Gold enters payroll credibility test as labor-market expectations soften

Key takeaways

Gold enters payroll day inside a market increasingly influenced by labor-market expectations, Treasury positioning and the evolving credibility of the Federal Reserve policy path.

Recent economic releases suggest growth is moderating rather than deteriorating, while weaker labor indicators have encouraged investors to reassess the trajectory of interest rates beyond the summer.

Real yields remain elevated, the US Dollar retains underlying support and participation conditions across precious metals continue reflecting cautious positioning ahead of Nonfarm Payrolls.

The current technical structure remains balanced, with gold rotating around the 4,075 participation area as investors await confirmation from employment data.

Gold enters a credibility phase ahead of payroll validation

Gold approaches the June employment report inside a macro environment that is becoming increasingly sensitive to labor-market signals.

The latest ISM Manufacturing survey softened to 53.3 from 54.0, suggesting that activity continues to expand but at a slower pace. Earlier labor indicators also pointed toward a moderation in hiring conditions, reinforcing the perception that the economy may be transitioning toward a more balanced growth regime.

For gold, this matters because labor conditions represent one of the most important transmission mechanisms influencing monetary policy expectations.

A resilient labor market supports the higher-for-longer narrative.

A gradual cooling in employment conditions encourages markets to consider a less restrictive trajectory further ahead.

Gold increasingly trades within that framework.

The metal has spent much of the year responding to changes in real yields, Treasury repricing and shifts in the perceived credibility of the Federal Reserve's commitment to maintaining inflation stability.

Payrolls therefore represent more than a monthly economic release.

They offer markets an opportunity to validate whether recent signs of moderation remain isolated events or the beginning of a broader transition in growth dynamics.

Consensus expectations currently point toward 114,000 jobs, compared with the previous 172,000, while the unemployment rate is expected to remain stable at 4.3%.

That configuration suggests investors are searching for confirmation rather than deterioration.

The distinction remains important.

Gold does not necessarily require a sharp slowdown to maintain participation. It benefits from environments where policy expectations become less restrictive while economic activity remains sufficiently stable to preserve confidence in broader financial conditions.

Labor expectations are becoming the dominant transmission layer

Inflation dominated market narratives during much of the previous year.

More recently, labor-market conditions have emerged as the central variable shaping expectations across asset classes.

Employment influences income growth.

Income growth influences consumption.

Consumption influences inflation persistence.

Inflation expectations influence Treasury yields.

Treasury yields influence precious metals participation.

Gold remains closely connected to that transmission chain.

Recent labor data have encouraged markets to reconsider the degree of policy restraint required over coming quarters.

A softer labor backdrop could reduce upward pressure on real yields.

Lower real yields generally improve participation conditions across non-yielding assets.

Conversely, a stronger-than-expected payroll report would likely reinforce the idea that the economy remains capable of absorbing elevated financing costs.

Such an outcome could support Treasury yields and maintain pressure across precious metals.

Gold therefore enters payroll day acting as a macro barometer.

Rather than responding purely to inflation, it increasingly reflects investor confidence in the sustainability of the current policy regime.

That behavior aligns with gold's evolving identity as a credibility asset.

Treasury positioning remains critical

Treasury markets continue to provide the clearest signal regarding gold's medium-term direction.

Yields remain elevated relative to historical standards, reflecting a Federal Reserve that has maintained a cautious stance toward easing expectations.

At the same time, recent economic data have reduced conviction around an extended period of aggressive monetary restraint.

Markets currently sit between two competing narratives.

One assumes that growth remains sufficiently resilient to support elevated yields for longer.

The other anticipates that labor conditions may soften enough to gradually alter the expected path of monetary policy.

Gold remains positioned between those outcomes.

The metal has shown resilience despite a supportive Dollar environment, suggesting investors continue allocating toward assets perceived as useful hedges against policy uncertainty.

Reserve diversification themes also remain present in the background.

Although short-term price action is largely determined by macroeconomic releases, institutional demand continues supporting gold's broader strategic role within global portfolios.

Participation therefore extends beyond speculative positioning.

It increasingly reflects a search for diversification within an environment characterized by elevated fiscal deficits, uncertain policy timing and shifting expectations regarding economic momentum.

Growth moderation does not imply economic weakness

One of the more important developments during recent weeks has been the distinction between moderation and contraction.

The ISM release illustrates that distinction.

