UK inflation heads towards 4%, but rate hikes off the table for now

UK inflation rose in March on higher fuel prices, and a forthcoming increase in household energy bills this July is likely to take it towards 3.5-4%, depending on where wholesale natural gas prices go next. We don't think the bar for a Bank of England rate hike has been met.

The latest rise in UK headline CPI tells us virtually nothing about the scale and duration of the inflation wave to come. The Bank of England is still flying blind, with the conflict unresolved. But the limited amount of survey data available so far suggests little cause for alarm on inflation. And against a fragile jobs market, we don’t expect a rate hike next week, or this year.

As for that March data, there was nothing too surprising. The combination of higher motor fuel and heating oil prices added roughly 40bp to headline inflation, which now sits at 3.3%. Services inflation was up, though only because of volatile air fares; our estimation of the Bank of England’s preferred gauge of “core services” stayed at 4.2%.

On ING’s base case for oil and natural gas prices – which has the former staying between 90-100 USD/bbl in the second and third quarters of the year, and the latter averaging 55 EUR/MWh this quarter – we’d expect UK inflation to peak fractionally above 4% in August/September, but generally bouncing around a 3.5-4% range in the second half of the year. That’s consistent with a 25% rise in household electricity/gas bills when the Ofgem price cap is next updated in July. And these forecasts assume some uptick in food inflation later this year.

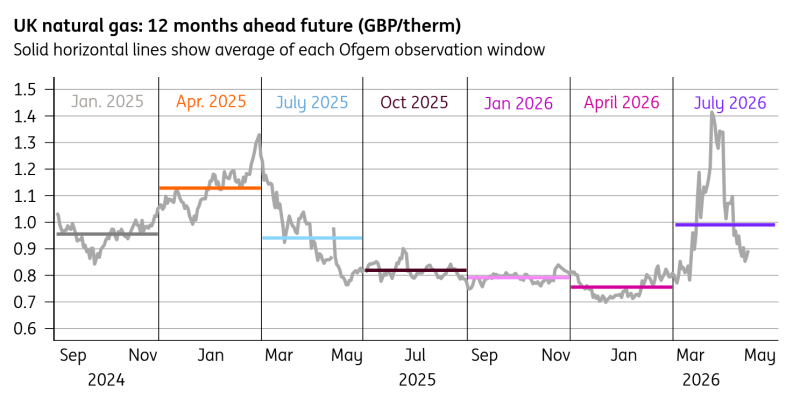

Wholesale Natural Gas prices close to pre-war levels

Since we last updated our scenarios, natural gas prices have come under renewed downward pressure. And remarkably, futures prices for delivery 12 months into the future are within spitting distance of their pre-war levels. And this matters for the Ofgem price cap, which tries to mimic what energy providers pay to lock in future supplies. If wholesale prices stay where they are today, the July price cap is more likely to rise by a mere 10-15% and retrace much of that increase in October. That’s consistent with inflation peaking around 3.5%.

So long as inflation doesn’t spike materially above 4% – a level above which the Bank has identified as being more likely to trigger a persistent bout of price pressure – we think the BoE will prefer to keep rates on hold this year.

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.