Silver balances growth expectations and real yields ahead of ISM

Key takeaways

Silver enters the ISM Manufacturing session within a market increasingly focused on the interaction between growth resilience and restrictive monetary conditions.

Treasury yields remain elevated, the Dollar continues trading from a position of relative strength and industrial assets are searching for confirmation that cyclical activity can maintain momentum into the third quarter.

Silver occupies a unique position between monetary sensitivity and industrial exposure, making manufacturing data particularly relevant for participation dynamics.

The technical structure continues to reflect compressed conditions, suggesting investors remain cautious ahead of the latest manufacturing signal.

Silver enters a growth-sensitive phase

Silver begins the second half of the year inside a market environment that looks very different from the one investors faced only a few months ago.

Federal Reserve expectations have largely been absorbed.

Treasury markets have already repriced the implications of a higher-for-longer policy regime.

Inflation data have moderated, while economic activity continues showing evidence of resilience.

Markets are now attempting to determine whether growth can remain sufficiently stable to support cyclical assets despite elevated financing costs and restrictive monetary conditions.

Silver sits directly at the center of that discussion.

Unlike gold, whose behavior remains primarily influenced by reserve allocation and credibility considerations, silver continues responding to both industrial and monetary forces simultaneously.

That dual identity makes the metal particularly sensitive to shifts in economic expectations.

The ISM Manufacturing release therefore represents more than a traditional macro event.

It offers another opportunity for markets to assess whether industrial activity remains capable of supporting broader metals participation.

Consensus forecasts point to a slight moderation in manufacturing momentum, with ISM expected at 53.8 compared with the previous 54.0.

The distinction between moderation and deterioration matters.

For silver, growth stabilization can remain constructive even in an environment characterized by firm yields and a relatively resilient dollar.

Growth resilience has become the dominant transmission layer

Markets have spent most of the year focused on inflation, interest rates and central bank communication.

Those variables remain important.

Yet the dominant question entering the third quarter increasingly revolves around growth durability.

Economic resilience influences capital expenditure.

Capital expenditure influences manufacturing activity.

Manufacturing activity influences industrial metals.

Silver remains directly exposed to that transmission chain.

The metal participates in sectors linked to electrification, electronics, energy infrastructure and broader industrial investment trends.

As a result, investors increasingly evaluate silver through the lens of cyclical engagement rather than purely defensive positioning.

This explains why silver frequently diverges from gold.

Both metals remain sensitive to real yields.

Both metals respond to dollar movements.

Silver, however, also reflects confidence regarding future industrial activity.

This broader reaction function makes silver one of the clearest expressions of macroeconomic balance.

Markets are attempting to determine whether restrictive policy settings can coexist with a still-resilient growth environment.

Silver provides a useful framework through which to observe that interaction.

Treasury yields continue influencing positioning

Industrial exposure does not eliminate silver's sensitivity to monetary conditions.

Treasury yields remain one of the most important variables influencing precious metals participation.

Higher yields support the dollar.

Higher real yields increase the opportunity cost associated with holding non-yielding assets.

Silver remains exposed to this process.

The relationship has become increasingly visible following the Federal Reserve meeting.

Markets now understand the broad contours of the current policy regime.

What investors seek next is confirmation that growth conditions remain sufficiently healthy to justify ongoing participation in cyclical assets.

If manufacturing conditions continue stabilizing, silver may retain support from its industrial component even while yields remain elevated.

If growth expectations soften more materially, industrial participation could weaken further.

This balance between cyclical resilience and monetary restriction defines the current environment.

Silver continues operating precisely at that intersection.

Industrial resilience remains a structural theme

Silver's longer-term identity continues extending beyond traditional precious metals narratives.

Demand remains associated with sectors that are influenced by investment decisions rather than short-term inflation dynamics alone.

Electronics manufacturing.

Solar deployment.

Electrical infrastructure.

Energy transition projects.

Industrial modernization.

These trends remain structural in nature.

Markets therefore do not necessarily require accelerating global growth to maintain constructive long-term expectations.

