Drop in UK unemployment isn’t all it seems

The UK unemployment rate, which dropped from 5.2% to 4.9%, appears to be driven by a spike in 'economic inactivity' as opposed to a rise in employment. And more importantly, it is likely to rise again as the energy crisis takes its toll on Britain's jobs market. That's why we don't currently expect the Bank of England to hike rates this year.

Is the UK jobs market at a turning point? It might be tempting to look at the relatively sharp drop in unemployment in the three months to February and conclude the answer is “yes."

The unemployment rate dropped from 5.2% to 4.9%. But crucially, this does not appear to be because of a big shift into work. Employment was little changed over the past quarter. Instead, the details reveal the drop in the jobless rate is pretty much solely down to a rise in “economic inactivity” – that is, people neither in work nor actively seeking it. And the Office for National Statistics notes that this was particularly visible for students. We’d be cautious about reading too much into this, but the bottom line is the drop in unemployment isn’t necessarily the “good news” story it first seems.

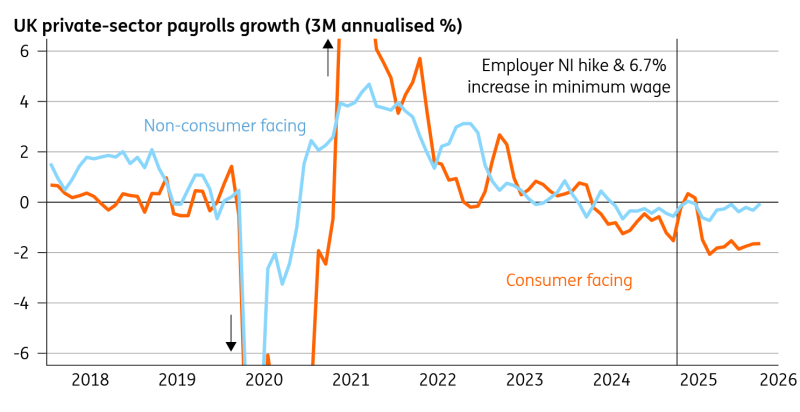

That’s further backed up by the more timely data on company payrolls (PAYE). Private sector employment continues to drop, driven primarily by consumer services. On a three-month annualised basis, employee numbers are falling by 1.6% in these sectors, which include hospitality and retail. And that pace of decline is showing no sign of abating.

Consumer-facing employment is showing consistent falls

At least some of that is attributable to last year’s employer National Insurance (payroll) tax and hike to the minimum wage, policy changes which have had a much more tangible impact on employment than inflation. That’s likely to be the playbook in the current energy crisis, too. Last year’s experience showed that corporate pricing power is diminished. And higher oil prices are likely to put renewed upward pressure on unemployment.

That is not a backdrop that is conducive to a renewed spike in wage growth. Private sector pay growth dipped to 3.2% in the most recent data, which, according to the Bank of England’s analysis in February, is consistent with a 2% inflation target. With headline inflation poised to rise towards 4% in Q3, it suggests real wages are set to fall and pressure on economic growth will mount.

Overall, today’s report is a reminder that the UK jobs market is going into the current energy crisis in a fragile state – and crucially, much weaker than it was in February 2022 at the onset of the last oil/natural gas shock. For the time being, we think the Bank will opt against rate hikes this year, keeping the Bank Rate at 3.75% instead.

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.