Global macro transmission monitor – Week ending June 12, 2026

Executive transmission map

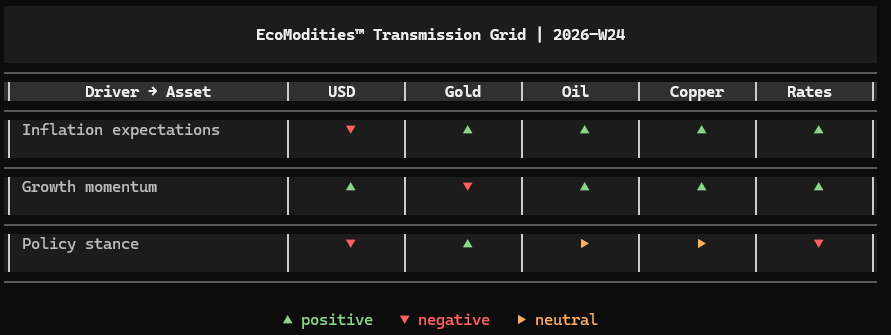

The macro transmission chain shifted toward softer US inflation pressure last week as Core CPI and Core PPI came in below expectations. Markets responded by reducing inflation-premium pricing, weakening support for the USD and improving conditions for gold and broader commodity markets.

Policy transmission became more regional after the European Central Bank raised its Main Refinancing Rate, narrowing part of the policy-differential gap against the USD without generating a broader hawkish repricing across global rates.

Growth signals remained uneven. UK GDP was in line with expectations but weaker than the previous month, reinforcing the view that disinflation is progressing while activity momentum remains fragile beneath the surface.

1. Macro shock layer

A. Inflation shock

What moved

US inflation data showed signs of moderation at the core level.

- Core CPI m/m: 0.2% vs 0.3% expected.

- Core CPI y/y: 2.9% vs 2.9% expected.

- CPI m/m: 0.5% vs 0.5% expected.

- CPI y/y: 4.2% vs 4.2% expected.

- Core PPI m/m: 0.4% vs 0.5% expected.

- PPI m/m: 1.1% vs 0.7% expected.

Why it matters

The softer core readings reinforced the view that underlying price pressures are easing, even as headline producer inflation remained firmer. Markets focused more on core disinflation than on the headline PPI surprise.

Transmission path

- USD lost inflation-driven support.

- Gold benefited from softer real-yield pressure.

- Oil and copper received support from improved financial conditions.

- Rates pricing moved toward a less aggressive path.

FX transmission

The USD weakened as inflation concerns eased. Commodity-linked and precious-metal-sensitive assets benefited from reduced real-yield pressure.

B. Growth shock

What moved

UK growth data weakened relative to the previous month while matching expectations.

- UK GDP m/m: -0.1% vs -0.1% expected.

- Previous: 0.3%.

Why it matters

The data did not surprise markets, but the decline from the previous month reinforced the view that growth momentum remains uneven despite improving inflation conditions.

Transmission path

- Oil remained supported despite softer European growth.

- Copper continued benefiting from broader macro optimism.

- Gold faced some pressure from resilient risk sentiment.

- Rates remained supported by slowing growth expectations.

FX Transmission

Growth-sensitive currencies traded selectively as investors differentiated between regional growth conditions rather than applying a broad risk-on or risk-off framework.

C. Policy Shock

What moved

The European Central Bank raised its Main Refinancing Rate.

- ECB Main Refinancing Rate: 2.40%.

- Previous: 2.15%.

The Bank of Canada left rates unchanged at 2.25%.

Why it matters

The ECB move introduced a regional tightening impulse, but the broader market response remained shaped by softer US inflation and contained global rates volatility. Policy transmission therefore weakened the USD through relative-differential channels rather than producing a broad hawkish repricing.

Transmission Path

- USD lost part of its policy advantage.

- Gold benefited from softer US rate pressure.

- Oil and copper remained broadly neutral to policy transmission.

- Rates volatility stayed contained.

FX transmission

EUR positioning improved as rate differentials narrowed against the USD, while broader FX markets continued focusing on inflation and growth differentials.

2. Cross-asset transmission grid – 2026-W24

3. Market alignment check

Cross-asset alignment improved during the week.

Softer US core inflation weakened support for the USD while improving conditions for gold, oil and industrial commodities. The ECB rate increase added a regional policy impulse, but did not override the broader disinflation narrative driving US rates and dollar positioning.

Growth remains the least aligned layer. UK GDP confirmed softer activity versus the previous month, while commodities continued to trade with support from financial conditions rather than clear demand acceleration.

The macro chain currently shows stronger inflation and policy transmission than growth confirmation.

4. Forward pressure points

USD

Pressure remains concentrated around further disinflation and narrowing policy differentials.

Gold

Gold remains highly sensitive to additional declines in inflation expectations and real yields.

Oil

Oil continues balancing supportive financial conditions against mixed growth signals.

Copper

Copper remains dependent on industrial demand resilience and manufacturing activity.

Rates

Rates markets remain vulnerable to additional disinflation signals and policy-differential repricing.

One-line takeaway

The macro transmission chain shifted toward softer US inflation last week, weakening USD support while improving conditions for gold and commodities, even as growth confirmation remained uneven.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.