Czech expansion continues at a milder pace

Czech real GDP growth was confirmed at 2.2%, while private consumption and fixed investment dynamics were revised downwards. Solid incomes could still propel consumer spending, but labour market difficulties determine the direction here. ETS2 is planned for 2028, arguably presenting another blow to European industry.

Revised consumption and investment

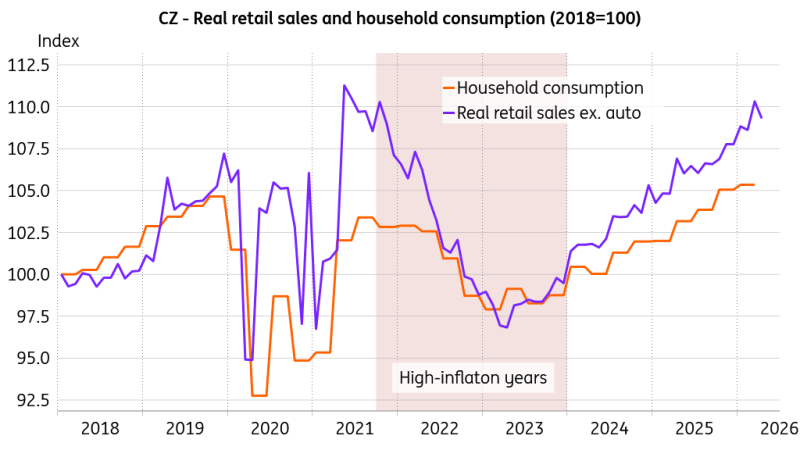

The Czech real GDP growth in the first quarter of 2026 was confirmed at 0.2% quarter-on-quarter and 2.2% yeyeaar-on-r. The new release shows a downward revision to the quarterly dynamics in household consumption to 0.3% and in fixed capital formation to 1.5%. In contrast, the quarterly dynamics of government consumption were revised upwards to 0.1%.

Muted household consumption gain in 1Q26

The investment rate of non-financial corporations increased by 0.5ppt from the previous quarter and 1.5ppt from the previous year, reaching 28.2% in 1Q26. Meanwhile, the profit rate dropped by 1.3ppt from the previous quarter and by 2.5ppt from the previous year, reaching 42.5% in 1Q26. Total wage costs of non-financial corporations added 8.7% YoY.

The average monthly income from employment added 1.0% QoQ in real terms and 5.6% YoY. The total real income of households per capita gained 0.3% QoQ in 1Q26 and increased by 3.2% YoY. The household savings rate in 1Q26 was 20%, which is 0.1ppt less than in the previous quarter and 0.3ppt more than a year ago.

Profitability is the key

The new investment cycle remained intact in 1Q26, though the annual dynamic eased. The appetite for investment is still there, as suggested by the rising investment rate. However, weaker profitability combined with increased uncertainty prompted by the Middle Eastern conflict may somewhat hamper fixed investment performance throughout the second and third quarters of this year. The ample income growth in both nominal and real terms can further foster consumer spending, but the dichotomy in the labour market that tends to favour experienced workers and leave low-income earners behind may inhibit any further acceleration.

And yes, it is profitability that enables both ample investment and punchy wage increases. Nevertheless, the profitability of European companies may come under even more serious pressure from foreign competition.

In particular, dumping export prices of Chinese producers – often enabled by state subsidies and other debated practices – present an existential risk. Combined with higher energy costs than almost anywhere else in the world, European industry is fighting an uphill battle – one it isn't guaranteed to survive.

ETS2 to hit in 2028

The EU ETS2 emissions pricing system has been approved by the European Parliament and is scheduled to start on 1 January 2028. This is a burden not only for households but also for small and medium-sized companies. The consequence is that resources for any homegrown research and innovation will be even smaller, which will only shift Europe closer to a subsidies-driven planned economy and further from market-based competition. And in the Czech Republic, memories still linger of poor supply under a state-run economy.

Perhaps a useful analogy here is Europe’s space research. You can proceed with training in Cologne’s European Astronaut Centre, but one problem remains: Europe doesn't have a decent space rocket. And with the ongoing regulatory push, Europe may risk reaching a dead end in the AI domain as well. Indeed, you may become the spearhead in AI regulation, but do you really have major players to regulate? Perhaps not; the regulatory burden could discourage their emergence. The story is similar for industry and energy: you squeeze the producers so much that, in the end, you may eventually end up with too little left to sustain.

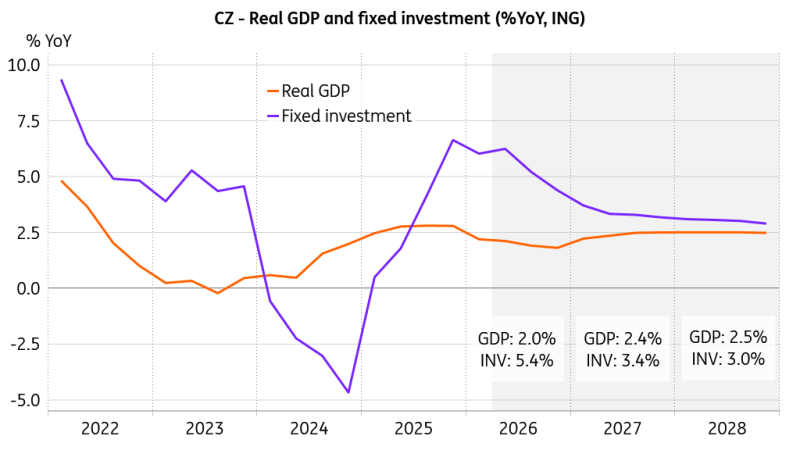

Solid investment fosters growth potential

In any case, we expect the Czech economy to continue to outperform that of the wider eurozone over the coming years, mostly on the back of two underlying driving forces: a) a sense of pragmatism and b) a sense of self-preservation. It could be argued that the recent shift observed, for example, in Germany towards closer cooperation with China (including asset sell-offs) rather than competing reflects neither. Instead, it appears more akin to a form of economic pessimism, partly driven by Europe’s challenging business environment, characterised by extensive regulation, high energy costs, and persistent uncertainty.

It remains to be seen how Czech firms will cope with these conditions over the longer term. Incorporating the revised GDP breakdown and lower Brent crude prices, we maintain our forecast of 2% growth this year and 2.4% next year.

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.