Japan’s stronger GDP and limited gas price risks support a BoJ rate hike in June

Japan’s GDP expanded more than expected in the last quarter of 2025, and household spending on goods and private services remains on track in January. With retail gasoline prices contained, the Bank of Japan is likely to delay any rate hike to June, standing pat in April.

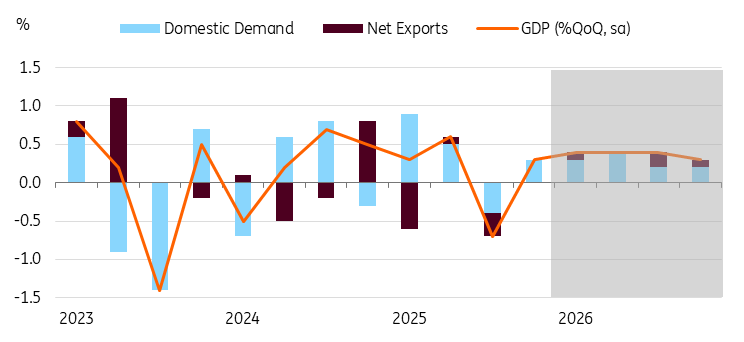

GDP revised up from 0.2% quarter-on-quarter to 1.3% annualised

The upward revision to Japan’s fourth quarter GDP was mostly due to strong business spending (1.3% vs flash 0.2%). Private consumption also rose a bit to 0.3% (vs flash 0.1%). Government spending is expected to rise in the current quarter, while energy subsidies and strong wage growth are set to boost private consumption. Inventory was a drag on growth for the second straight quarter. But we expect the restocking cycle to reverse and begin contributing positively to the current quarter.

Downside risks increased, but we expect a steady growth ahead thanks to government support

Source: CEIC, ING estimates

Household spending dropped unexpectedly, but underlying trend appears to remain firm

Household spending unexpectedly dropped 1.0% year-on-year in January (vs -2.6% in December, 2.4% market consensus). The decline was mainly driven by significant declines in housing (-12.3%) and education (-22.6%). Meanwhile, spending increased in food (1.5%), furniture (13.5%), and culture and recreation (10.8%). Despite the soft headline, underlying spending on goods and private services still seems resilient. Combined with solid wage data (real wage growth of a 1.4% YoY in January) from yesterday, recent trends support our view that private spending is expected to remain firm in the current quarter.

Gasoline price hikes are limited despite the heavy dependence on Middle East oil

Recent global oil price increases have had a limited impact on domestic inflation, largely due to government measures. Gasoline prices rose 2.4% between the end of February and 9 March, according to a price comparison website. There has been an acceleration in the last two days, but no queuing at gas stations, indicating that market sentiment remains controlled.

The government has subsidised petroleum companies to stabilise prices. It also abolished the gasoline “provisional tax rate” at the end of last year. These measures are helping to limit gasoline price hikes in Japan.

Japanese authorities announced this morning that they are also prepared for a potential release of strategic oil reserves. Public and private reserves could cover domestic demand for about 254 days; any release would likely be coordinated with G7 partners.

It is a close call, but we see June is a possible time for the next hike

Despite earlier rate hikes, the economy seems to be performing well, and financial conditions remain accommodative. Thanks to cooling inflation, combined with steady wage growth and positive wealth effects, consumer purchasing power has improved recently. Combining all these factors, the Bank of Japan will likely continue its policy normalisation.

BoJ action is unlikely later this month due to geopolitical uncertainty. Also, the BoJ will watch wage growth and inflation trends. As mentioned earlier, energy inflation is somewhat tame in Japan. This should give the BoJ time to examine how recent developments have affected inflation. We believe the BoJ would downplay supply-shock-driven inflation if it lasts only for a short time. As such, we believe that the BoJ would like to see solid wage growth continue with results from the Shunto wage negotiations. More importantly, tracking April inflation, especially service prices, will be quite important as companies tend to adjust their prices in the first month of the fiscal year.

Overall, the probability of a rate hike in April is likely to rise if initial Shunto results exceed expectations. Additionally, we will pay close attention to comments from BoJ officials, as their communications often provide indications regarding potential rate hikes ahead of policy meetings.

Read the original analysis: Japan’s stronger GDP and limited gas price risks support a BoJ rate hike in June

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.