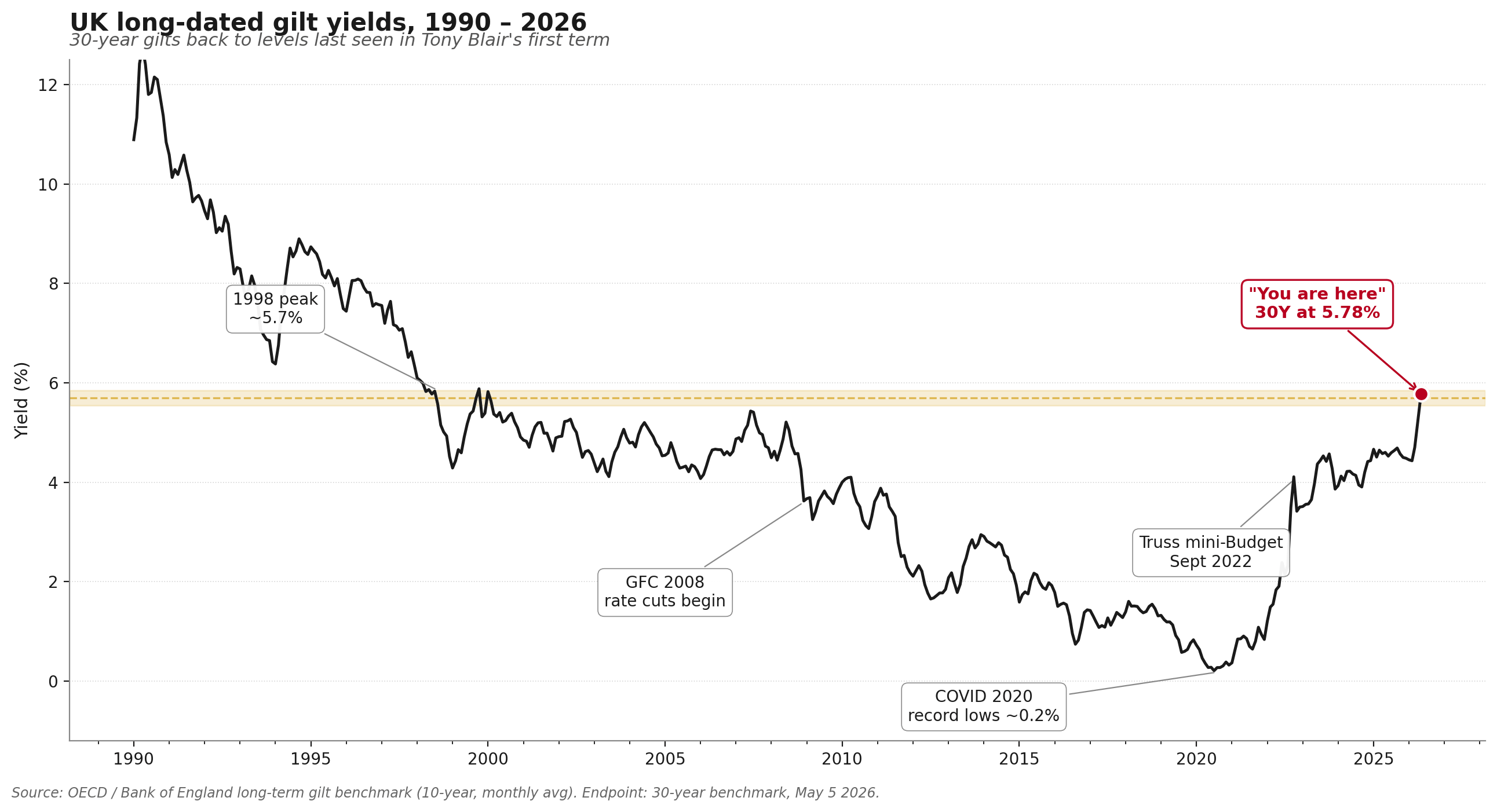

UK 30-year gilts hit 5.78%, the highest since 1998: what is being priced in?

