Hotter US inflation numbers could further bolster Fed hike bets – Preview

- Middle East tensions keep inflation risks elevated.

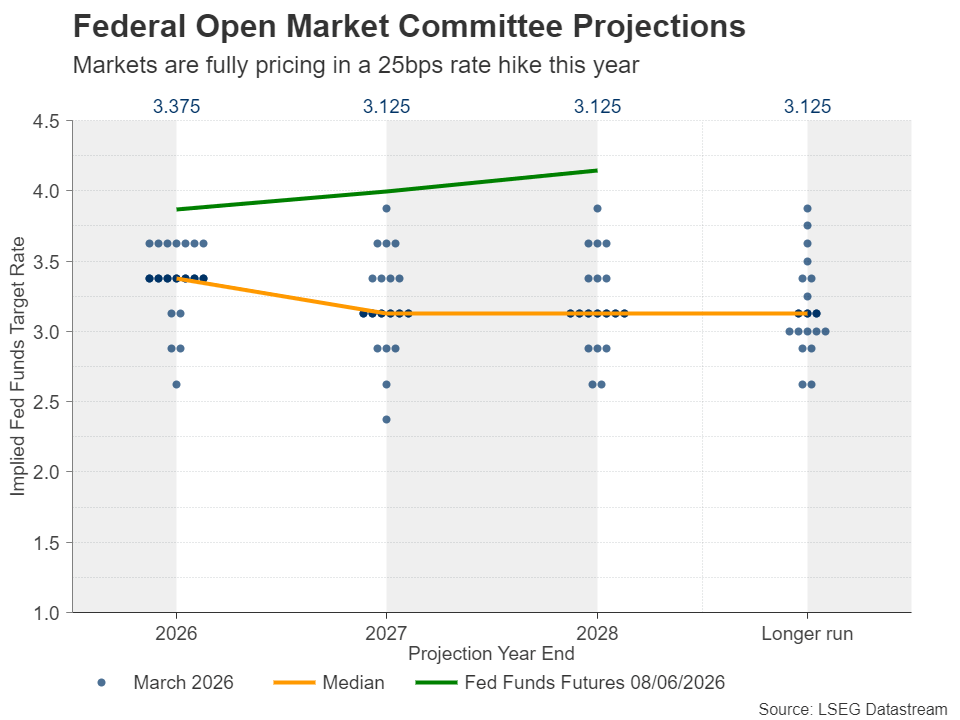

- Fed hike fully priced in by year end amid strong NFP report.

- US CPI data on Wednesday (12:30 GMT) to enter the spotlight.

- Further acceleration in inflation could drive the dollar higher.

Middle East tensions and NFP data bolster Fed hike bets

With tensions in the Middle East escalating once again over the weekend, hopes vanished that the Strait of Hormuz will reopen at some point soon, giving room to heightened inflation concerns as oil prices opened this week with a positive gap. Although it pulled back following headlines that Iran ended its military operations against Israel, the pullback was far from reflecting hope about permanent ceasefire soon. After all, Iranian officials warned that they would resume hostilities if attacks against Lebanon continue.

On Sunday, Iran fired missiles at Israeli military targets in retaliation for Israel’s attacks on Lebanon. Israel responded by attacking Iran, defying US President Trump’s call for restrain. The new hostilities came on top of a robust US jobs report on Friday, keeping inflation fears elevated and allowing investors to bring forward their Fed rate hike bets.

According to Fed funds futures, a quarter-point rate hike is now fully priced in for this year, the probability of it being delivered in September resting close to 50%. With the upcoming meeting being the first of the new Chair, Kevin Warsh, it is unlikely that the Fed will press the hike button before September. After all, Warsh was appointed by US President Trump, on the premise that he holds a less hawkish view than his predecessor Jerome Powell.