Manufacturing activity remains in expansion territory.

Economic growth continues to show resilience.

Consumer conditions have softened at the margin without signaling a meaningful deterioration in activity.

For gold, this environment creates a relatively balanced backdrop.

A severe economic slowdown would introduce broader concerns regarding demand and financial stability.

Persistent economic strength would likely reinforce restrictive monetary expectations.

The current situation lies between those extremes.

Markets are attempting to determine whether slower hiring can coexist with stable economic activity.

Gold remains particularly sensitive to that scenario because it combines monetary exposure with a role as a macro confidence indicator.

This explains why labor-market releases have gained importance for precious metals investors.

Employment data increasingly determine whether recent shifts in expectations become durable or remain temporary adjustments within a broader higher-rate environment.

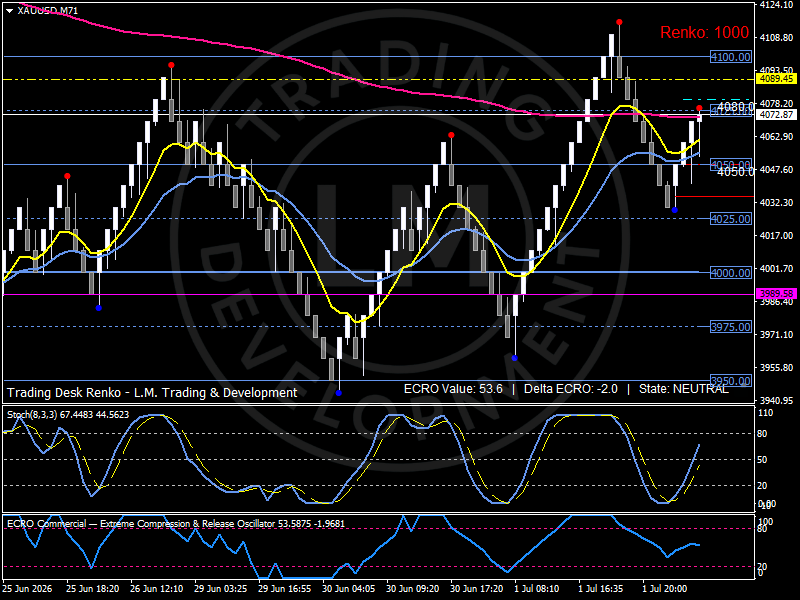

Technical structure: Gold stabilizes near the 4,075 participation pivot

The technical structure remains consistent with a market awaiting confirmation.

The Renko framework shows gold rotating inside a broadly neutral environment following recent volatility associated with economic data releases.

ECRO currently stands near 53.6, while Delta ECRO remains slightly negative at -2.0.

The market remains classified in a NEUTRAL state.

Participation conditions therefore remain balanced rather than directional.

The immediate participation pivot develops around 4,075, which has become the central equilibrium area during recent sessions.

Resistance remains concentrated near 4,100, followed by the broader participation corridor between 4,108 and 4,110.

Support develops around 4,050, while the deeper stabilization area extends toward 4,025.

Shorter-term EMA layers continue rotating above the broader structural trend, suggesting that downside pressure has moderated after the recent correction phase.

Momentum indicators have improved from previous lows, although conviction remains incomplete ahead of payroll confirmation.

The technical picture therefore reflects a market waiting for labor-market validation before committing toward a more persistent directional phase.

Bird's eye view

Gold currently operates inside a credibility-driven market where labor conditions, Treasury positioning and policy expectations remain tightly interconnected.

Payrolls represent the dominant catalyst because they offer insight into whether recent signs of labor moderation can influence the future trajectory of monetary policy.

Structurally, gold remains centered around the 4,075 participation pivot, with resistance concentrated near 4,100–4,110 and support developing around 4,050–4,025.

The key variables remain employment conditions, real yields, Dollar positioning and broader confidence in the durability of the current economic expansion.

Outlook

Gold enters payroll day within a balanced environment characterized by cautious positioning and moderate participation.

Markets have already absorbed softer manufacturing data and are now looking toward labor conditions as the next source of macro confirmation.

The upcoming employment report has the potential to influence expectations regarding yields, policy timing and Dollar behavior during the opening weeks of the third quarter.

The next directional phase will likely emerge from the interaction between labor-market dynamics, Treasury yields and evolving expectations regarding the credibility of the Federal Reserve policy path.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.