Gold investors, don’t panic – Gold’s rally is almost there

The logic behind the recent gold correction has been simple: the Middle East conflict has made the oil prices surge, which is highly inflationary. Higher inflation readings should in turn force the Fed and other countries’ central bankers to increase the interest rates, thus provoking an economic slowdown or even a recession as a result. But this would just be the beginning of the precious metals’ rally. Here is why.

Iran-Israel war

In my previous publication titled “Why I Think High Oil Prices Are Here To Stay”, I wrote that it would be hard to replace Iranian oil, while it is likely that the war in the Middle East would last for more than “four to five weeks” as originally planned by the White House administration. The Middle Eastern countries that are members of OPEC+ would be unable to drill more because they are also affected by Iranian airstrikes, while sanctions are imposed against Russia and its energy imports, the third largest oil producer.

But why do I think that the conflict between Israel and Iran would last for a while? To start with, according to The Guardian’s Patrick Wintour, there are three ways in which the conflict between Iran and Israel might end, namely “a long and drawn out conflict ending with Iran’s capitulation; a unilateral declaration of victory by Trump; or an agreement, large or small, regional or bilateral, sweeping or narrow, that ends the fighting.” It seems, however, that Iran is highly unwilling to capitulate or reach a peace agreement that the US and Israel would approve of. On 11 March, the 12th day of the Israel-Iran war after many Iranian government officials have already been killed and much of the country’s infrastructure has been destroyed, Iran’s President Masoud Pezeshkian, wrote “The only way to end this war — ignited by the Zionist regime and U.S. — is recognizing Iran’s legitimate rights, payment of reparations, and firm international guarantees against future aggression”. By “Iran’s legitimate rights” Pezeshkian also meant Iran’s nuclear enrichment right, which the US and its allies have been trying to prohibit for decades. Also, it is the first time that Tehran speaks of reparations, a condition that neither Israel nor the US would likely agree to in the near future. Therefore, in my view, neither Iran’s capitulation nor the Iran-Israel peace agreement is likely in the near future. As concerns, the second option that Trump declares victory on Iran, according to The Guardian, “that presupposes Iran is willing to go along with this pretence”. But Iran is unwilling to do this either because “a harder, more nationalist Islamic Revolutionary Guard Corps” have come to power instead of the killed Ali Khamenei, the country’s supreme leader. That is why in my view the quick end of the war is not very likely.

But what would the prolonged war between Israel and Iran lead to? Interestingly, it would not only lead to substantially lower oil supplies. It would also disturb the shipping and airfreight, thus leading to deficits of many types of products, including food, water, textiles and a number of commodities, including aluminum. Also, between 30% and 35% of global nitrogen fertilizer passes through the Strait of Hormuz. Also, there were airstrikes on US allies, including the UAE, Oman, Kuwait and Qatar, which led to logistics issues in these countries. Consumers in many Middle Eastern countries panic bought essentials, which in turn led to empty shelves in supermarkets. Many analysts believe that these problems might spread to other countries. As I have mentioned above, there are supply bottlenecks. Not only oil and natural gas but also other commodities and even fertilizers fail to reach their destinations. What this means is that it would get much more expensive to grow food, to produce and even transport various goods, which would lead to supply deficits and even higher inflation readings.

The 1970s Oil crisis

The current situation reminds me of the 1970s oil crisis when an embargo was imposed by Arab nations against the collective West in response to their support of Israel. This led to prolonged oil deficits in Europe and the US. Obviously, this led to much higher inflation readings and a very hawkish Fed as a result.

Below I have prepared the inflation and the interest rate histories.

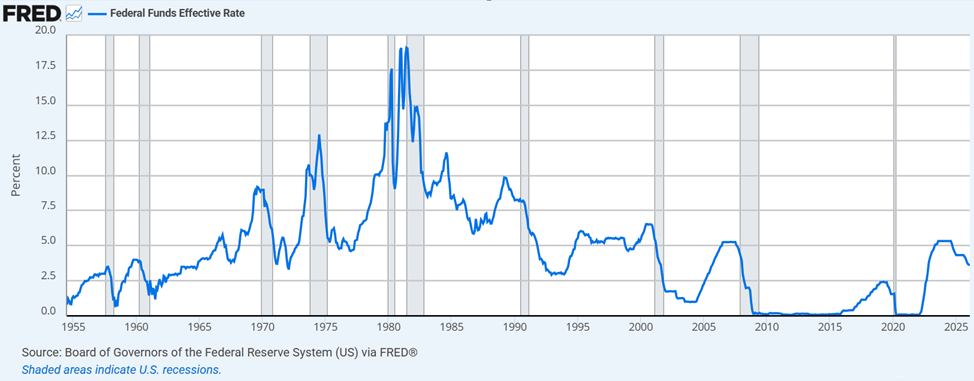

As you could see from the two graphs below, the 1970s have been marked with higher Fed’s interest rates, several recessions and higher inflationary readings.