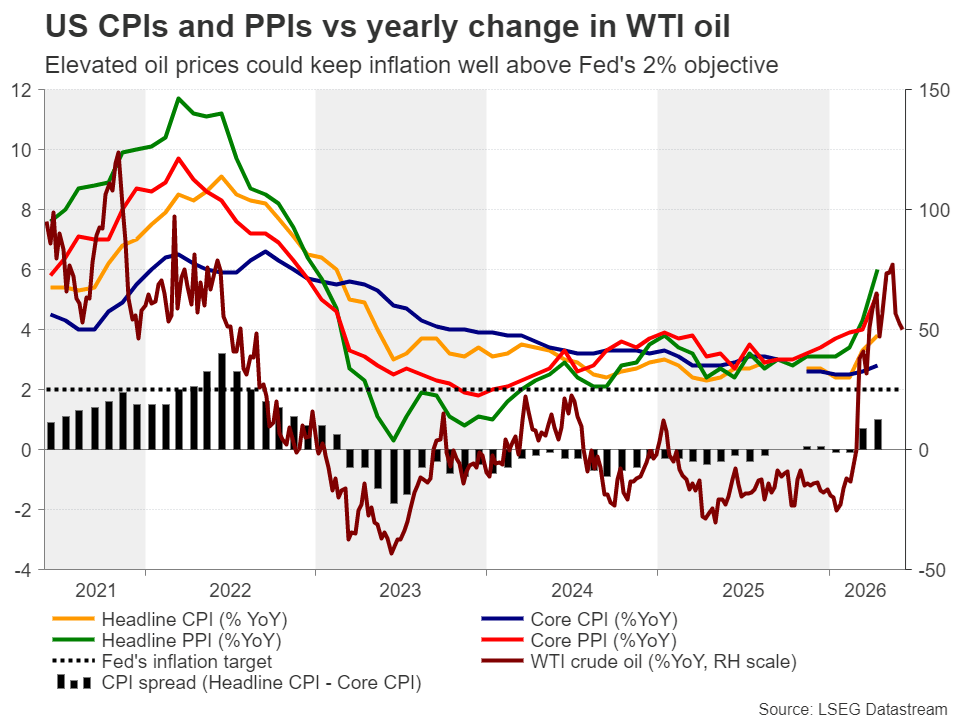

US CPI and PPI data could reveal further acceleration

On Wednesday, the spotlight is likely to turn to the US CPI data for May, while on Thursday, the PPI figures will be released. In April, the headline CPI rate accelerated to 3.8% y/y from 3.3% amid the surge in oil prices due to the Middle East tensions, and although the rise in the core rate was smaller, the headline PPI rate surged to 6%. This means that products that were produced in April were set to arrive on store shelves at higher prices over the following months.

What’s more, although the year-on-year rate of change of WTI crude oil declined lately, it is hovering at April levels, which leaves little room for a material slowdown in inflation. All this poses upside risks to this week’s data. Indeed, the forecasts point to further acceleration, with the headline CPI rate expected to climb to 4.2% y/y from 3.8%, and the core to tick up to 2.9% y/y from 2.8%.

Another month of hotter-than-expected prints could drive the probability of a September hike higher, thereby pushing Treasury yields higher and adding more fuel to the dollar’s engines. At the same time, gold could extend its slide as the opportunity cost for holding the precious metal increases.

