The Iranian regime’s energy blackmail: Aimed at the US, felt in Asia

The real shape of the shock

By threatening Hormuz and regional energy flows, Tehran is trying to raise the cost for Washington, but the immediate economic damage is landing far more heavily on Asia and its Gulf neighbors.

The Iranian regime may present disruption in the Strait of Hormuz as a way to raise the cost of war for the United States and the West, but the immediate economic burden falls much more heavily on the countries physically tied to Gulf energy flows. Around 20 million barrels per day of oil normally move through the Strait, and roughly one-fifth of global LNG trade also passes through it. By contrast, alternative pipeline capacity through Saudi Arabia and the UAE is only around 3.5 to 5.5 million barrels per day, far below normal Hormuz volumes.

This is not just a price shock. It is a logistics shock. When the route itself becomes unsafe, the question is no longer simply who produces energy. The real question is who can still move it. That is why the geography of the disruption matters more than the slogans surrounding it.

Why some exporters benefit while others do not

The clearest short-term winners are the energy exporters outside the Gulf chokepoint. They can sell into a higher-price market without depending on Hormuz for export access. In practical terms, they receive the benefit of tighter supply without suffering the same transport constraint.

Canada is a good example. Canadian crude exports averaged about 4.20 million barrels per day in 2024. Using a simple rule of thumb, every 10 dollar rise in oil prices adds roughly 42 million dollars per day in gross export value. Norway sits in a similar position. With output around 2.0 to 2.2 million barrels per day, a 10 dollar increase in oil adds roughly 20 to 22 million dollars per day in gross value. Brazil also fits the same pattern. With crude production around 3.8 to 4.0 million barrels per day, the gain is roughly 38 to 40 million dollars per day for each 10 dollar move higher in oil.