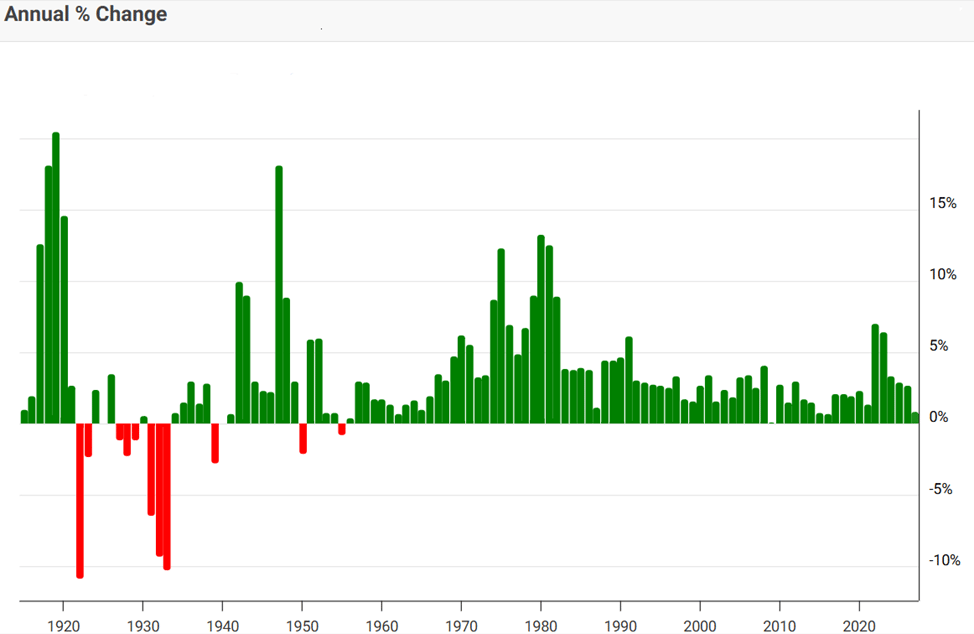

The graph below shows the US inflation rate history. As you could see below, US inflation was at some point even close to 20% per year.

Inflation rate history

Source: Macrotrends

The graph below shows higher interest rates during the 1970s. These were raised many times following higher oil prices and higher inflationary readings as a result. Therefore, there were three recessions -shaded in grey on the graph- in the 1970s.

Federal Funds’ rate history

Source: Fed

But how about gold? How did it respond to the higher rates for longer? Because we all know that tighter monetary policies suppress prices for precious metals. However, during this time period this did not happen.