Instead, investors increasingly focus on whether industrial activity can remain stable enough to sustain broader engagement across strategic sectors.

This distinction becomes increasingly relevant as markets move deeper into the second half of the year.

Industrial resilience does not imply aggressive expansion.

It implies continuity.

Silver continues benefiting from exposure to that continuity.

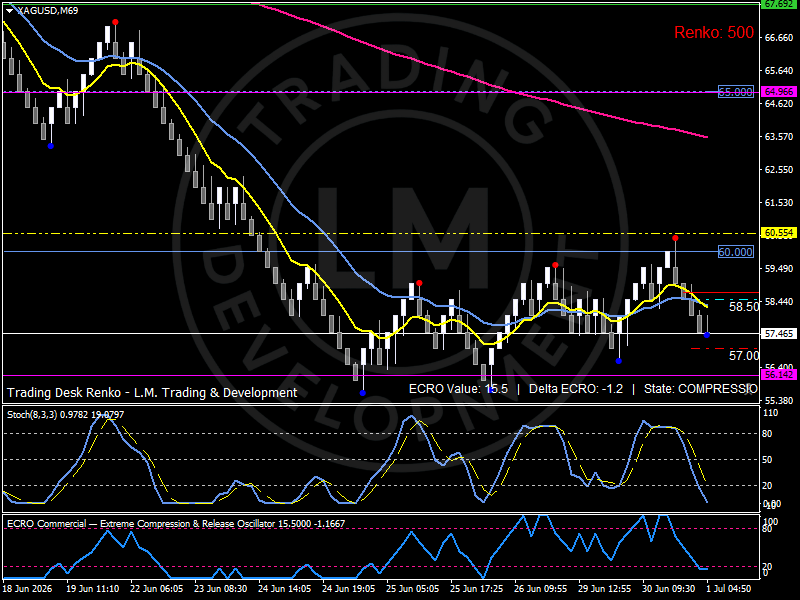

Technical structure: Silver remains trapped inside compression

The technical picture reflects a market waiting for confirmation.

The Renko framework shows that silver has undergone a meaningful repricing process during the second half of June before transitioning into a more balanced environment.

Participation conditions remain subdued.

ECRO currently stands near 15.5, while Delta ECRO remains marginally negative.

The system continues operating in a COMPRESSION state.

This combination suggests investors remain cautious rather than aggressively directional.

Momentum indicators have returned toward lower participation zones, highlighting a reduction in conviction following previous liquidation phases.

Price continues rotating around the 58.50 participation pivot, which has become the main equilibrium point between stabilization and renewed downside pressure.

Immediate resistance develops near 60.00, followed by the broader participation corridor around 60.55.

Support remains concentrated around 57.45, while a deeper structural zone extends toward 57.00 and 56.15.

The overall configuration remains consistent with consolidation.

Markets appear increasingly willing to wait for additional information before committing toward a more persistent directional phase.

Today's ISM release may provide that information.

Bird's eye view

Silver currently operates inside a growth-sensitive market where cyclical resilience and restrictive monetary conditions remain closely interconnected.

Federal Reserve policy has largely been repriced, while Treasury yields continue exerting pressure across precious metals.

The next layer of market attention has shifted toward growth validation.

Structurally, silver remains centered around the 58.50 participation pivot, with resistance developing at 60.00–60.55 and support concentrated around 57.45–57.00.

The dominant variables remain ISM Manufacturing, real yields, Treasury positioning, industrial resilience and broader metals participation.

Outlook

Silver enters the ISM session inside a compressed environment where investors are evaluating whether resilient growth conditions can coexist with restrictive monetary settings.

Manufacturing activity has become increasingly important because it offers insight into the durability of industrial demand expectations.

The current technical structure remains cautious but balanced.

Participation remains limited.

Conviction remains moderate.

The next directional phase will likely emerge through the interaction between growth conditions, industrial resilience, Treasury yields and broader metals engagement.

For now, silver continues reflecting one of the most important macro themes of the current cycle: the relationship between economic durability and monetary restraint.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.