Winter is coming: Middle East war, Oil shock, and the return of inflation?

The escalation of the war in the Middle East is rapidly becoming a global economic problem. Surging Oil prices are reviving inflation fears at a time when central banks believed the worst of the price shock was behind them. Europe, still vulnerable after the Russia-Ukraine energy crisis, could once again find itself at the center of the fallout. But it does not matter much in which corner of the world you live – the ongoing chaos will affect you.

Pain will be felt more deeply in the Northern Hemisphere and hit Europe harder, as winter is coming. Remember the still ongoing Ukraine-Russia war?

Early in 2022, Russian President Vladimir Putin decided that Ukraine was getting too much support from Europe and decided to put a halt to it. He invaded the country, thinking the takeover would last a few days, just like with the Crimean Peninsula.

Never in his wildest dreams would Putin have figured that four years later, he would still be dealing with Kyiv.

Moscow could never imagine the length and breadth of Western support to Ukraine, but this also came at the expense of weaponizing Gas supplies, provoking an unprecedented energy crisis for the EU, which saw gas prices increase by roughly 30%. The energy shortage in the Old Continent also resulted in higher liquefied natural gas (LNG) prices worldwide due to the increasing demand from the EU.

The EU learn its lesson and took action to end Russian energy imports and reduce its energy dependency from the Euro-Asian giant. EU leaders diversified energy imports and applied sanctions to Russia, while deciding to increase their storage ahead of winter.

And they clinched a good bunch of their goal: At the beginning of the 2025 winter season, Gas storage towards winter was at 95%.

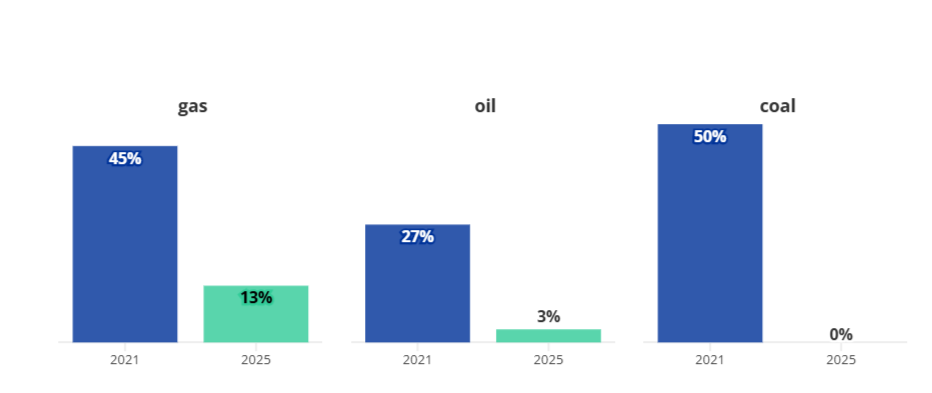

As of now, the share of Russian Gas, Oil, and coal in the EU's energy imports dropped significantly between 2021 and 2025, but Russian Gas and Oil have not been completely phased out yet, according to the European Commission.

Source: European Commission

At this point, it is worth remembering that inflation reached multi-decade peaks in 2022 and led to central banks rushing into hiking interest rates aggressively. Soaring energy prices due to Moscow’s decision to reduce supply to Europe were one of the reasons inflation skyrocketed.

With the ongoing war in the Middle East, there’s a feeling of déjà vu in many of the world’s capitals as they see how Crude Oil prices have risen a whopping 20% in the first week of March.

Higher Oil prices and the EU need to fulfill its energy goals are likely to revive inflationary pressures, at a time when most central banks are still in the final stage of their loosening monetary path.

Even further, Russian President Putin revived the idea of cutting off the little Gas he still supplies to Europe. The EU, in January, approved a ban on Russian Gas imports and the complete phase-out of Russian LNG by the end of 2027.

Putin responded through a local interview by suggesting he will halt Gas exports before the ban comes into play. "Now other markets are opening up. And it might be more profitable for us to stop supplies to the European market right now to move to those markets that are opening up and gain a foothold there," Putin said.

So here we are: In a world that is barely returning to its inflationary goals, in which central bankers took a break after a long battle to control it, and with fears of an Oil shock that is resurfacing ghosts from the past.

And of course, a world at war. The impact of the first week of back-and-forth attacks in the Persian Gulf is already hard to measure, but indeed negative. Skyrocketing energy prices will boost Inflation and there’s nothing nobody can do about it. Consumption is likely to remain reduced as real income will be affected. And let’s forget about economic growth outside the US.

In the meantime, speculative interest is piling up bets on interest rate hikes coming up. Can you imagine US President Donald Trump's reaction if the upcoming Federal Reserve Chair Kevin Warsh announces a rate hike? But well, that’s a story for another time.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.