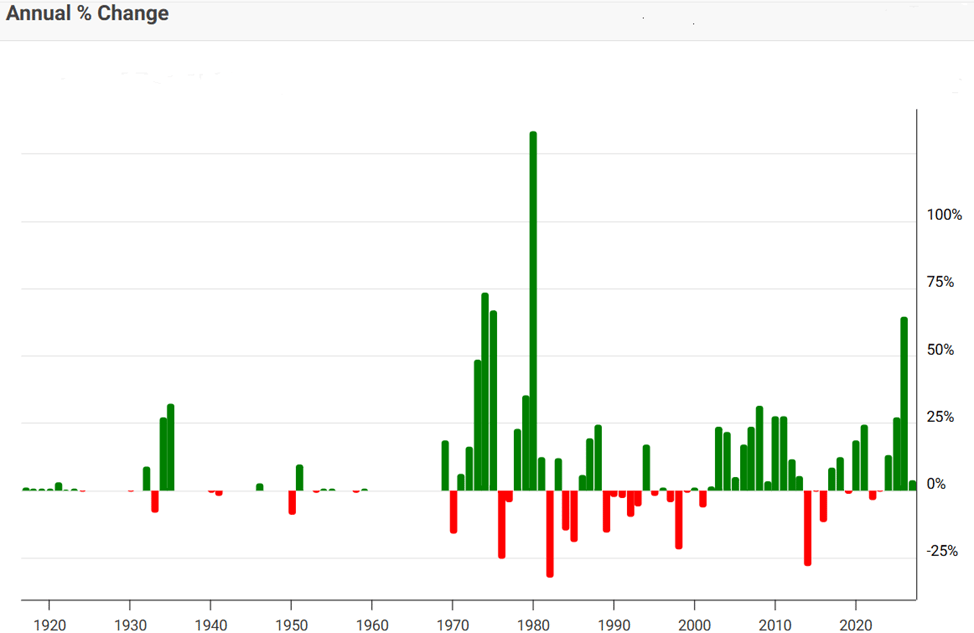

In fact, the 1970s has so far been the best period for gold prices. This could be partly explained by President Nixon’s decision to abandon the gold standard. In 1971 Nixon ended the direct convertibility of the USD into gold, which ended the Bretton Woods system and led to a run on US gold reserves. Yet, the gold prices did not only soar in 1971. In 1979 when there was a revolution in Iran and oil prices surged, gold prices soared as well.

Source: Macrotrends

Source: Macrotrends

As Mark Twain once famously said,“history doesn't repeat itself, but it often rhymes” –. In other words, I think that a similar situation might actually happen now. Here is why.

The Fed’s policies

There are several scenarios of what may happen now. First, it is still possible that the conflict between Iran and Israel may not last for a long time. After all, the US and Israel might reach a peace agreement with Iran. Alternatively, the US might win the war with Iran. The Strait of Hormuz might be unblocked as a result and even Iranian oil supplies might recommence. Until this happens, the Fed might take the “wait and see” approach instead of lifting the rates straight away. This way, the US economy would manage to avoid a crisis. As I have explained above, I personally highly doubt that the Israel-Iran war would end in the near future. So, this scenario is not very likely.

However, what if the US-Iran war lasts for longer? According to Saudi Arabia, if the war between Iran and Israel lasts for longer, by late April oil prices might surge to $180 per barrel, a situation we have not witnessed for decades. In this case, the Fed would raise the interest rates, thus provoking a recession. Higher rates and the resulting recession would initially provoke a market shock, a higher US dollar, and a selloff across many asset classes, including gold and silver. But in the long run the situation is bullish for gold.

Why is the situation bullish for Gold in the long run?

As I have mentioned above, my base-case scenario is that in the long run if the Fed raises the interest rates, it would provoke a recession. This means that most US macroeconomic indicators, including retail sales and employment figures, would deteriorate. After these indicators get more critical than inflation figures, the Fed would get dovish. How dovish it would get depends on the scale of the crisis the American economy would experience. If there is an economic decline similar to the one observed during the Covid-19 pandemic or the 2008-2009 Great Recession, the Fed would have to decrease the interest rates to zero and even launch the quantitative easing (QE) program to make the US economy recover. Monetary easing is highly bullish for gold and other precious metals simply because it involves money printing and leads to the USD’s devaluation.