UK 30-year gilts traded as high as 5.78% on Tuesday, the highest level since 1998, while 10-year yields topped 5.10% with markets pricing in nearly three-quarter-point Bank of England (BoE) rate hikes this year. The selloff is being driven by a converging set of forces: speculation over Prime Minister Keir Starmer's leadership, fresh anxiety over the UK's fiscal rules, and Iran-conflict energy inflation feeding through into the headline rate. It comes ahead of the BoE's June 18 rate decision and into a structurally weaker buyer base for long-dated gilts than the UK has had in a generation.

A yield from another century

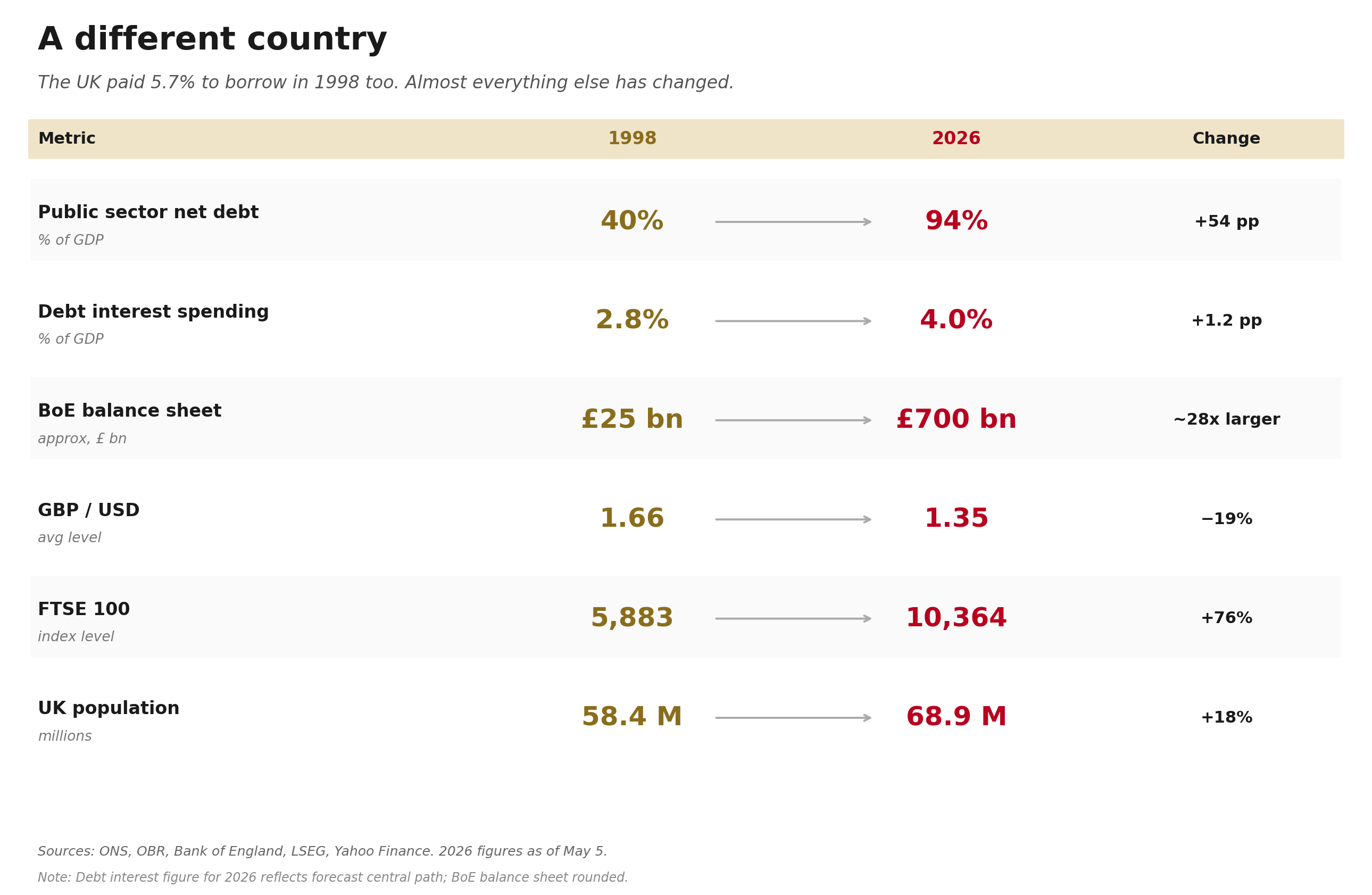

The last time UK 30-year gilts traded near 5.8%, Tony Blair was in his first term as Prime Minister, the Euro did not exist, and the iPhone was nine years away. The yield level itself is not a crisis; pre-2008, the UK routinely paid this much to borrow. What has changed is everything sitting underneath it. Public sector net debt is now 94.3% of GDP, up from roughly 40% in 1998.

Debt interest spending hit a post-war high of £111.6 billion in 2022-23, equivalent to 4.3% of GDP. The point is not that 5.78% is unprecedented: the point is that 5.78% means something very different on a debt stock that has more than doubled relative to the economy.

Bond traders are voting first

This week's acceleration has less to do with inflation than with politics. Speculation has intensified over a possible Labour Party leadership contest and what it would mean for the UK's fiscal rules, with bond traders pricing a higher term premium for the uncertainty. As noted by analysts, political risk feeds directly into the term premium and ultimately into the cost of UK borrowing. The market is essentially front-running an electoral conversation that has not formally started.

