Some losses for the Dollar ahead of the NFP

Continuing expectations of a treaty in the Gulf have been somewhat negative for the greenback.

News on 4 June that Israel and Lebanon had agreed a ceasefire seemed to be positive for progress between the USA and Iran with participants in financial markets remaining generally confident that the conflicts will be resolved within the next few weeks. The key data for CFDs on 5 June is the American job report. This article summarises recent news and the context of the American job market then looks briefly at the charts of EURUSD and USDJPY.

The latest financial news has been dominated by speculation about SpaceX’s IPO announced late GMT on 3 June. However, for CFDs specifically, oil retreated somewhat while gold bounced on 4 June as participants continued to see the light at the end of the tunnel for the Gulf conflict. With Israel and Lebanon having agreed a ceasefire, one primary sticking block between the USA and Iran might have been removed. However, Hizballah wasn’t consulted about the Israeli-Lebanese agreement and it didn’t give a timeline for the end of Israel’s current occupation of border areas in southern Lebanon.

While traders will continue to monitor major news from the Middle East and the Gulf, they’re also gearing up for 5 June’s NFP. There’s some variation in expectations but overall the consensus is for a somewhat weaker release than last month’s strong data:

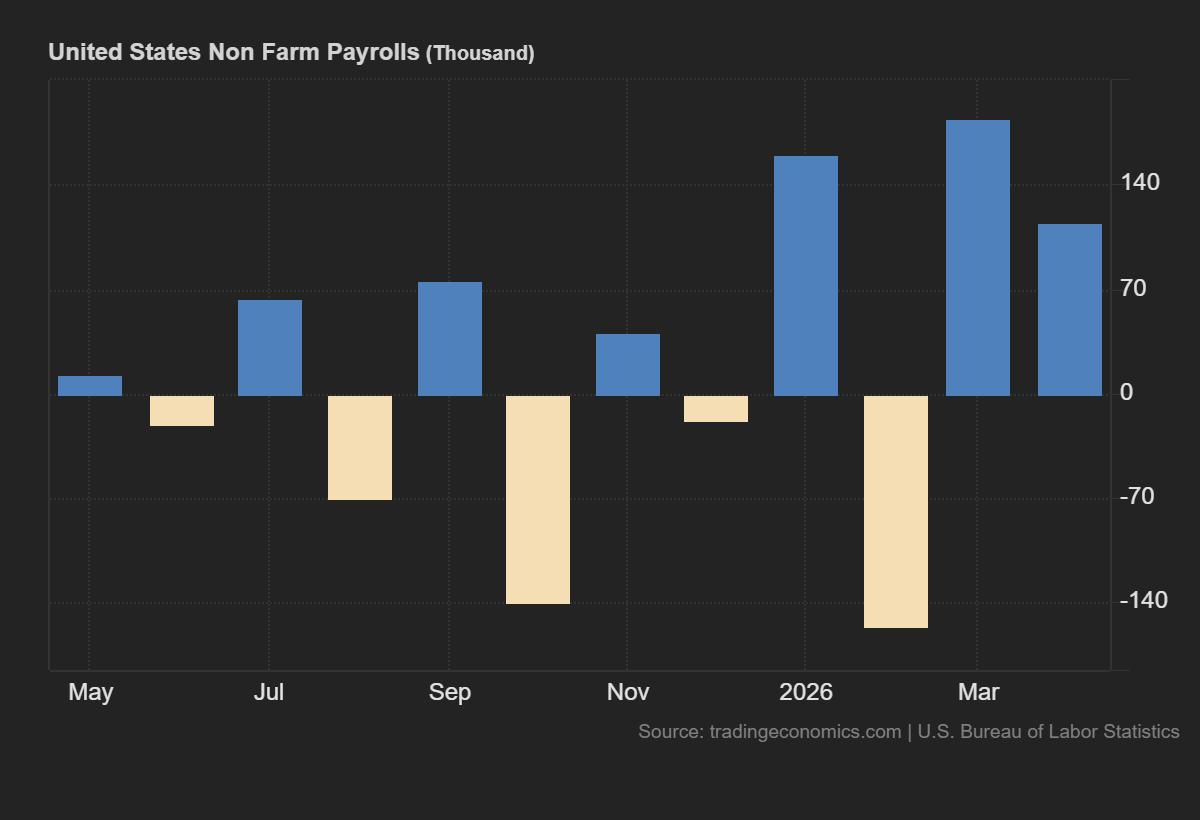

May’s NFP covering April was the first consecutive positive NFP in more than a year and indicated that the labour market in the USA might be resilient. March’s figure was also revised slightly up to 185,000. The consensus on 4 June was for about 85,000 for the next NFP but the actual release is almost certain to diverge from that one way or the other.

