China’s reflation trend continues to solidify

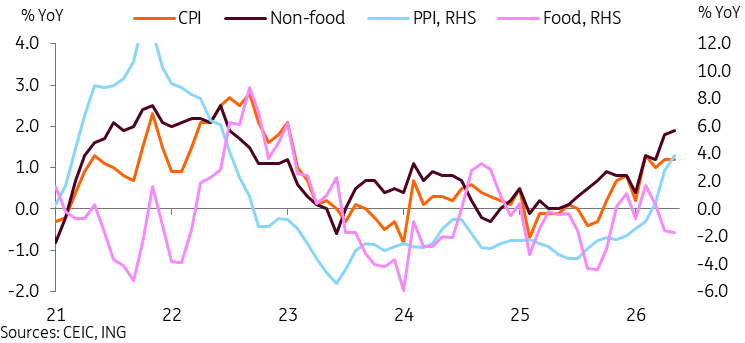

China’s May inflation data was broadly in line with forecasts, with CPI steady at 1.2% year-on-year and PPI rising to 3.9%. Food and property prices are helping suppress headline inflation for now. But rising prices more broadly suggest we're moving from deflation into a low inflation environment.

CPI inflation steady in May as higher energy is offset by slumping food and rental prices

China's CPI inflation remained unchanged at 1.2% year-on-year in May, marginally softer than our forecast and market expectations for a slight uptick to 1.3%. Inflation has been at or over 1% for the past 4 months, and in positive territory for 8 straight months, suggesting the reflation trend is solidifying.

Consumer prices were supported by a major surge in the transportation fuels subcategory, which rose 21.1% YoY in May, reflecting higher oil prices. While local gasoline prices generally didn’t rise as much as Brent crude oil, we saw moves of around 24% above pre-Iran War levels. If crude oil prices remain elevated for longer, pump prices could rise further.

Most inflation subcategories were fairly stable in May. Clothing (1.4%), healthcare (2.1%), and Education, Culture, and Entertainment (1.3%) were all within 0.1pp of April's data.

Two main categories continue to hold back inflation:

First, food inflation fell further to -1.7% YoY in May, as pork (-16.1%), fresh fruit (-2.2%), dairy (-1.2%), and edible oil (-1.2%) remained in deflationary territory. China's pork cycle has taken longer than normal to turn. This has been attributed to rising production efficiency, while purchase agreements to import soybeans could also be contributing to low feed prices.

Second, housing inflation remained negative for a sixth consecutive month. Rental prices fell -0.6% YoY, as the property market has yet to confirm a bottom. We've seen some positive signals in the recent monthly property price data. They include stabilisation in tier-1 cities and an overall slower pace of price declines. This drag, though, is likely to continue in the near term.

These factors will likely keep China's CPI inflation at positive but low levels moving forward.

Falling food and rental prices are balancing out higher inflation elsewhere

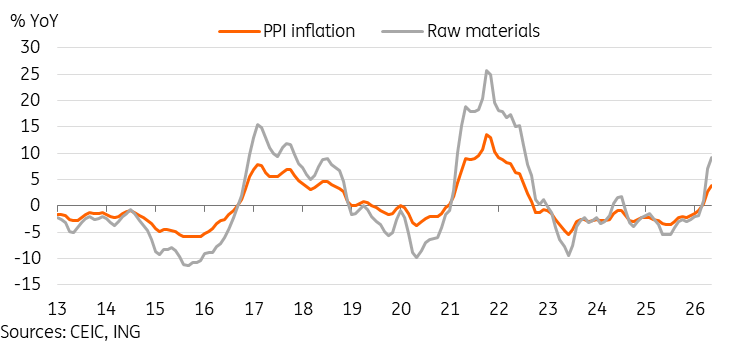

Higher energy having clearer upward impact on PPI inflation

PPI inflation rose to 3.9% YoY, up from 2.8% in April and in line with expectations. However, in month-on-month terms, producer prices actually cooled from 1.7% to 0.5%, a 3-month low.

Looking at ex-factory prices, we see the biggest increases in non-ferrous metals mining (36.5%) and oil and gas extraction (35.7%) industries. The petroleum and coal processing industries also saw prices rise by 18.4% YoY in May. The trend in the non-ferrous metals industry was already underway before the Iran war. But upticks in the oil and gas extraction and fuel processing industries clearly reflect the impact of higher energy prices. The Iran war has accelerated what was previously set to be a more moderate return to positive PPI inflation.

Raw material prices further accelerated to 9.2% YoY, and look set to move into the double-digits in the coming months. This is likely to feed through to other prices in the coming months. Many producers operating on thin margins will have no choice but to pass on the cost to consumers.

Rising raw material costs are likely to feed through to other prices moving forward

Will China see second-round inflation effects?

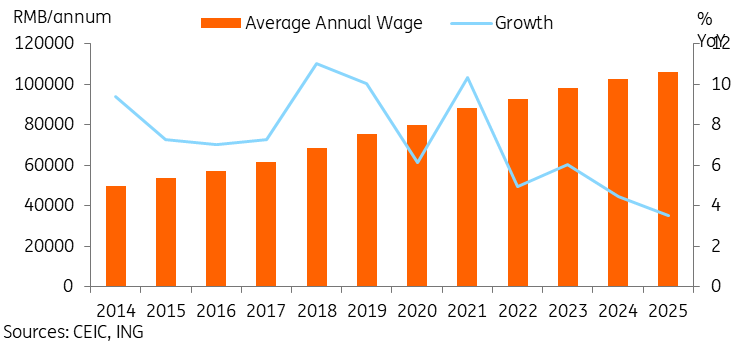

In the past few months, you may have seen some of my colleagues write about so-called second-round effects on inflation. This is where the impact of higher wages in response to initial price upticks leads to workers demanding higher wages, companies raising prices to stay profitable, and a wage-price spiral.

Is this going to happen in China? If so, it could actually be welcome news for many workers, after deflationary expectations and general cost-cutting pressures amid involution-type competition led to years of slowing wage growth and even pay cuts.

We're not expecting major momentum on this front this year. This is especially the case as we still see elevated youth unemployment numbers, and many workers are more concerned about keeping their jobs amid AI advancements. Anecdotal observations suggest that many workers' bargaining power and mobility still seem generally weaker than in the pre-COVID era.

With that said, if it does play out, it marks an upside risk for our inflation forecast of 1.3% YoY. For now, though, this sort of low but positive inflation isn't likely to impede potential monetary policy easing. This is still on the table this year, especially if we see economic data continue to soften.

Could recent reflation turn around the falling wage growth story?

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.