It is tempting to compare this to September 2022, when Liz Truss's mini-Budget sent 30-year yields up more than 100 basis points in four days. The comparison is instructive mostly in what is different. The 2022 episode was a single-event shock with a forced-seller amplifier in the liability-driven investment (LDI) sector. This time, there is no shock and no forced seller. Yields have walked here on their own, driven by the slow accumulation of inflation, fiscal, and political risk. Different mechanism, same destination.

Translate the figure into Pound Sterling (GBP) terms, and the political stakes sharpen: a sustained 1% rise in gilt yields adds roughly £15 billion to annual borrowing costs by 2030, according to the Office for Budget Responsibility’s (OBR) sensitivity analysis. Chancellor Rachel Reeves' £21.7 billion of fiscal headroom looks much smaller against a yield curve that has drifted higher for three months straight.

The plumbing nobody is looking at

Here is the part most coverage skips: the natural buyer of long-dated gilts has historically been UK defined-benefit pension schemes, which used LDI strategies to match long-dated liabilities. Higher yields have done their job; most schemes are now in surplus and are de-risking via insurance buy-ins, a process that typically involves selling gilts rather than buying them. The BoE itself flagged this in a recent insights paper, noting that long-maturity gilt supply is now being met by more price-sensitive participants who lack natural demand for long duration.

Now add in the BoE's own quantitative tightening (QT) program, currently running at £70 billion of stock reduction for the year to September 2026. The BoE has already tilted away from selling long-dated gilts to better reflect demand conditions, a polite admission that the long end cannot easily absorb more supply.

Meanwhile, the Debt Management Office (DMO) needs to fund a £257 billion gross financing requirement through 2027. Less natural demand, more price-sensitive demand, and a central bank still actively selling into the market. That is the structural picture beneath the headline yield.