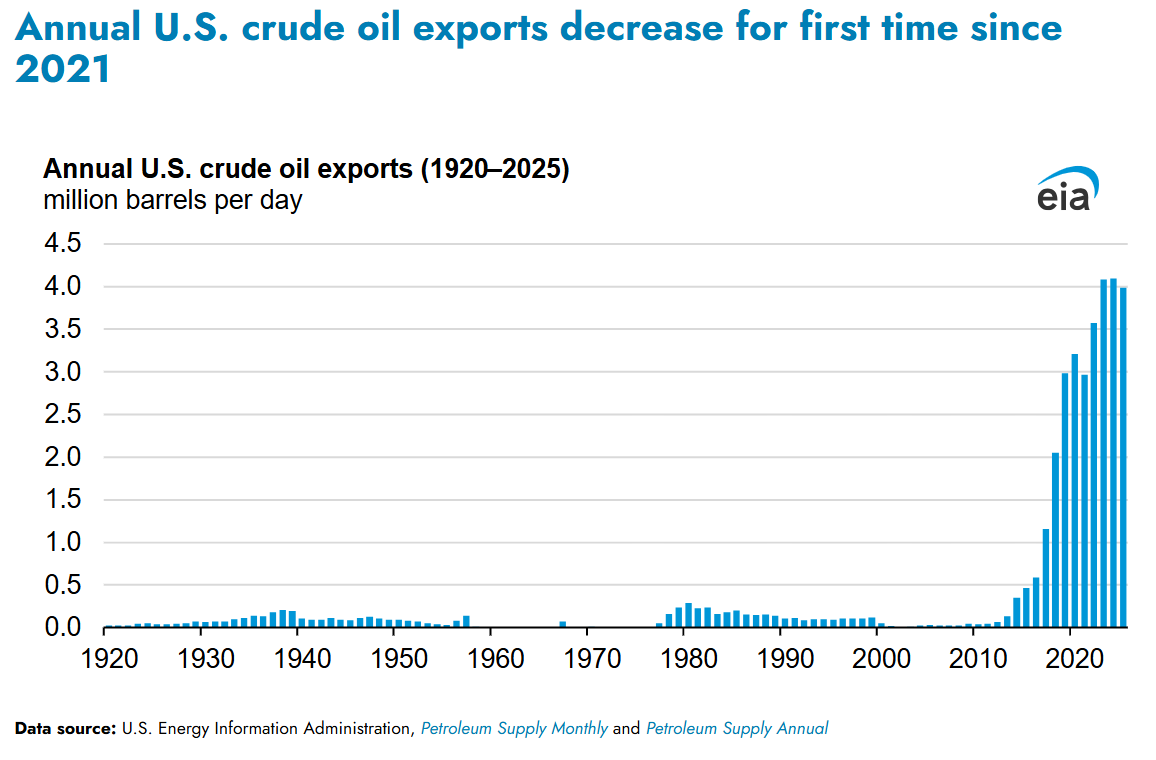

The U.S. upstream sector also benefits in this sense. With crude exports around 4.0 million barrels per day and domestic production at roughly 13.6 million barrels per day, a 10 dollar rise in oil prices implies about 40 million dollars per day in extra crude export value and around 136 million dollars per day in additional upstream gross production value. That does not make the entire American economy a winner. Higher oil prices still hurt consumers, transport costs, and inflation expectations. But in the short run, the U.S. energy sector is one of the clearest beneficiaries of a supply shock centered far from its own export routes.

For forex traders, the message is straightforward. Countries that can keep exporting from outside the chokepoint gain terms-of-trade support. Countries trapped behind the chokepoint do not.

Why Gulf producers are not automatically winners

A common mistake in energy shocks is to assume that all oil and gas exporters benefit when prices rise. That logic breaks down when the export route itself is under threat. Higher prices help only if the producer can still deliver the volume.

In a Hormuz disruption, the most vulnerable exporters are the ones whose barrels are effectively trapped behind the Strait. Saudi Arabia and the UAE have some ability to reroute supply through pipelines to the Red Sea and Fujairah, which makes them less exposed than some neighbors. But even together, that bypass capacity is far too small to replace normal Hormuz flows. They are better positioned than others, not protected from the shock.

Iraq is one of the clearest losers because its vulnerability is not just commercial. It is fiscal and political. Under disruption conditions, reported crude output has been around 1.4 million barrels per day, far below normal levels, while more than 90 percent of government income depends on oil. That means Iraq does not simply lose shipments. It loses the revenue stream that finances the state itself.

