Is SpaceX worth $1.75 trillion?

The most interesting aspect of this IPO may not be what SpaceX has built. It is the fact that two rational, informed traders study the same prospectus and arrive at valuations nearly a trillion dollars apart. That tension is the story. Because nobody can agree whether it is visionary or delusional, and the gap between those two positions is measured in hundreds of billions of dollars.

What the prospectus actually reveals

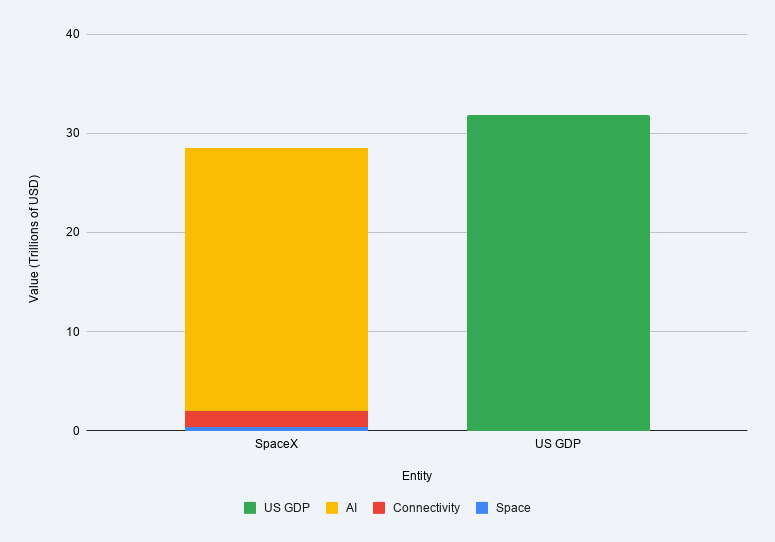

SpaceX declares it has identified the largest actionable Total Addressable Market (TAM) in human history and then quantifies it at $28.5 trillion.

The chart tells you everything about how SpaceX wants to be seen:

- Space (launch, satellites, exploration): $370 billion ~ 1.30%.

- Connectivity (Starlink broadband + mobile): $1.6 trillion ~ 5.62%.

- AI (infrastructure, consumer, advertising, enterprise): $26.5 trillion ~ 93.08%.

The internal composition of that TAM is where it gets truly audacious. Of the $28.5 trillion total, $26.5 trillion nearly 90% of the entire figure is attributed to xAi alone. Not rockets. Not Starlink. A category SpaceX did not compete in until it absorbed xAI six months ago.

Now here is where the GDP comparison becomes the most useful analytical lens available. $28.5 trillion is almost exactly the annual GDP of the United States, the largest economy on Earth, representing roughly 25% of all global economic output. Put differently, SpaceX is claiming it has identified a market opportunity equal in size to every good and service produced by 335 million Americans in an entire year. Global GDP sits at approximately $110 trillion. SpaceX's claimed TAM represents roughly 26% of the entire world's annual economic output, and that is excluding China and Russia.

The TAM is not the problem. TAMs are always aspirational. The problem is the implied capture rate baked into the IPO price and whether a company that generated $18.7 billion in total revenue last year deserves to be priced as though it has already won a war it has not yet entered.

This comparison is not just an interesting bar chart. It is a diagnostic tool for intellectual honesty.

Understanding SpaceX’s business structure

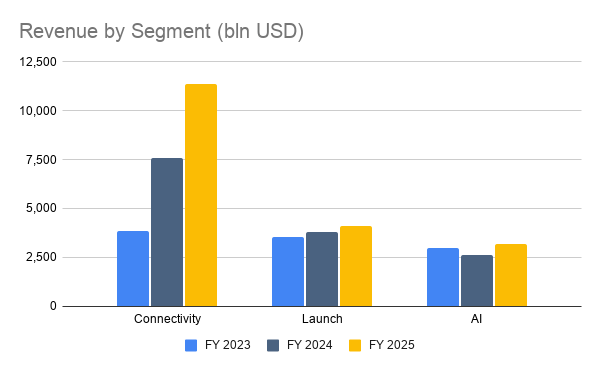

Following the merger with xAI, the company operates across three core segments: Connectivity (Starlink), Launch, and AI.

Starlink/connectivity: The core high-margin cash engine

Financial performance: Generated $11.4 billion in 2025 revenue, accounting for 61.9% of the company's total top-line performance. It has successfully captured a massive 10.3 million subscriber base spanning 164 countries.

Profitability: Delivered a stellar segment-level operating income of $4.4 billion at an approximate 63% EBITDA margin. It stands as SpaceX's sole profitable division after clearing its capital-intensive deployment phase.

Competitive moat: Operates as a software-style global infrastructure monopoly with an unreplicable fleet of 9,600+ low-Earth orbit (LEO) satellites. This establishes an order-of-magnitude lead over emerging competitors like Amazon's Kuiper (~500 satellites) and OneWeb (~650 satellites).

Launch services: Starship development driving asymmetric upside

Financial performance: Contributes approximately 22% of total top-line revenue, posting over $4 billion in 2025.