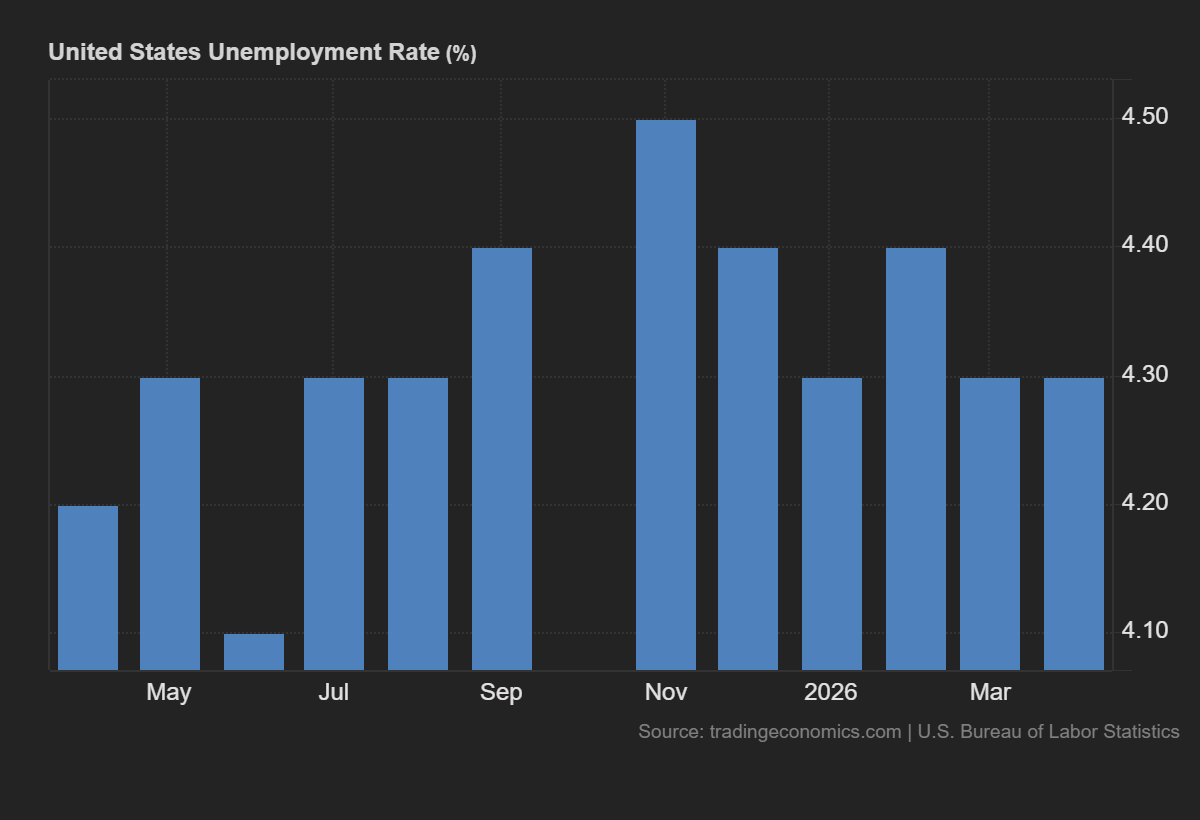

While the NFP proper has been more positive in the last couple of months, unemployment has remained more-or-less stable for some time:

Unemployment has clearly risen from the average in 2022 and 2023 but doesn’t show any immediate sign of pushing consistently much higher when considered with recent NFPs and demographic factors. A relatively decent job market – or at least certainly not as negative as had been expected in some quarters six months ago – is a positive factor for the Fed, giving it flexibility to hike rates if inflation continues to rise.

So far, there’s no immediate urgency for tighter monetary policy given that the worst effects of the Gulf conflict on American inflation now seem unlikely at least for now. The economic pressure on the American government to end the war even with less favourable terms is high. Expectations for the funds rate at the end of the year are about evenly divided between hold (46% according to CME FedWatch) and at least one hike (52%). Between the NFP on 5 June and American inflation the following Wednesday, traders will have plenty to chew on both for short-term movements and where the Fed’s heading.

Euro-Dollar bounces from support as the NFP approaches

Apart from continuing intrigue about a potential agreement in the Gulf, the focus for the euro recently has been on monetary policy. The ECB is nearly certain to hike its main refinancing rate to 2.4% on 11 June. Current expectations suggest a total of 2-3 hikes by the ECB before the end of 2026 while there’s still considerable uncertainty over whether the Fed will hold or hike once.

The price bounced again on 4 June from the likely support around $1.16 which coincides with the 23.6% weekly Fibonacci retracement. Volume has been significantly lower in the last few days, which is normal in the context of the upcoming NFP, American inflation and meeting of the ECB.

The 50 SMA from Bands around $1.17 is likely to cap gains in the immediate future but each of the other moving averages between there and the current price could also be important. There’s no indication of saturation, so the strength so far of the bounce might suggest further limited gains to come although these would be unlikely to continue if the NFP is again clearly stronger than the consensus.

Dollar-Yen nearing intervention area again

Dollar-yen’s recovery from last month’s intervention has continued in June so far with the price holding around ¥160. The latest intervention by the Japanese authorities was worth over ¥11 trillion but didn’t have any clear, lasting effect in shoring up the struggling yen. Divergence in monetary policy remains a key factor in the yen’s weakness while the Japanese economy’s dependence on imported raw materials also seems to make it more vulnerable to an extension or possible escalation of the Gulf conflict. Participants expect the BoJ to hike to 1% on 16 June despite inflation significantly below target.

‘The trend is (usually) your friend’ but the ongoing direction for dollar-yen seems less certain: another, maybe even larger, intervention certainly seems possible if the price holds around ¥160 for more than a few days. ¥156.50 is a possible support given that the price failed to break through there in late April and early May amid very long tails of several periods.

Although the golden cross of the 20 SMA above the 50 SMA from Bands can probably be ignored in the context, overall a significant retracement without a fundamental narrative remains questionable. Some technical retracement lower is quite likely sooner or later, though, especially if the NFP is weaker than expected, given the strong overbought signal from the slow stochastic, low volume accompanying the bounce over the last month and significantly lower volatility.

Author

Michael Stark

Exness

Michael has been investing since 2007 and trading CFDs since 2013. He favors considering both fundamental and technical analysis where possible, with a focus on swing and position trading.