BoE recap: An 'active hold' as inflation risks re-emerge

The Bank of England (BoE) kept rates unchanged at 3.75%, but unlike a passive pause, this was framed as a deliberate and active policy choice.

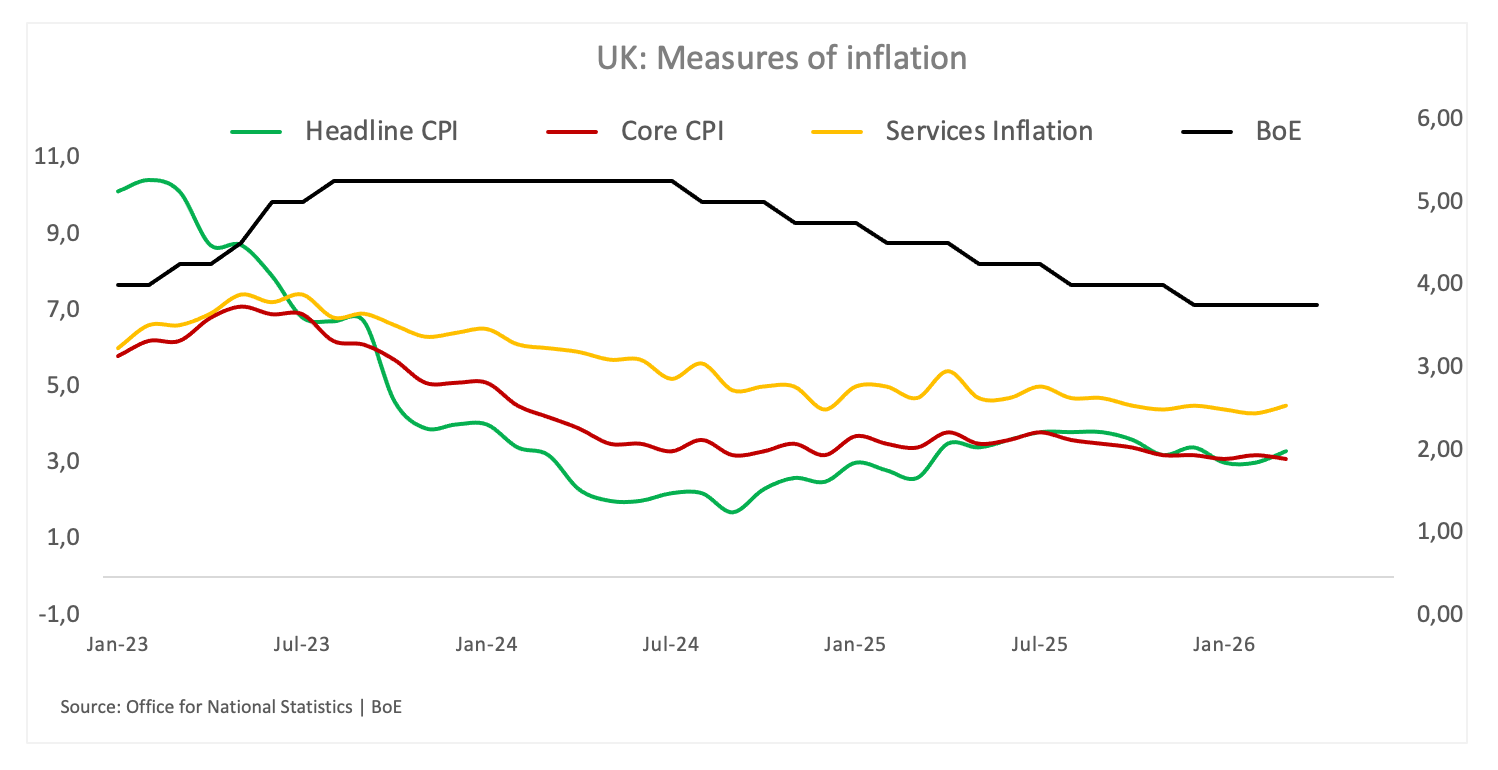

The decision itself was widely expected, but the 8–1 vote split, with one member pushing for a rate hike (Huw Pill), immediately signalled a more hawkish tilt beneath the surface. Policymakers are clearly becoming more concerned about the inflation outlook, particularly as higher energy prices begin to feed through the economy.

Governor Andrew Bailey made it clear that the current environment presents a difficult trade-off. Indeed, monetary policy cannot prevent the initial impact of higher global energy prices, but it must ensure that these shocks do not become embedded in wages and broader price-setting behaviour.

Furthermore, that risk of second-round effects was at the heart of the message. While still uncertain, Bailey stressed that waiting for definitive evidence would be a mistake, effectively signalling that the central bank is prepared to act pre-emptively if needed.

At the same time, the BoE is not rushing into further tightening. Instead, it is using its current stance, and crucially, the decision not to cut rates as previously expected, as a way to lean against inflation pressures. In that sense, policy is already doing more work than the headline decision might suggest.

The outlook, however, remains highly dependent on energy prices, particularly in light of the ongoing crisis in the Middle East. The longer the current shock persists, the greater the risk to both inflation and growth, leaving policymakers navigating a narrow and uncertain path.

All in all

This was not a dovish pause. The BoE is actively holding its ground, pushing back against rate cut expectations and keeping the option of further tightening alive if inflation pressures broaden.

BoE FAQs

The Bank of England (BoE) decides monetary policy for the United Kingdom. Its primary goal is to achieve ‘price stability’, or a steady inflation rate of 2%. Its tool for achieving this is via the adjustment of base lending rates. The BoE sets the rate at which it lends to commercial banks and banks lend to each other, determining the level of interest rates in the economy overall. This also impacts the value of the Pound Sterling (GBP).

When inflation is above the Bank of England’s target it responds by raising interest rates, making it more expensive for people and businesses to access credit. This is positive for the Pound Sterling because higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls below target, it is a sign economic growth is slowing, and the BoE will consider lowering interest rates to cheapen credit in the hope businesses will borrow to invest in growth-generating projects – a negative for the Pound Sterling.

In extreme situations, the Bank of England can enact a policy called Quantitative Easing (QE). QE is the process by which the BoE substantially increases the flow of credit in a stuck financial system. QE is a last resort policy when lowering interest rates will not achieve the necessary result. The process of QE involves the BoE printing money to buy assets – usually government or AAA-rated corporate bonds – from banks and other financial institutions. QE usually results in a weaker Pound Sterling.

Quantitative tightening (QT) is the reverse of QE, enacted when the economy is strengthening and inflation starts rising. Whilst in QE the Bank of England (BoE) purchases government and corporate bonds from financial institutions to encourage them to lend; in QT, the BoE stops buying more bonds, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive for the Pound Sterling.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.