Dreadful UK jobs report questions need for rate hikes

The latest UK jobs report, which features rising unemployment, sharply lower payrolls and tumbling wage growth, is a reminder that the economy is much less susceptible to 'second round' effects from the incoming energy shock. We're still forecasting a rate hike in June, but that is far from guaranteed.

Ouch! Taken at face value, the latest UK jobs report is bad pretty much wherever you look.

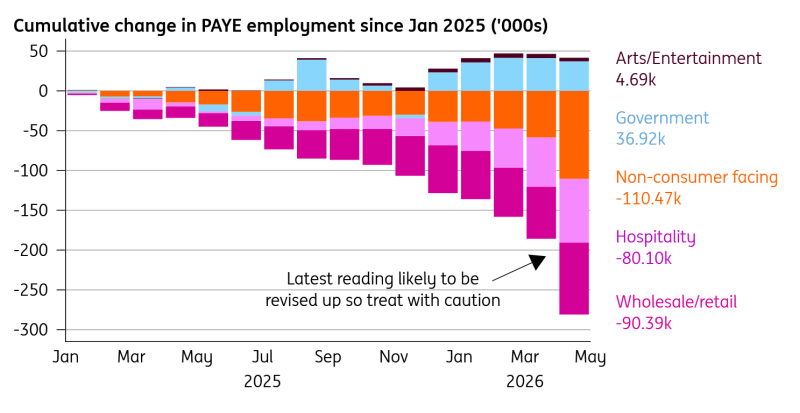

Admittedly, some of it looks more like noise than signal. Take the 100,000 drop in payrolled employment. That is a big number, but one that will almost certainly get revised up. We saw something similar last May, where an initially reported 109k drop was then revised up to a much more modest -14k decline. There are plenty of similar examples in recent history.

Still, backward revisions to both February and March are a reminder that the situation is fragile. Weakness has been particularly concentrated in consumer-facing sectors most affected by last year’s tax and minimum wage hikes. That pressure is only likely to be exacerbated by the incoming energy shock.

Payroll employment has been particularly weak in consumer services

Then there’s the unemployment rate, which picked up a tenth of a percentage point to 5.0%. Again, this has been bouncing around for the past couple of readings owing to volatility surrounding people recorded as unemployed and inactive. Given long-running issues with data quality and the Labour Force Survey, which is the source of the unemployment rate, we’re still inclined to take this with a heavy pinch of salt.

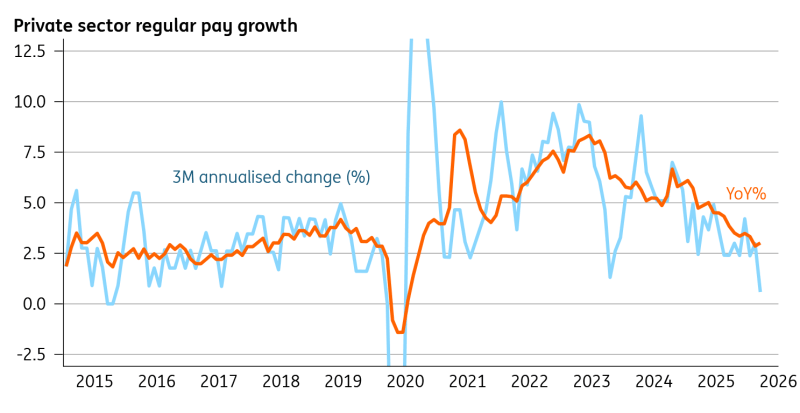

What really stands out here though is wage growth. Just look at the three-month annualised change in private pay – a mere 0.6%. By our reckoning, that’s the lowest figure since 2015. This does bounce around and almost certainly exaggerates the true picture. But at the very least, it says the near-term direction of private sector wage growth is lower. This is set to fall below 3% in the coming months.

Wage growth is slowing rapidly

All of this questions the need for Bank of England rate hikes. The economy looks much less susceptible to “second round” effects from higher energy prices on things like wage growth than it did four years ago in the last oil/gas shock.

Following the April BoE meeting, we’ve tentatively been forecasting a one-and-done rate hike in June. That remains our base case, mainly because our house view on energy prices, particularly for natural gas, and given that the Strait of Hormuz is showing little sign of reopening. But it’s a close call, and we remain open-minded about next month’s meeting. A lot will also depend on tomorrow’s inflation data.

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.