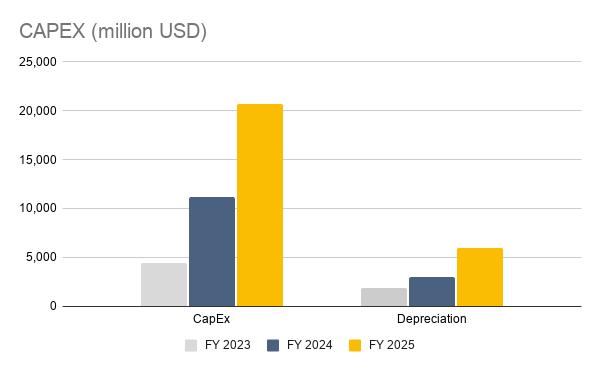

Capital constraints: The division is heavily exposed to a capital-intensive investment phase, posting a $662 million operating loss in 1Q2026 with cumulative Starship development spend exceeding $15 billion.

Market dominance: The Falcon 9 continues its run as the world's most reliable and frequently launched vehicle, executing approximately 161 launches in 2025 compared to competitors such as Rocket Lab and Blue Origin with only 18 and 11 launches, respectively

The disruption ultimate goal: If Starship successfully achieves its target cost structure to reduce launch costs to ~$100/kg (down from the current ~$1,500/kg), the technology will render every existing launch vehicle commercially obsolete.

Artificial Intelligence (xAI): The high-beta infrastructure pivot

Financial performance: Recorded $818 million in Q1 2026 revenue and $3.2 trillion in 2025, but remains locked in a high cash-burn phase.

Current operational losses: Posted a staggering $2.47 billion operating loss in Q1 2026, acting as the primary driver behind SpaceX’s consolidated red ink.

Monetization & "picks and shovels" model: Rather than competing directly with entrenched consumer AI rivals, the segment prioritizes industry collaboration through an infrastructure leasing model. This is anchored by a disclosed $1.25 billion/month compute contract with Anthropic ($15 billion annually), establishing a clear path toward near-term profitability.

Future catalyst: The segment aims to develop space-based orbital AI data centers, providing a definitive solution to the intense power consumption and heat dissipation bottlenecks currently facing ground-based tech infrastructure.

The bull case: Three compounding speculation, each explosive on its own

Starlink’s software-like hyper-monetization: Boasting an incredible 63% EBITDA margin, Starlink functions more like a high-margin SaaS giant than a telecom utility. As it aggressively scales from residential users to high-ARPU enterprise, maritime, aviation, and direct-to-cell markets, it will unlock an unstoppable, recurring cash fountain to fund the rest of the ecosystem.

Starship’s dominance of space logistics: Achieving a cost structure of $100/kg will give SpaceX absolute pricing power over the global space economy. This is the ultimate asymmetric upside in the prospectus, allowing SpaceX to launch its own massive constellations and heavy orbital infrastructure at near-zero internal cost while forcing traditional aerospace entities into obsolescence.

Space-based AI centers dominate the next tech wave: The $15 billion annual Anthropic contract proves that xAI’s true value lies in infrastructure provision rather than consumer apps. By moving supercomputers into low-Earth orbit, SpaceX offers a definitive solution to Earth's power grid shortages and heat dissipation bottlenecks, unlocking a Total Addressable Market (TAM) valued at $26.5 trillion for orbital AI computing.

The bear case: Brilliant business, mission impossible

Stretched multiples and inflated TAM projections: The aggregate $1.75 trillion valuation implies a standalone valuation of $600 billion to $900 billion for the AI segment. Underwriters allocating $26.5 trillion of the $28.5 trillion total TAM to AI is classic IPO marketing fluff. In reality, xAI's consumer vertical heavily lags behind incumbents, and the mảng is bleeding cash with a $4.3 billion net loss in Q1 2026 alone.

Endless capex black holes and cash burn vulnerability: To maintain its lead, SpaceX must remain a hyper-aggressive cash burner. Starlink’s hard-earned profits are currently being entirely consumed by AI losses and Starship’s multi-billion dollar development cycles. If global tech capital expenditure or the AI arms race cools down, SpaceX's heavily leveraged financial structure will face severe post-IPO strains.

Thermal physics bottlenecks and governance red flags: Technically, operating high-density data centers in a vacuum environment faces unforgiving radiative heat dissipation hurdles that lack large-scale commercial precedent. Governance-wise, Elon Musk holding over 85% of voting rights with only ~46% equity is a major corporate governance warning sign for institutional funds demanding standard checks and balances.

The bull and bear debate is not a sign of market confusion. It is a sign that SpaceX is genuinely, structurally unlike anything that has ever been brought to public markets before. For traders who understand asymmetry, that same ambiguity is the setup.

The most interesting aspect of SpaceX may not be the rockets, the satellites, or even the AI ambition. It may be the company has managed to build something so complex, so multi-layered, and so dependent on one man's continued execution.

In the history of public markets, that has never happened before listing day. It is happening now.

Author

Van Ha Trinh

Exness

Bachelor’s in Finance & Banking – Ho Chi Minh University of Banking Passed CFA Level II – CFA Institute CFA Research Challenge participant Over 10 years of experience across banking, brokerage, and analysis