A hawkish hold in Australia, a cautious hike in Japan, and a defining moment for the Fed

In Australia, policymakers left interest rates unchanged but maintained a clear tightening bias, warning that higher energy costs could keep inflation elevated and potentially require additional rate increases. In Japan, the Bank of Japan (BoJ) delivered another rate hike, taking borrowing costs to their highest level in more than three decades, yet policymakers appeared cautious about committing to a sustained tightening cycle.

Attention now shifts to the Federal Reserve. Although the Fed is widely expected to leave rates unchanged, investors are focused less on the decision itself and more on what new Chair Kevin Warsh reveals about the future direction of US monetary policy. At a time when markets are searching for clues on global interest-rate trends, the Fed’s communication may prove more important than the policy decision.

Australia: A hold that still sounds Hawkish

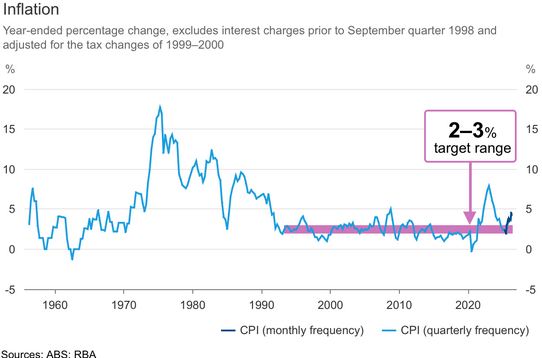

The Reserve Bank of Australia (RBA) left its cash rate unchanged at 4.35%, adopting a wait-and-see approach as policymakers assess the impact of previous rate increases on the economy.

The decision was unanimous, reflecting the central bank’s preference to gather more evidence before making another move. However, investors should not mistake the pause for a shift toward easing. The RBA maintained a distinctly hawkish tone and made clear that additional tightening remains possible if inflation proves more persistent than expected.

The main concern remains energy prices. Rising oil costs have raised the risk that consumer prices remain above the RBA’s 2% to 3% target range for longer than anticipated. Although headline inflation has moderated, underlying price pressures remain elevated, suggesting the battle against inflation is not yet won.

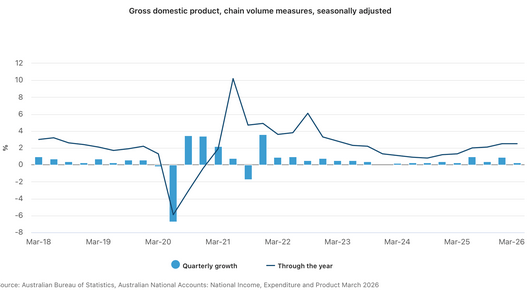

At the same time, economic growth is slowing. Australia’s economy expanded by just 0.3% during the first quarter, down sharply from 0.9% in the previous quarter. Household spending has weakened as higher borrowing costs continue to weigh on consumers, while the labour market has also shown signs of cooling.

For now, the central bank appears determined to keep its tightening option alive. The message from Sydney is clear: rates may not have moved this month, but the possibility of another hike remains firmly on the table.

Japan: A historic hike accompanied by caution

The BoJ raised its policy rate from 0.75% to 1%, bringing borrowing costs to their highest level since 1995 and marking another major milestone in Japan’s long journey away from ultra-loose monetary policy.

The decision reflected growing concern that inflation could accelerate further as higher energy prices feed through the economy. Policymakers warned that underlying inflation risks remain tilted to the upside and reiterated their willingness to respond if price pressures intensify.

Daily Brent Crude Oil Chart - Source: TradingView with ActivTrades Data

Several factors suggest that further tightening may not come quickly. The Japanese economy remains vulnerable to external shocks, particularly given uncertainty surrounding global trade and energy markets. Some policymakers have also expressed concern that higher borrowing costs could undermine growth and employment.

Political considerations add another layer of complexity. Prime Minister Sanae Takaichi has generally favoured accommodative policies designed to encourage investment and support economic expansion. While the BoJ remains operationally independent, political preferences can influence expectations regarding the pace of future tightening.

The Japanese yen also remains a major concern. Despite previous intervention efforts, the currency continues to trade at relatively weak levels against the US Dollar. A weaker yen increases import costs and contributes to inflation, but it also complicates the policy outlook by creating uncertainty about the effectiveness of future rate increases.

Daily USD/JPY Chart - Source: TradingView with ActivTrades Data

As a result, the BoJ’s latest decision can be described as a hawkish action accompanied by a relatively dovish outlook. Policymakers have acknowledged inflation risks, but they have stopped short of signalling a clear sequence of additional hikes.

This stands in contrast with Australia, where the central bank did not raise rates but maintained a stronger tightening bias for future meetings. The spotlight now turns to the Federal Reserve.

The Federal Reserve faces a communication test

Markets overwhelmingly expect policymakers to leave the federal funds rate unchanged in a range between 3.5% and 3.75%, meaning the policy decision itself is unlikely to generate significant surprises. Instead, attention will focus on the Fed’s guidance and, more specifically, on the first major appearance of new Chair Kevin Warsh.

Every new Federal Reserve chair faces a credibility test, and this meeting provides Warsh with his first opportunity to shape market expectations. Investors are eager to understand how he views inflation risks, economic growth and the future direction of monetary policy.

The challenge is particularly significant because the global monetary landscape has become increasingly fragmented. Australia remains concerned about inflation persistence. Japan has begun normalising policy but appears cautious about tightening too aggressively. Meanwhile, the US economy continues to navigate the balance between moderating inflation and maintaining growth.

Against this backdrop, traders will scrutinise every element of Warsh’s communication. One key question is whether he adopts a more hawkish or dovish tone than markets currently expect. Another is whether he signals broader changes to the way the Federal Reserve communicates policy decisions.

Warsh has previously expressed scepticism about some of the Fed’s communication tools, particularly the widely followed "dot plot" that shows policymakers’ rate expectations. Any indication that the Fed could eventually alter its forecasting framework would attract significant market attention.

For investors, the post-meeting press conference is the real main event, overshadowing the actual rate decision. What matters most right now isn’t the current rate, but how the new chair intends to steer policy over the coming months.

Stay up to date with what's moving and shaking on the world's markets and never miss another important headline again! Check ActivTrades daily news and analyses here.

Author

Carolane de Palmas

ActivTrades

Carolane graduated with a Masters in Corporate Finance & Financial Markets and got the AMF Certification (Financial Markets Regulator in France). Afterward, she became an independent trader, investing mostly in European and American stocks/indices.