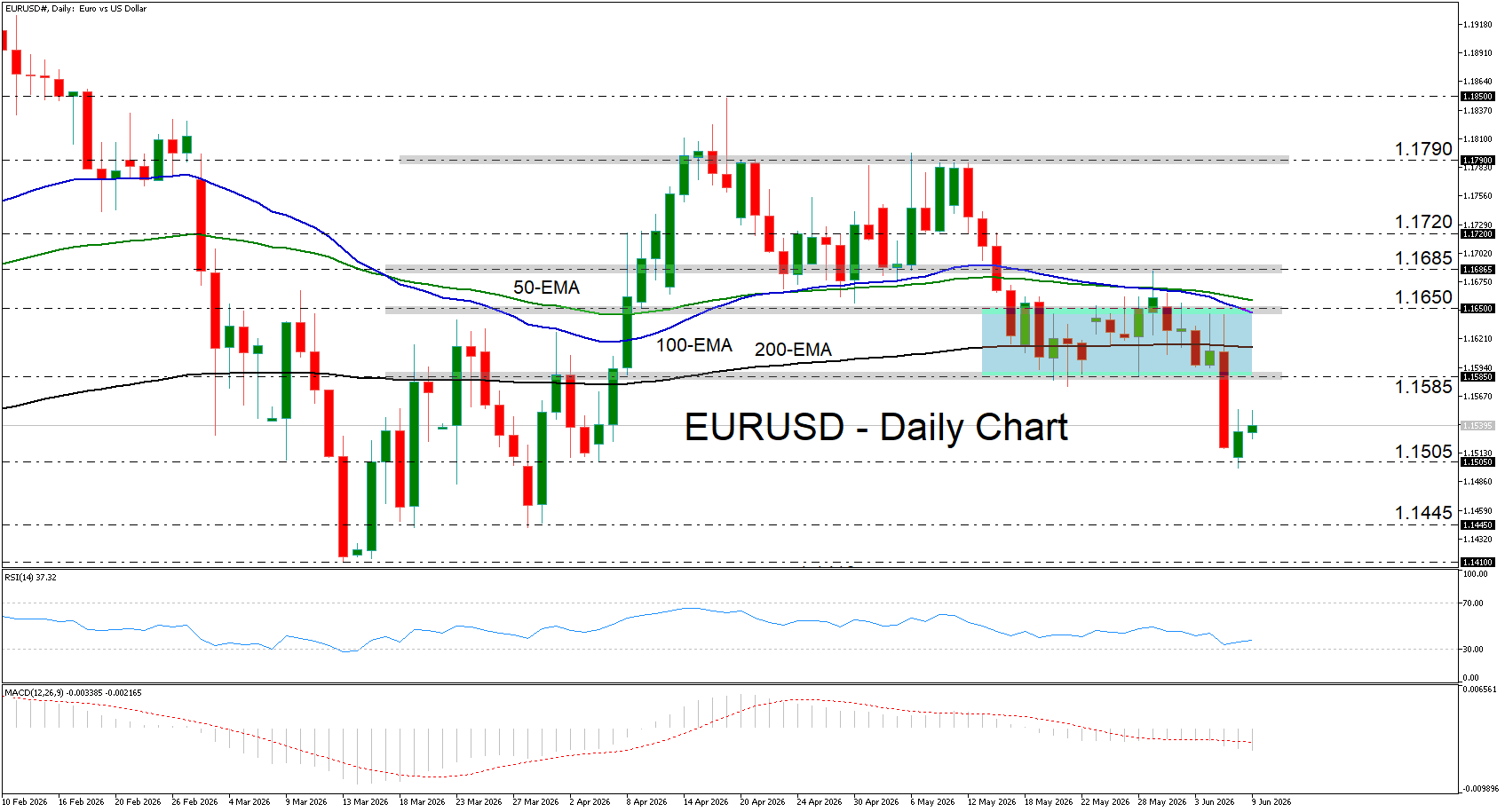

Euro/dollar rebounds, but outlook remains bearish

From a technical standpoint, euro/dollar tumbled on Friday following the better-than-expected NFP report, breaking below the 1.1585 barrier and hitting support near the 1.1505 zone. Although the pair is now recovering, the short-term outlook remains negative.

Even if the rebound stretches a bit more, the bears could re-charge from near the 1.1585 zone and shoot for another text near 1.1505. A break lower could set the stage for declines towards the 1.1445 area, marked by the lows of March 30 and 31. On the upside, a clear close above 1.1585 could signal the pair’s return within a sideways range, while a decisive move above 1.1650 may shift the outlook to bullish.

Author

Charalampos joined Trading Point in August 2022 as a senior market analyst. He has extensive experience in analyzing financial markets, gained through a decade-long career, with his primary focus being on the currency market.