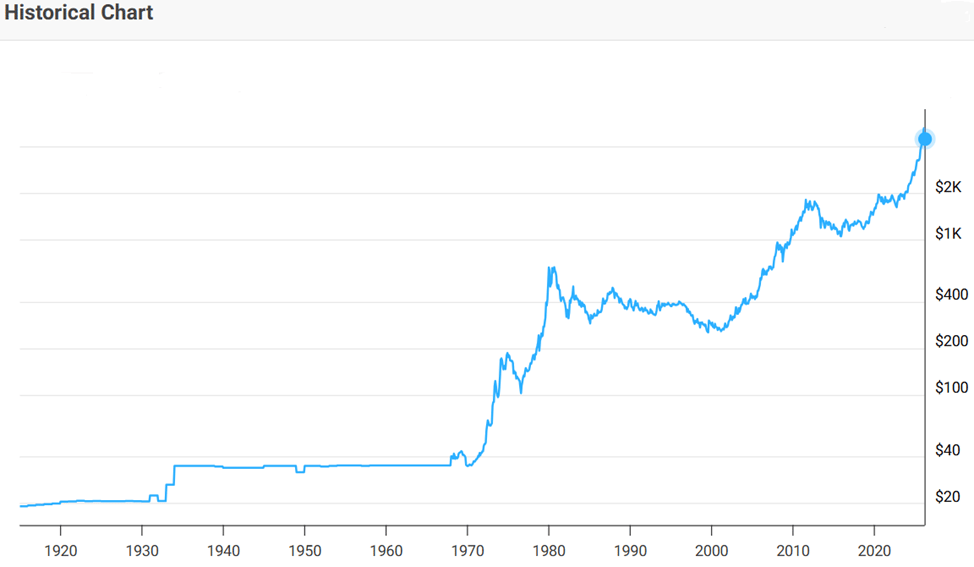

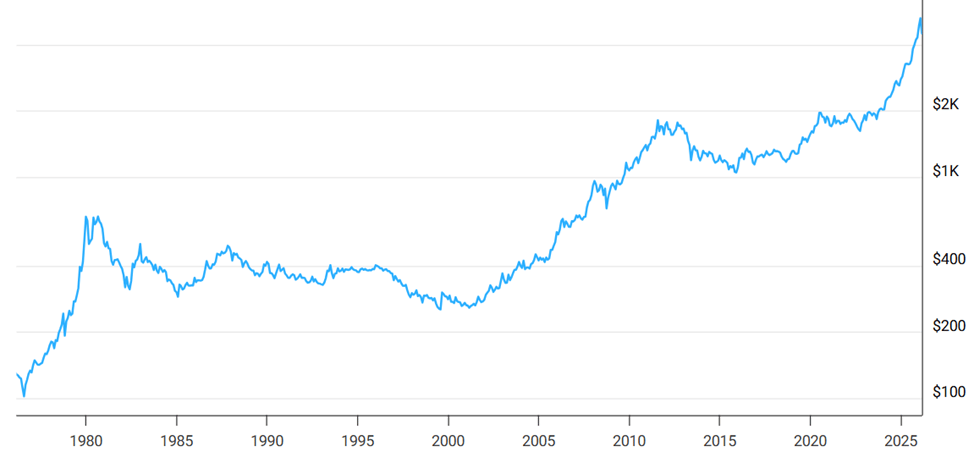

Let me illustrate how gold performed both in 2008-2009 and during the 2020 Covid-19 crisis.

Source: Macrotrends

It sold off initially in 2008 when there was market panic and the US dollar strengthened only to surge to new all-time highs. The gold prices’ peak was in 2011 when gold prices reached more than $1800 per ounce, over and above the $700 price gold traded for in 2007. During the 2020 pandemic, gold prices corrected somewhat, falling from the $1550 reached before the lockdowns to about $1475 per ounce after the US dollar strengthened. Later in 2020 gold prices surged to $2000. They even reached $5500 per ounce at the beginning of 2026, as a result of the non-stop rally after 2021. I believe the situation would repeat itself now.

Downside risks

The downside risks for gold are simple. First and foremost, is that the Fed’s tightening would last longer than originally expected. However, this would lead to a more serious recession and even stronger measures to get the economy going. Obviously, this is even more bullish for gold prices in the long run.

Another risk is that of the Iran-Israel war ending earlier than originally forecasted. However, this would make my bullish scenario for more rates cuts intact. The US economy would not even have to enter recession first to make the Fed ease its monetary policies. If we assume that the oil price surge resulting from the conflict is very short-lived, the Fed would only postpone its rate cuts for a short time period. So, the easing cycle would start earlier than the markets now expect, given the Iran-Israel war, which would be bullish for gold.

Another downside risk, in my view, is investors rushing to buy high-risk assets if the recession gets postponed. So, the demand for safe-haven assets like gold would not be as high as during turbulent times.

Conclusion

It seems to me that the gold rally halt is temporary. Even from a technical perspective, no rally can last forever non-stop. Gold prices, however, have a good potential to rally further thanks to the likelihood the Fed’s potential tightening would provoke a recession. The resulting monetary easing would eventually raise the gold prices. There are multiple ways in which long-term investors can benefit. Some may want to buy gold ETFs, others may want to choose reliable gold miners that also pay dividends. I am not personally in favor of buying so-called “paper gold”, either in the form of options and futures or even ETFs, simply because there is much more paper gold than physical gold. According to Global Coin’s web-site, the paper-to-physical gold ratio is cited to be between 100-to-1 and 250-to-1. As concerns gold miners, they do indeed offer plenty of potential gains but a lot of company-specific research, including that of financials and the management, is needed. In my opinion, buying physical gold is much safer because there is no counterparty risk even though physical gold means much higher storage costs.

Author

Anna Sokolidou

Independent Analyst

A research analyst, a freelance finance writer and an economics teacher looking for interesting investment opportunities. I have been investing for years. I am mostly interested in writing about commodities, precious metals and large corporations.