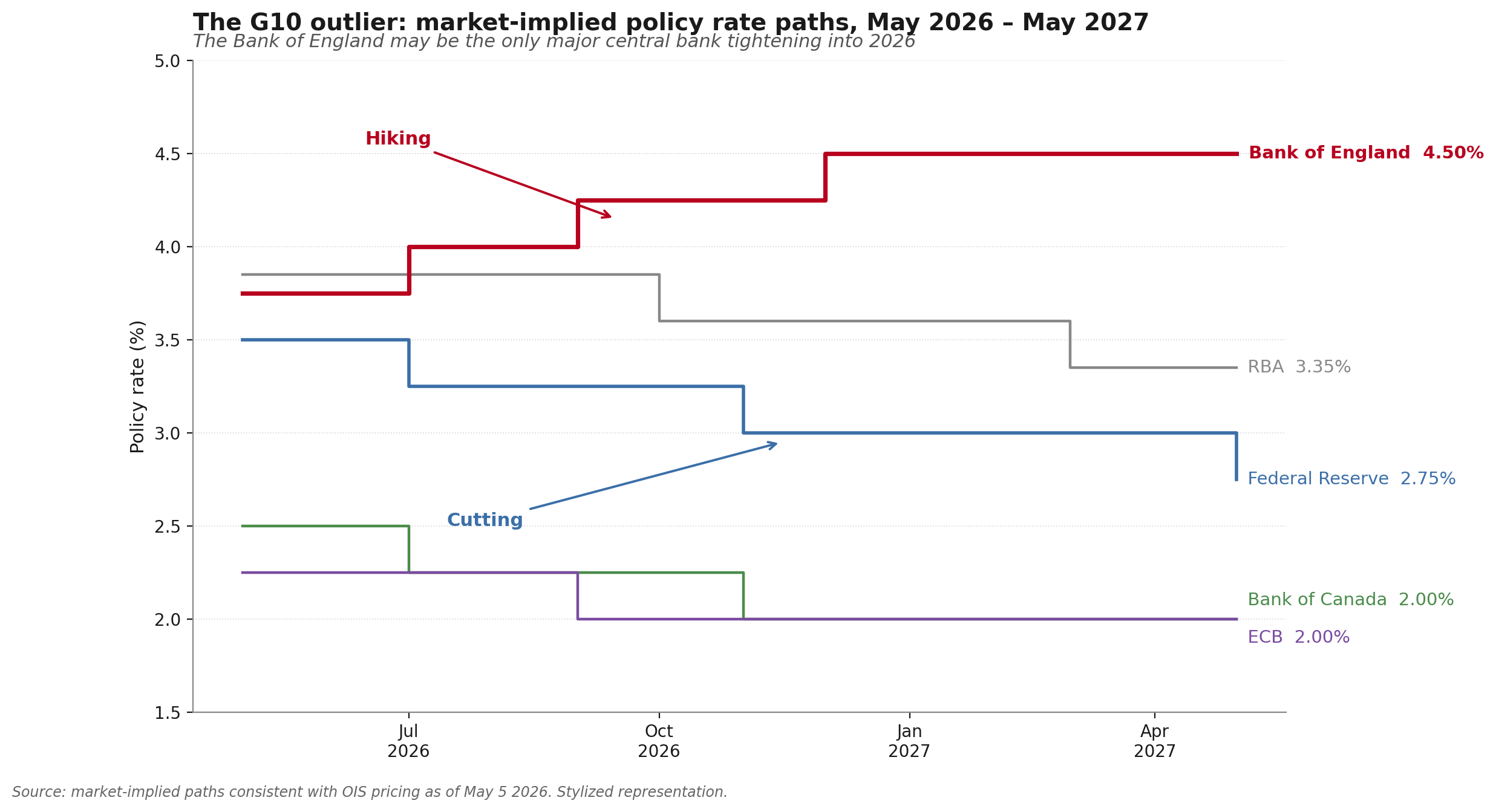

The G10 outlier

The forex implication is the most underappreciated part of this story. The Federal Reserve (Fed), European Central Bank (ECB), and Bank of Canada (BoC) are all in cutting cycles. The BoE held at 3.75% on April 30 in an 8-1 vote, with one Monetary Policy Committee (MPC) member voting to hike to 4%. Markets are now pricing in around three-quarter-point hikes from the Bank this year, driven by Iran-conflict energy inflation and the prolonged closure of the Strait of Hormuz.

That makes the BoE the only major G10 central bank seriously discussing tightening into 2026. In theory, that should support the Pound. In practice, the Sterling has been treading water, a pattern that suggests investors are pricing in higher rates as a fiscal-stress response rather than a growth-positive signal. The Pound is not behaving like a high-yielder; it is behaving like a currency whose central bank may have no choice but to follow yields higher, whether it wants to or not.

The next BoE decision is on June 18. Markets will be watching the vote split as closely as the rate itself. If a second member joins the hike camp, the question is no longer whether the Bank can resist the global easing momentum, but whether the gilt market is even willing to give it a choice.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.