Why Oil has not cleared $100: The VaR trap might be smothering the barrel

Takeaways by dark side of the boom

- VaR is the missing barrel. Oil may still have a bullish physical story, but if risk capital refuses to warehouse the trade, the fundamentals struggle to transmit into price.

- Open interest is the market’s oxygen gauge. When it drains this hard, it tells you investors are not just cautious. They are actively choosing not to fund crude exposure.

- Policy noise has turned oil into a headline volatility contract. Deal on, deal off, attack, no attack, ceasefire, sanctions, tanker risk. That makes the carry look less like compensation and more like a trapdoor.

- The barrel can be bullish while the balance sheet is bearish. Inventories, geopolitics, and supply risk still matter, but the paper market is capital-starved.

- Trade the view, but size the violence. In this tape, oil exposure has to be proportioned to OVX. Bigger conviction means nothing if the volatility toll booth is charging double.

- Oil below $100 is not proof of abundance. It is proof that capital aversion is smothering the upside before the physical story can fully ignite.

The VaR trap might be smothering the barrel

Hat tip to Jeffrey Currie for putting the sharper lens on this on X of all places, because I think he may be circling one of the more important control panels in the oil market.

The reason oil has not punched cleanly through $100 may not be simply that the physical market is comfortable. It may not just be the tanker-goat trail through the Middle East, larger reserve buffers, or the post-Covid change in consumer demand behaviour, although all of those likely matter. The deeper issue could be that the oil market has lost part of its financial transmission belt. The barrels may still be tight, inventories may still be drawing, and geopolitics may still be throwing sparks across the map, but the risk capital that normally turns those facts into price appears to have stepped back from the table.

That is where VaR becomes the important word. Not in the sterile textbook sense, but in the real trading desk sense. VaR is the amount of pain capital is willing to tolerate before the position becomes too hot to hold. It is the market’s risk budget. It is the permission slip. It tells you how much balance sheet is willing to sit in a trade when the tape gets noisy, the headlines go feral, and the price action starts moving faster than the spreadsheet.

And in oil, that permission slip looks like it may have been cut back aggressively.

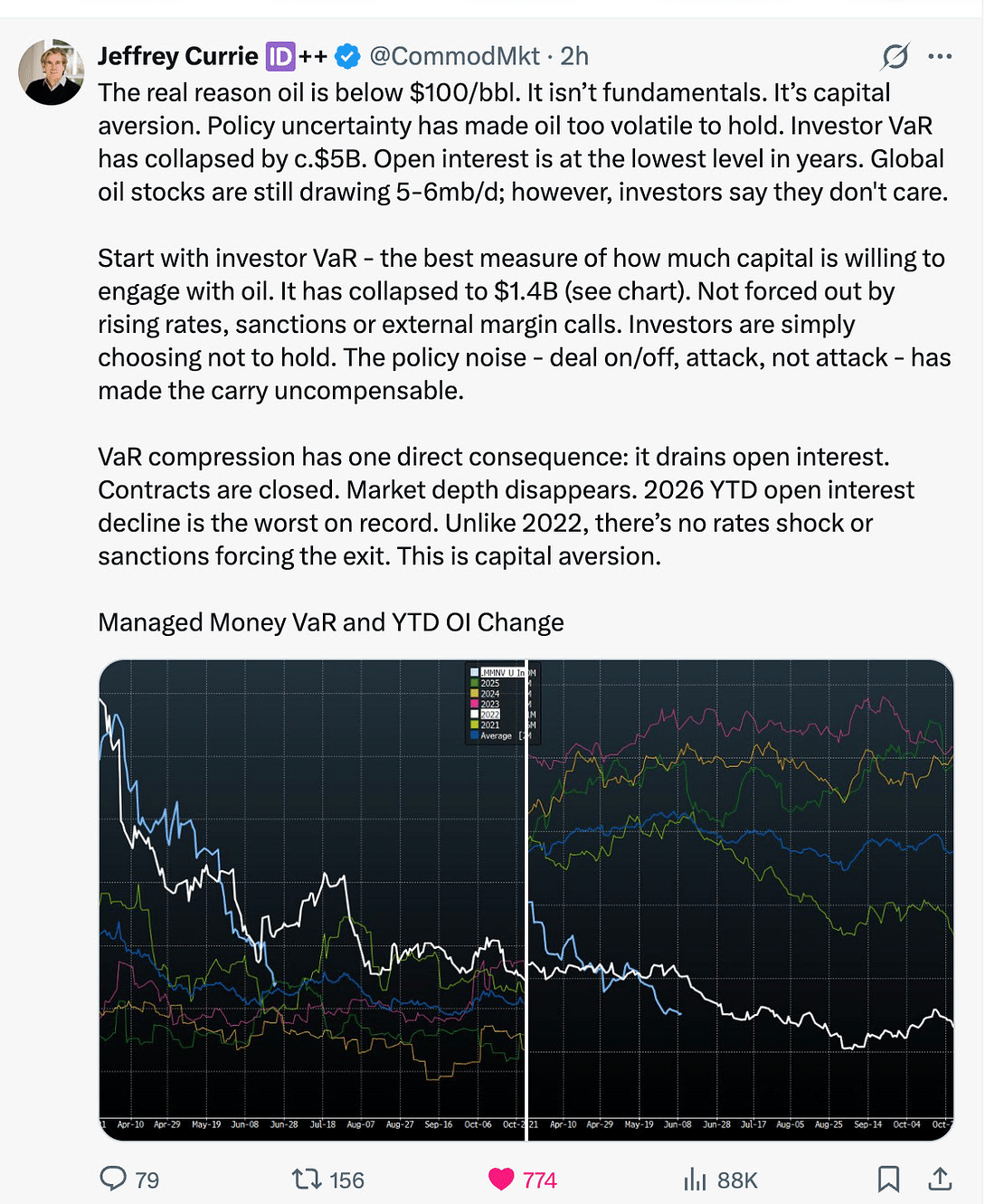

The point Currie makes, and I think it has real merit, is that investor VaR in oil has collapsed. That is not just some back-office metric. It is the oxygen level of the trade. When VaR shrinks, capital does not merely become cautious. It can physically leave the market. Positions are cut. Contracts are closed. Open interest drains. Market depth thins. The barrel still exists, but the balance sheet behind the barrel disappears. That may help explain how you can have a fundamentally tight oil market and still fail to generate the kind of durable upside that a classic supply shock would normally produce.

