March inflation numbers in Hungary and the Czech Republic may restore rates momentum

Inflation in the eurozone and Poland reached record highs in March, surprising markets massively. The experience of recent months suggests that we can expect a similar story in Hungary and the Czech Republic. Despite the fact that market expectations have shifted significantly upwards in recent weeks, we believe there is still room to grow.

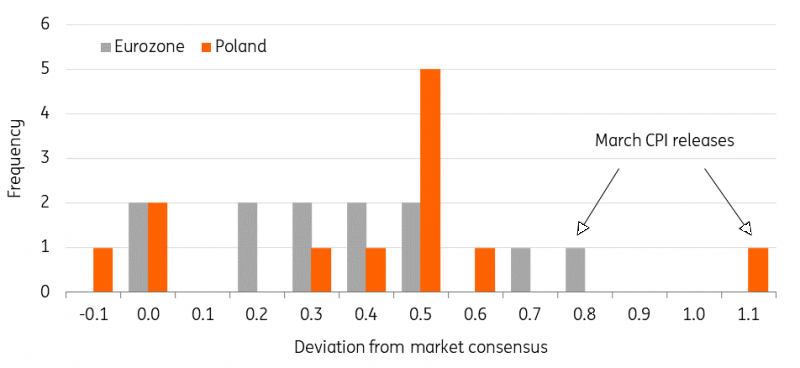

Eurozone and Poland see record upside surprise in inflation for March

Recently-released March inflation data in the eurozone and Poland showed a massive surprise compared to market expectations. In the eurozone, year-on-year inflation amounted to 7.5% from the previous 5.9%, surprising the markets by 0.8pp. In Poland, March inflation reached 10.9% from the previous 8.5%, beating market expectations by 1.10pp. In both cases, the latest readings and the market surprises reached multi-year, or even all-time highs.

March inflation numbers surprised massively

Source: Refinitiv, ING

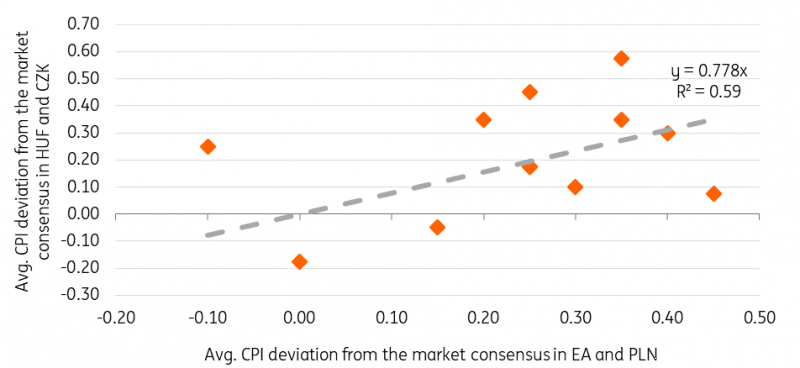

The same story can be expected in Hungary and the Czech Republic

In the coming days, inflation figures will be published in Hungary (8 April) and in the Czech Republic (11 April). Based on the experience of recent months and the nature of common inflationary pressures, we believe that we may see a significant upside surprise in inflation in these countries as well. March is the first month fully affected by the Ukrainian conflict, higher energy, oil and food prices. Added to this are the Central and Eastern Europe region-specific inflationary pressures in the core component, which together make inflation hard to gauge these days.

In Hungary, the market consensus expects an increase from 8.3% to 8.8%. Our economist Peter Virovacz in Budapest expects 9.1%, but even higher figures are realistic in his view. In the Czech Republic, the market consensus has not yet been published, but we believe that expectations will be in the range of slightly above 12%. In our view, however, it is not impossible that inflation will be closer to 13%.

Eurozone and Polish figures imply surprises in Hungary and the Czech Republic

Source: Refinitiv, ING

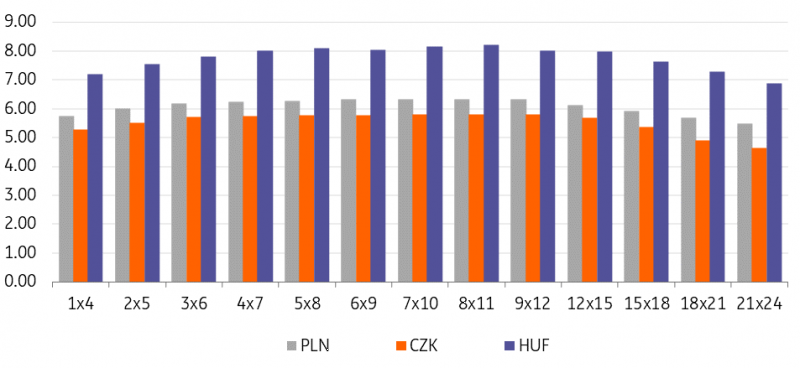

Market implied policy rates in Central and Eastern Europe

Source: Refinitiv, ING

Read the original analysis: March inflation numbers in Hungary and the Czech Republic may restore rates momentum

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.