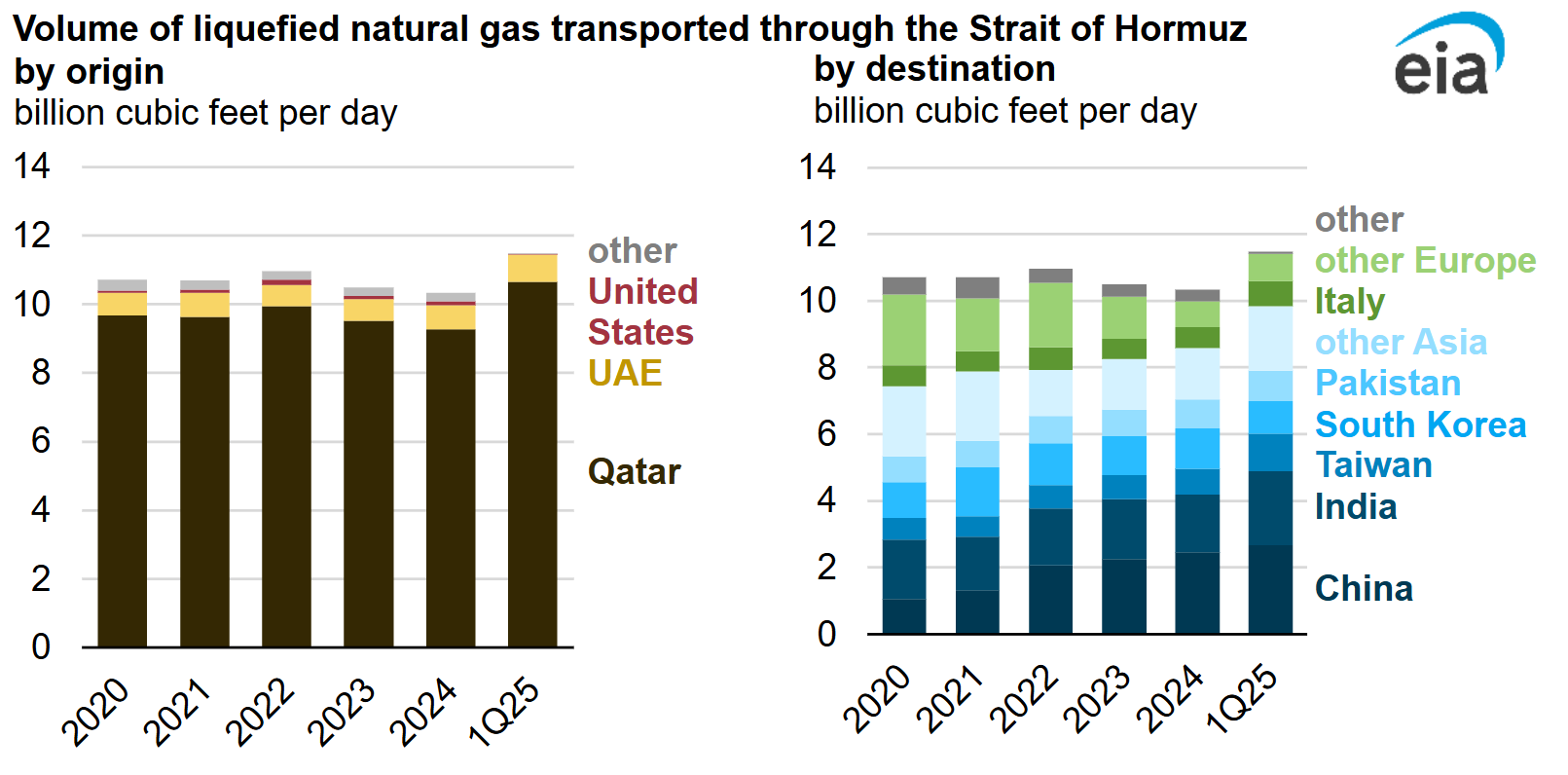

Kuwait faces a similar structural problem. It remains highly dependent on Hormuz for exports and has limited rerouting flexibility. Qatar is even more exposed in strategic terms because this is not only an oil story. It is also an LNG story. Roughly one-fifth of global LNG trade moves through Hormuz, much of it from Qatar, and around 83 percent of that LNG goes to Asian markets. That makes Qatar central to any global gas disruption linked to the Strait.

So the irony is obvious. Some of the countries sitting closest to the world’s most important energy chokepoint are not the biggest beneficiaries of higher prices. In a severe disruption, they become some of the biggest losers.

Why Asia carries the heaviest burden

This is where the numbers become decisive. Around 84 percent of the crude oil and condensate moving through Hormuz goes to Asian markets. Around 83 percent of LNG moving through the Strait also goes to Asia. China, India, Japan, and South Korea together account for roughly 69 percent of Hormuz crude flows. In other words, if Hormuz is disrupted, the first and biggest external shock does not land in Washington. It lands across Asia.

Japan is one of the clearest examples. About 95 percent of its oil imports come from the Middle East. Imports were roughly 2.8 million barrels per day in January, and around 70 percent of those flows depend on Hormuz. Japan does have substantial emergency reserves equal to about 254 days of consumption. That reduces the risk of an immediate physical shortage, but it does not remove the macroeconomic hit. Reserves can cushion supply disruption. They do not fully shield the economy from higher prices, imported inflation, or pressure on the trade balance.

South Korea looks similar. Around 70 percent of its oil and 20 percent of its LNG come from the Middle East, with about 208 days of consumption in reserve. That provides some short-term protection, but it does not change the underlying exposure. Even well-prepared importers are forced into emergency policy responses when Gulf energy routes are under pressure.

India is a more mixed case. On crude, it is less vulnerable than before because non-Hormuz sourcing has reportedly risen to around 70 percent of total imports. That is a meaningful improvement in resilience. But India still has important exposure through LPG and gas. A large share of LPG imports still comes through Hormuz, and parts of the gas supply chain remain vulnerable to Gulf disruption. So India has reduced one weakness without eliminating the broader energy shock.

