the Nasdaq 100 enters July in a more complex position. The index retreated from its June highs near 29,500 as a hawkish FOMC and concerns over AI capex sustainability triggered a broad semiconductor selloff. Heading into July, the index faces a key test of whether the AI-driven bull market can hold or give way.

The macro backdrop: Fed hawkishness versus softening labor data

The recent FOMC delivered a notably hawkish signal, projecting a rate hike before year-end and the median dot-plot jumping to 3.8% from 3.4%. Fed Chair Warsh has since maintained a cautious tone, stressing data dependency and keeping the July meeting guidance deliberately vague.

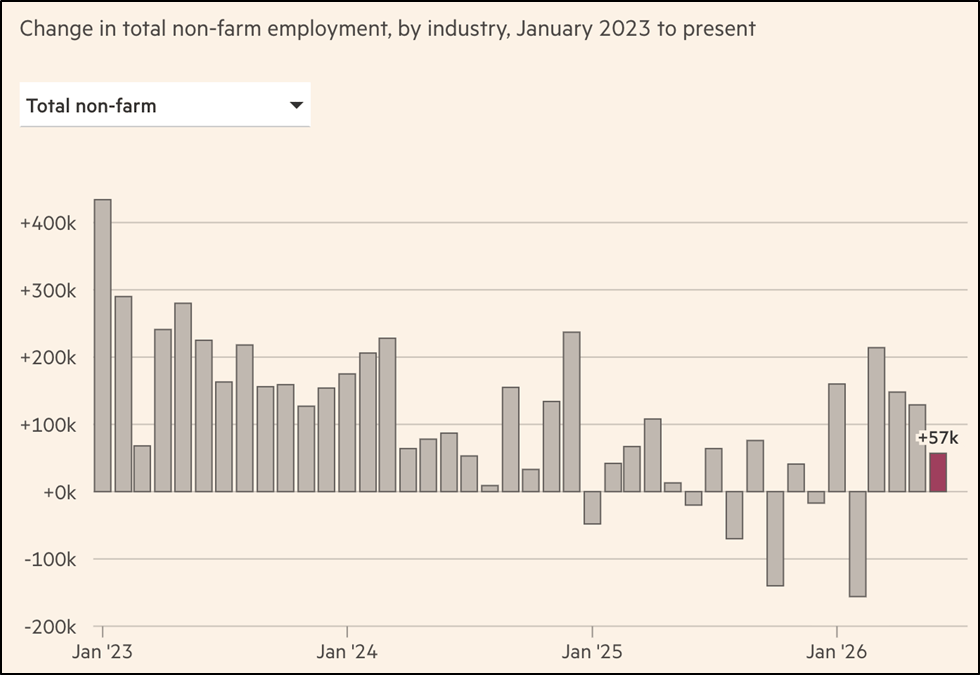

However, the June NFP report offered some relief. Payrolls came in at just 57k, well below the consensus of 115k, with prior months revised down by a combined 74k. While the Unemployment Rate decreased to 4.2%, this reflected a sharp drop in labor force participation rather than genuine labor market strength. Markets interpreted the print as softening the case for a near-term hike, which provided brief relief for rate-sensitive tech stocks.

July’s direction hinges on whether incoming inflation data, particularly the June CPI and PCE prints, reinforces or undermines the hawkish Fed narrative. A softer reading would likely give the index room to push higher, or a hotter print could reignite rate hike fears and pressure the index.

Source: FT, accessed on 02 Jun 2026

AI capex concerns: The emerging headwind

The more pointed concern is whether AI infrastructure spending has outpaced revenue. Meta Platform's (META) plan to sell excess compute capacity as a cloud service suggests some hyperscalers may already be sitting on more capacity than they need, while Microsoft (MSFT) and Apple (AAPL) passing surging memory costs onto consumers points to margin pressure spreading beyond chipmakers. With capex at several names now exceeding earnings, the debt-funded buildout narrative is gaining traction, and the Philadelphia Semiconductor Index trading 65% above its 200-day moving average, the first time since 2000, gives short sellers a compelling case. Hyperscaler stocks have already begun to underperform the broader market, suggesting the pace of AI-driven gains may be peaking rather than accelerating.

The 2Q earnings season: What to watch

July's primary driver for the Nasdaq 100 will be the 2Q earnings season. The key hyperscaler reports are clustered between late Jul and late Aug: Apple (AAPL) on 30 Jul, Microsoft (MSFT) on 28 Jul, Amazon (AMZN) on 30 Jul, and Alphabet (GOOGL) around 28 Jul, with Nvidia (NVDA) reporting on 26 Aug. If these results confirm the demand dynamics seen in Micron's blowout 3Q earnings, buying pressure in the index could remain relevant over the medium term.

Conversely, any sign that AI revenue conversion is lagging behind infrastructure spending could trigger a broader reassessment of valuations at current levels, particularly given the index is trading at elevated multiples.

Outlook

The index looks set for a volatile July, with direction hinging on whether cooling inflation gives the Fed room to step back from its hawkish stance. Strong hyperscaler earnings could extend the rally toward 30,700, but any disappointment at current multiples would likely accelerate the rotation already underway into cyclicals and blue-chips.

Author

Inki Cho

Exness

Bachelor’s in Business Management & Financial Engineering Master’s in Finance & Investment Management Certified Financial Planner (CFP) Capital Market and Securities Analyst (CMSA) Risk Management Specialist – New York Institute o