ECB Recap: Between rising inflation risks and a slowing economy

As widely telegraphed, the European Central Bank (ECB) kept its policy rates unchanged on Thursday, but the tone of the meeting reflected a far more complicated backdrop.

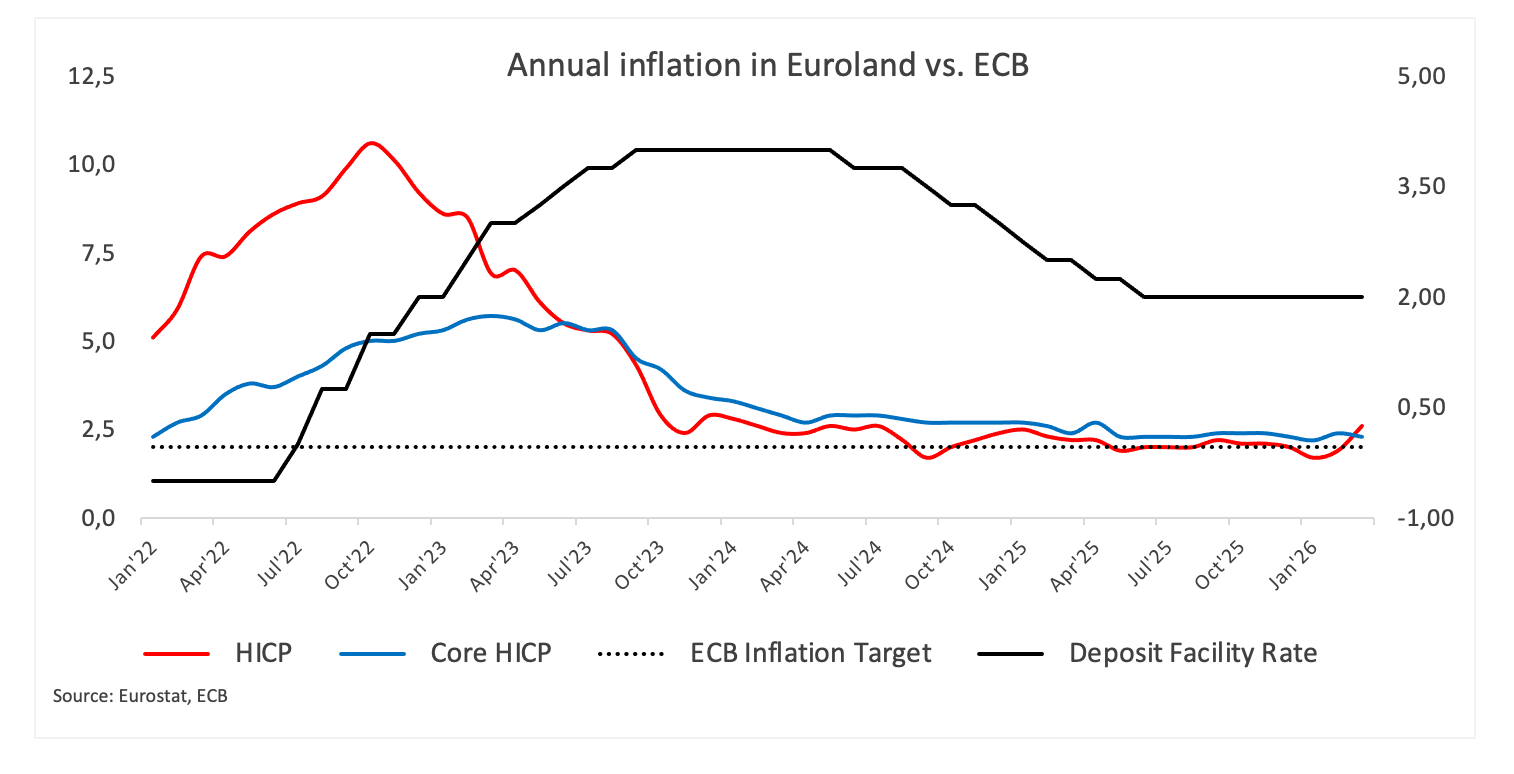

On one side, inflation risks are clearly building again. Indeed, higher energy prices are set to keep inflation well above target in the near term, and the bank openly acknowledged that risks to inflation are now tilted to the upside. That alone would normally argue for a more cautious stance on easing.

But the other side of the equation is becoming increasingly difficult to ignore. On this, the growth outlook is weakening with the central bank citing increased uncertainty, lower business confidence and rising pressure on supply chains. High energy costs are not only lifting inflation, but also eroding household incomes and discouraging investment, a combination that is starting to weigh on activity… and on some officials’ views.

When Christine Lagarde addressed the press, the message was one of caution and balance. She noted that the economy had entered this period of turbulence from a relatively solid starting point, with domestic demand still providing some support and households in a reasonably strong financial position. However, she also made it clear that the outlook has become highly uncertain and that risks to growth are now firmly tilted to the downside.

At the same time, there were a few signs of alarm on underlying inflation. Wage pressures appear to be easing gradually, and longer-term inflation expectations remain anchored around the 2% target. That gives the ECB some room to wait, even as near-term price pressures pick up again. It does seem reasonable to wait, but how long?

Bottom line

The ECB is navigating a classic stagflation risk: energy is pushing inflation higher, while growth is losing momentum. For now, that keeps policymakers firmly in wait-and-see mode, with no commitment to a particular rate path and a growing focus on how the balance between inflation and growth evolves in the coming months.

ECB FAQs

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy for the region. The ECB primary mandate is to maintain price stability, which means keeping inflation at around 2%. Its primary tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will usually result in a stronger Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

In extreme situations, the European Central Bank can enact a policy tool called Quantitative Easing. QE is the process by which the ECB prints Euros and uses them to buy assets – usually government or corporate bonds – from banks and other financial institutions. QE usually results in a weaker Euro. QE is a last resort when simply lowering interest rates is unlikely to achieve the objective of price stability. The ECB used it during the Great Financial Crisis in 2009-11, in 2015 when inflation remained stubbornly low, as well as during the covid pandemic.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the European Central Bank (ECB) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the ECB stops buying more bonds, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive (or bullish) for the Euro.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)