When presidents move markets

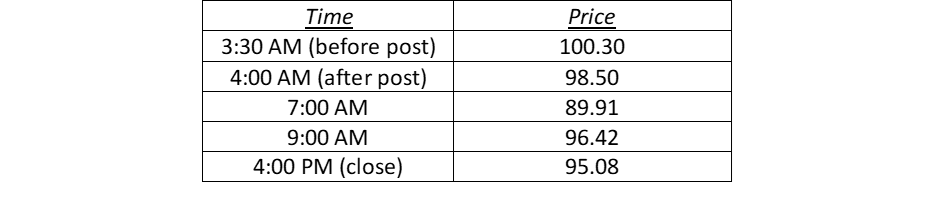

At 3:40 AM on May 6, a spike in trading volume occurred in the market for crude oil futures. Allegedly, someone — perhaps several people — was aware that later that morning Trump would be posting something on Truth Social that they believed would depress crude oil futures prices. They saw an opportunity and took it to front run the anticipated price change. The post came out at 3:50 AM and prices did, indeed, tumble. The drop lasted for the next two hours before making a partial recovery. This history is reflected in the circled portion of the chart below.

This chart may be a bit confusing, because the May 6 trading day starts at 5 PM on May 5 and ends at 4 PM on May 6. Moreover, the chart only reflects prices as of the hour and half hour, so it provides a general indication of what went on that day, albeit one lacking some degree of precision. In any case, here are the critical times and prices pulled from that chart:

As you can see, anyone who managed to execute a short position (i.e., a bet that prices would move lower) prior to Trump’s posting would have made a profitable trade. How much they made would depend on (a) the price at which they entered the market with the original short sale and (b) the price at which they liquidated their position. Few would be expected to exit at the exact, lowest price of the day on May 6; but clearly, any short position initiated before the posting would have ended up yielding a profit-– a sleazy one, but a profit nonetheless.

Here’s the text of Trump’s post on Truth Social:

“Based on the request of Pakistan and other Countries, the tremendous Military Success that we have had during the Campaign against the Country of Iran and, additionally, the fact that Great Progress has been made toward a Complete and Final Agreement with Representatives of Iran, we have mutually agreed that, while the Blockade will remain in full force and effect, Project Freedom (The Movement of Ships through the Strait of Hormuz) will be paused for a short period of time to see whether or not the Agreement can be finalized and signed.”

This story amazes me. To be clear, the spike in the trading volume preceding the post and the severity of the market drop do seem to indicate something nefarious transpired, and I, for one, would love to know who may have been involved. In fact, this information is knowable. The Commodity Futures Trading Commission has the capacity to identify those traders, and if a connection to the administration is found, those parties should be identified and held to account. To be clear, the CFTC routinely investigates situations like this, but no public statements about this specific instance have been made. I wait with bated breath.

Aside from the issue of market manipulation or abuse, I’m struck by the scale of the market reaction. Underlying the allegation is the presumption on the part of the short sellers that the market response to the announcement had a high likelihood of moving the market — and probably not by just a little. Perhaps whoever made those trades didn’t know exactly what Trump was planning to say, and he or she thought that the content would be more definitive. I read the post and marvel at (a) how little it says and (b) how the market reacted to it. In any case, it seems that the market ignored — or at least gave little consideration to — the fact that Trump still intended to maintain the blockade and that we had still not reached an agreement with Iran. The idea of returning to anything approaching the status quo ante with a blockade in place and no agreement in place seems totally contradictory. Posting anything was premature.

Surely, the post injected some measure of optimism about an off-ramp from this nightmare, but enough to foster a $10 a barrel adjustment in the price of crude? That seems crazy to me, as would the idea of any sane person risking his or her capital on such a bet. In fact, ultimately, the market saw that the pendulum had swung too far and gave back more than half of that decline. Moreover, we’ve been hearing for weeks from industry professionals that it’ll likely take months for any substantial decline in energy prices to occur. Given all the vagaries and uncertainties in Trump’s post, even a $5 per barrel reaction to this “news” seems excessive.

Dramatic price changes by themselves are concerning. They jeopardize the confidence that institutional agents will have in this market’s capacity to deliver fair and reasonable prices; and when that confidence erodes, so too does the willingness to use these contracts for hedging purposes. Without these institutional players, we’re left with a population of speculators whose only objective is to pick each other’s pockets; but more critically, we lose a vital risk management tool that supports capital formation and the willingness of companies to invest.

In this instance, the responsibility for the volatility we’ve witnessed is shared. Trump’s post was likely intended to manipulate expectations and crude oil prices. It appears that he got what he was after, and the traders who executed the short trades prior to the posting simply got the ball rolling. Those traders deserve to be sanctioned for jeopardizing the integrity of an important market institution. The bigger problem, as I see it, is that Trump simply doesn’t know when to keep his mouth shut; and unfortunately, that seems unlikely to change.

Author

_Profile.jpg)

Ira Kawaller

Derivatives Litigation Services, LLC

Ira Kawaller is the principal and founder of Derivatives Litigation Services.