China is highly exposed in absolute scale. Roughly half of its oil imports and about one-third of its LNG imports come from the Middle East. But China is less fragile than many peers because it has much larger strategic reserves, estimated at around 900 million barrels, along with greater state capacity to manage disruption. That does not make China safe. It makes China more resilient in the immediate term than countries such as Japan, South Korea, Bangladesh, or Pakistan.

The smaller and poorer importers are where the arithmetic becomes harsher. Bangladesh and Pakistan are particularly vulnerable because they combine energy dependence with thinner financial and logistical buffers. A country with deep reserves and stronger state capacity can absorb the same shock more easily. A country without those buffers feels the damage faster and more intensely. That is the brutal logic of chokepoint crises.

Why the United States is affected, but not in the same way

The United States is not immune to a Hormuz crisis. Higher oil prices raise inflation risk, complicate interest-rate expectations, and add political pressure through gasoline prices and market volatility. But the direct physical supply vulnerability is much lower than in Asia. The United States has sharply reduced its dependence on Middle Eastern oil over time and imports virtually no LNG from the region.

That distinction matters. America feels the shock mainly through price, inflation, and politics. Asia feels it through physical exposure, import dependence, and direct energy-security risk. Those are not the same thing. One is an indirect macroeconomic problem. The other is a core supply vulnerability.

For traders, this is not a semantic detail. It is the difference between a market narrative driven by inflation pressure and one driven by real disruption to external balances and energy access. The United States may feel the political sting of higher energy prices, but the countries most directly tied to Gulf energy flows carry the heavier economic burden.

The deeper strategic conclusion

In my view, the Iranian regime’s attempt to close or militarily disrupt the Strait of Hormuz is less a precise blow against the United States than a broad act of economic coercion designed to create fear, disrupt trade, and raise the political cost of war through global energy markets. It is not a narrow tactical move. It is a deliberately wide shock.

The evidence points in that direction. This has not been limited to rhetoric about the Strait. Civilian shipping has been attacked. Regional energy infrastructure has been hit. Insurance costs, shipping risk, and supply anxiety have all surged. That pattern suggests a willingness to endanger the wider civilian trading system in order to increase pressure on the West.

But the deeper irony is that this strategy may end up hurting South Asia, Asian importers, and the Iranian regime’s Gulf neighbors more directly than the United States itself. That does not make America untouched. It makes the burden uneven. And that unevenness is the central quantitative conclusion of the article. The shock falls hardest on those most dependent on Gulf oil and gas routes, not on the country the Iranian regime most wants to pressure.

There is another layer to this. By turning Hormuz into a source of insecurity for civilian shipping and regional energy infrastructure, the Iranian regime may end up producing the opposite long-term result from the one it seeks. Rather than fracturing Western resolve, it may strengthen coordination among Europe, the United States, and Gulf states around a more durable maritime and energy-security framework. It may even encourage major Asian economies, many of which are more directly exposed to Gulf disruption than the United States is, to align more closely with Western efforts aimed at securing energy routes and building more durable supply resilience.

That final outcome is still a forward-looking inference, not a settled fact. But it is a reasonable one. When a regime tries to weaponize a global energy chokepoint, it does not just raise prices. It also teaches the rest of the world a hard lesson about dependence, vulnerability, and the cost of leaving strategic trade routes exposed.

Final takeaway

The short-term winners in a Hormuz shock are mostly oil and gas exporters outside the Gulf chokepoint that can continue shipping into a tighter market. The short-term losers are mostly Gulf exporters trapped behind the Strait and Asian importers that rely heavily on Gulf crude and LNG. That is the hard numerical reality.

So, while the Iranian regime may portray Hormuz disruption as pressure on the United States, the numbers tell a different story. The immediate damage falls more heavily on Asia, neighboring Gulf economies, and the broader civilian energy system. In that sense, this is not only an energy-market shock. It is a test of who is most exposed to the infrastructure of globalization itself.

Author

Ali Mortazavi

Errante

BEc, CMSA, Member of IFTA - International Federation of Technical Analysis, Associate Member of STA - Society of Technical Analysis (UK).