GBP/JPY rises as Oil-driven Yen weakness and BoE-BoJ rate gap sustain bullish bias

- GBP/JPY rises as the Yen remains under pressure from elevated Oil prices amid Middle East tensions.

- Wide interest rate differential between the BoE and BoJ keeps the British Pound supported.

- Technically, GBP/JPY holds above key SMAs, but momentum remains mixed with RSI near neutral and MACD in negative territory.

GBP/JPY edges higher on Tuesday as the Japanese Yen (JPY) tumbles across the board, with the impact of Tokyo’s intervention fading and attention shifting back to ongoing tensions in the Middle East. At the time of writing, the cross is trading around 213.90, up nearly 0.53% on the day.

The Japanese Yen remains under pressure as rising Oil prices increase concerns about Japan’s import costs. While both the UK and Japan rely on energy imports, Japan is more vulnerable due to its heavier dependence on supplies passing through the Strait of Hormuz, where tensions remain high.

Meanwhile, the cross continues to draw support from the wide interest rate differential between the Bank of England (BoE) and the Bank of Japan (BoJ). Oil-driven inflation risks are reinforcing this divergence, as expectations grow that central banks may need to tighten policy to contain price pressure.

While the BoJ remains on a gradual tightening path, concerns over economic growth from the energy shock could cloud its policy outlook, whereas the BoE is seen as more likely to act, with traders pricing in at least two rate hikes by year-end, keeping the yield gap tilted in favor of the British Pound (GBP).

Technical Analysis:

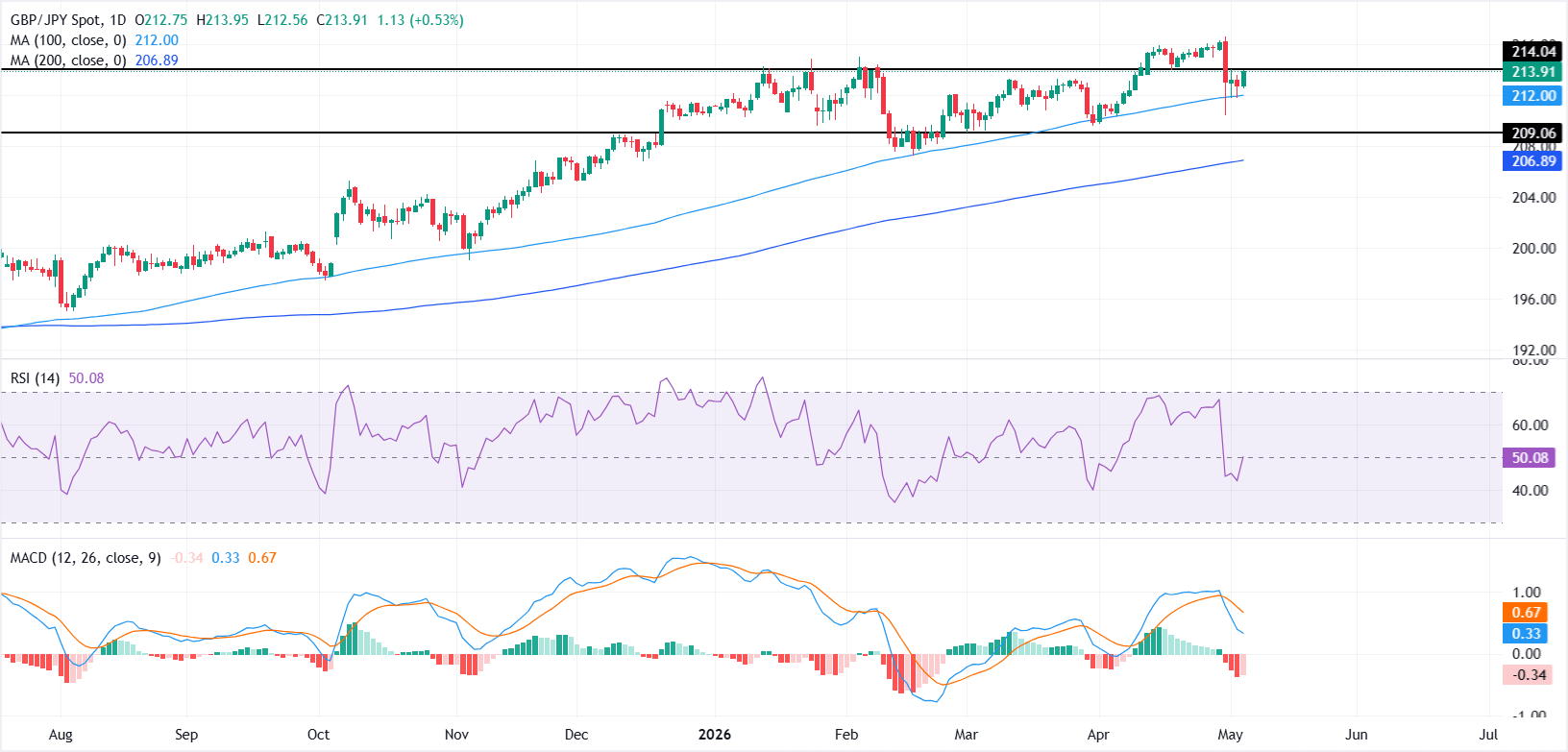

In the daily chart, GBP/JPY holds a constructive bias as it remains above both the 100-day Simple Moving Average (SMA) and the 200-day SMA. The placement of price over these medium- and long-term averages suggests the broader uptrend is still intact, although the Relative Strength Index around 50 hints at neutral momentum and a lack of immediate directional conviction, while the negative Moving Average Convergence Divergence (MACD) reading warns that upside progress could be uneven in the near term.

On the topside, initial resistance aligns with the nearby horizontal barrier at 214, where a clear break and daily close higher would open the way for a renewed advance within the prevailing bullish structure. On the downside, the 100-day SMA at 212 offers the first layer of support ahead of the horizontal floor at 209, with the 200-day SMA down at 206 reinforcing the broader bullish backdrop as a deeper but still trend-consistent demand zone.

(The technical analysis of this story was written with the help of an AI tool.)

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Author

Vishal Chaturvedi

FXStreet

I am a macro-focused research analyst with over four years of experience covering forex and commodities market. I enjoy breaking down complex economic trends and turning them into clear, actionable insights that help traders stay ahead of the curve.