This is the key distinction. Oil below $100 may not be proof that the bullish fundamental case is dead. It may be proof that the bullish fundamental case is underfunded.

The old oil playbook says that if inventories are drawing, supply risk is rising, and the geopolitical map is glowing red, crude should trade higher until price rations demand or pulls new supply into the system. But that playbook assumes investors are willing to warehouse the risk. Right now, they may not be. The policy environment has turned oil from a carry trade into something closer to a headline volatility contract. Deal on. Deal off. Attack. No attack. Sanctions. No sanctions. Ceasefire. Broken ceasefire. Tankers rerouted. Hormuz risk priced, then faded, then repriced again before lunch.

That kind of market is not merely volatile. For many institutional investors, it may be close to unholdable.

The carry may look attractive on paper, but the overnight gap risk can make it feel uncompensable. Nobody wants to explain to an investment committee why they were long a geopolitical barrel into a 5% air pocket because a policy headline changed between New York close and Asia open. That is the VaR trap. The market may want to own the bullish story, but the risk system may not allow it to hold the position at size.

This is also why open interest matters so much here. Open interest is not just a plumbing statistic. It is the footprint of conviction. When open interest collapses, the market may be telling you that capital is not prepared to engage. It does not necessarily mean traders cannot see the argument. It may mean they do not want to fund the argument. In 2022, oil risk was forced around by sanctions, rates, margin pressure, and the shock of a physical energy crisis. This feels different. This may be less about forced liquidation and more about capital aversion. Investors may simply be choosing not to carry crude because the policy noise has made the trade structurally unstable.

That is a very different animal.

And this is where the needle needs to be threaded properly. I do not buy the blunt version that says fundamentals do not matter. Fundamentals always matter in oil. The barrel is still the barrel. Inventory draws matter. Spare capacity matters. Tanker routes matter. Strategic reserves matter. Demand destruction matters. But fundamentals only become price when capital is willing to express them. Right now, the physical market may be whispering of a shortage, while the financial market is shouting about risk reduction.

So the better formulation may be this: fundamentals are the loaded spring, but VaR compression could be why the spring has not snapped.

That also fits with what we are seeing on the ground. The tanker-goats that trail through the Middle East matter because they show the market is still finding ways to move barrels around the danger zone. Larger reserve buffers may matter because they provide policymakers and consumers with greater shock absorption than markets had in older cycles, even if those buffers are difficult to quantify precisely. Post Covid demand behaviour may matter because consumers and businesses have become more adaptive to price spikes, substitution, and mobility changes. But those are only part of the answer. They may explain why the panic has been contained. VaR may explain why the rally has not found sponsorship.

The paper market looks capital starved.

That is the part many people may be missing. Oil can be tight and still trade heavy if the marginal buyer is no longer a patient macro allocator. If the marginal buyer is a fast money desk, then the market becomes a headline scalping machine. Rallies get sold faster. Dips become tactical rather than strategic. Risk is rented, not owned. The market starts behaving less like a structural bull market and more like a casino table where everyone wants the upside but nobody wants to sleep with the chips overnight.

That is why $100 has become such a psychological wall. It is not just a price level. It is the point where the market asks: who is willing to add balance sheet here? Who is willing to carry this through the next policy headline? Who is willing to own crude when diplomacy, missile risk, reserve politics, and tanker insurance are all sitting in the same cockpit?

At the moment, the answer may be: not enough.

This is why I am still trading oil, but sizing it against OVX. That is not some academic exercise. It is survival. When oil volatility is elevated, the same notional position carries a much larger risk footprint. Bigger conviction does not justify bigger size if the volatility toll booth has doubled the cost of entry. In this market, the position size has to respect the violence of the tape. The barrel can be right and the trade can still be wrong if the VaR math is wrong.

That is the trader’s lesson here. You can have the right macro view and still get carried out if the market structure refuses to finance the view.

So when people ask why oil is not through $100, I would not answer with one clear fundamental explanation. The answer is layered. Yes, tankers are finding routes. Yes, reserve buffers may be bigger than the market can precisely quantify. Yes, demand behaviour may have changed since Covid. Yes, consumers respond faster, and policymakers have become more willing to lean against energy shocks. But the missing ingredient may be risk capital. The oil market may have become too volatile to hold, and when VaR collapses, the bullish barrel can lose its sponsor.

That may be why crude feels like it should be higher but keeps failing to escape gravity.

Oil is not necessarily capped because the world is swimming in abundance. It may be capped because the capital stack has gone missing. The physical market may still be drawing. The geopolitical map may still be smoking. But the paper barrel appears under-owned because investors do not want to fund a policy minefield. Until VaR expands again, open interest rebuilds, and capital decides the carry is worth the headline risk, oil can remain fundamentally tight yet financially constrained.

In other words, the barrel may be bullish, but the balance sheet may be bearish.

And right now, the balance sheet may still be winning the tape.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.