Possible divergence between BoE and ECB could commence today

After a muted reaction to a surprisingly more hawkish vote share from the Fed meeting yesterday, eyes are turning across the Atlantic towards the Bank of England and the European Central Banks interest rate decisions today. Both banks recognised back on March 19th, when they last met, that the conflict in Iran would have a material and almost immediate impact on inflation.

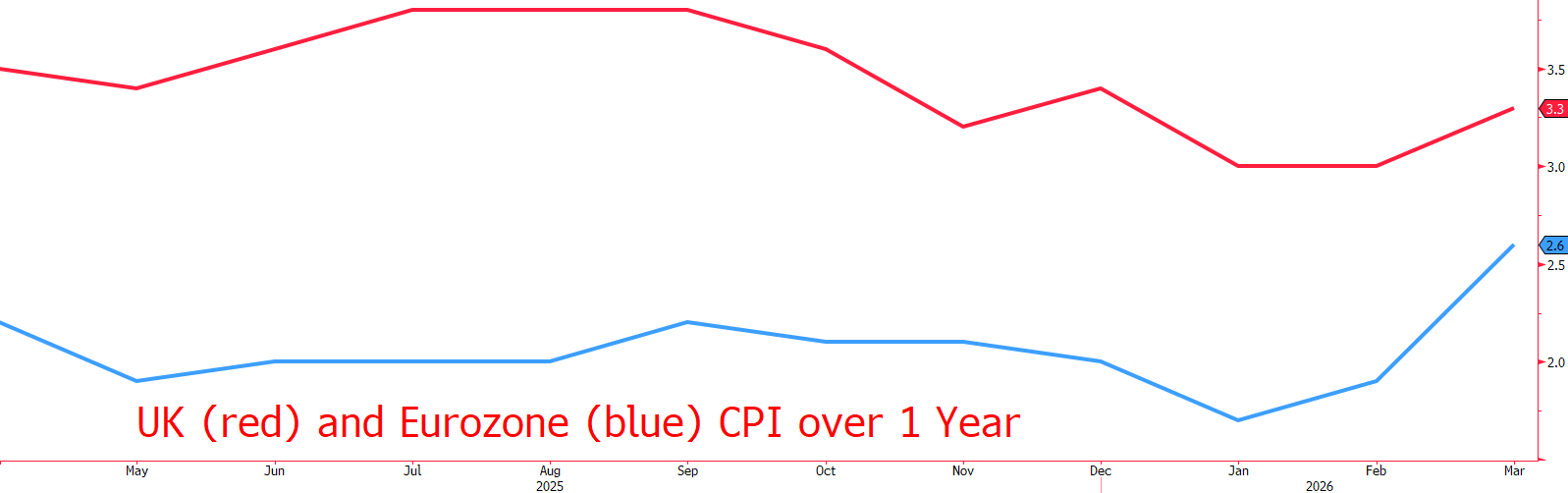

The BoE stated that forecasts suggested CPI between 3 and 3 ½ % would be likely over the next few quarters, the ECB stated that Eurozone inflation was likely to average 2.6% over the year.

Since then, Oil prices have grinded higher after an overdone depreciation caused by overly optimistic hopes of a swift end to the war. UK inflation printed its fastest one month increase since April 2025 whilst Eurozone CPI accelerated its most since 2022. Banks are not clairvoyant, but the lack of any end in sight between the US and Iran does make these initial estimates seem forlorn.

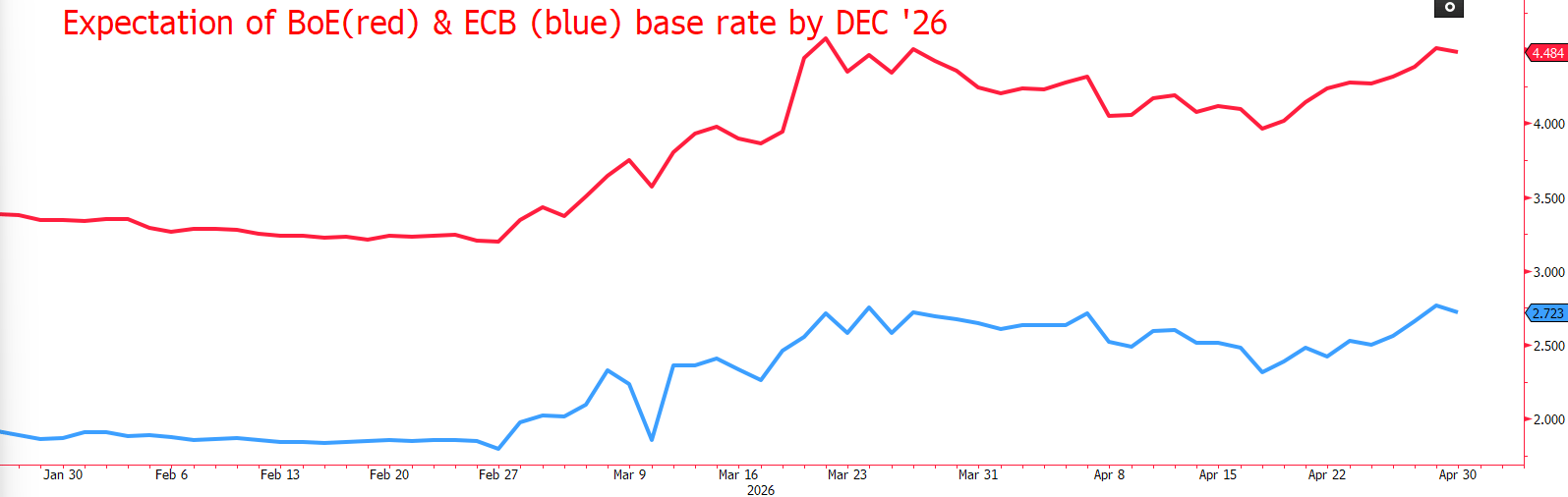

Whilst it is very unlikely that either Central Bank will move their main rates today, there is the possibility of a divergence in guidance that could greatly influence GBPEUR in the near term. Both banks are expected to hike rates at least three times this year, looking at futures pricing, which seems a tall order given the persistently weak growth that is currently underpinning both economies.

The BoE seems like the one most likely to blink during their statement today, with Governor Bailey repeatedly pouring cold water on suggestions of multiple rate hikes this year. Moreover, the day prior to the beginning of the conflict, the BoE was expected to drop rates twice this year, whilst the ECB was expected to hold, or possibly even hike should unemployment remain so low in the zone.

Another concern of the BoE that the ECB does not suffer is that Gilt yields are starting to enter painful territory. The 30 yr Gilt is almost 60bps higher since the start of the war, a retreat that threatens to start punishing the Pound should this velocity be maintained. Indeed, after the surprisingly hawkish tone the BoE took at the last meeting spooked Gilt traders, Bailey had to hold a press conference to state that the Bank was in no rush to tighten conditions.

European officials have been more staid in their comments, although undeniably have advantages that their British counterparts simply cannot boast. Today could end similar to yesterday’s Fed, savouring of disappointment, or, it could mark the beginning of a divergence that could set the tone for GBPEUR going forward.

Author

David Stritch

Caxton

Working as an FX Analyst at London-based payments provider Caxton since 2022, David has deftly guided clients through the immediate post-Liz Truss volatility, the 2020 and 2024 US elections and innumerable other crises and events.