British Pound bags a soft PCE and forgets about it

- Core PCE missed the consensus to the downside, with Q1 GDP revised lower for good measure.

- Sterling rallied into the print, then stalled, suggesting the dovish read was already in the price.

- Next week brings four Bailey speeches, BoE Monetary Policy Report Hearings, and NFP on Friday.

The Personal Consumption Expenditures Price Index (PCE) print Sterling traders had been waiting for landed in the bears' lap, and the Pound did almost nothing with it. Core PCE rose 0.2% on the month against a 0.3% consensus, the softest monthly read in three. The headline equivalent printed 0.4% versus 0.5% expected. The Gross Domestic Product (GDP) revision for Q1 came in at 1.6% annualised, down from the 2% advance estimate. Three dovish data points in one window, and the Pound is sitting near 1.3440, more or less unchanged from where it traded into the 12:30 GMT release. The interesting story is not the data. It is the lack of follow-through.

A rally that arrived early

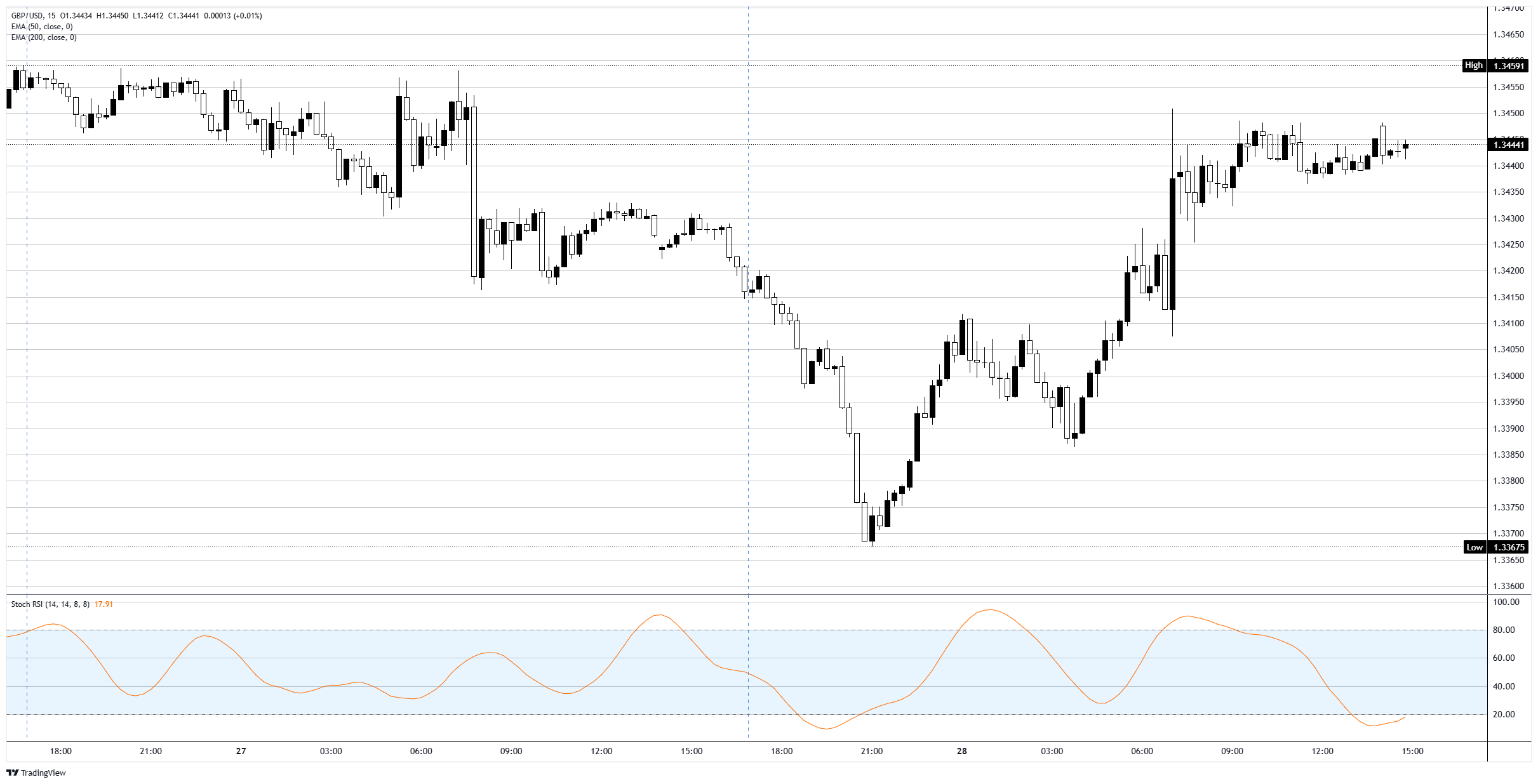

The pre-PCE positioning told the story. Sterling bottomed close to 1.3350 late Wednesday and ground higher through the European morning, printing 1.3450 a full five hours before the data. By the time the Bureau of Economic Analysis pushed the release, the dovish surprise was already priced into the tape, and the GDP revision lower did nothing to extend the move. This is what a positioning-driven rally looks like when it runs ahead of the catalyst. The actual print becomes the take-profit signal rather than the trigger, and the pair settles into a range. Anyone hoping the soft PCE would carry Sterling cleanly through the 50-period Exponential Moving Average (EMA) above 1.3500 will need a different excuse next week.

The Bailey roadshow nobody is calendar-circling

Governor Bailey speaks four times next week. Friday morning, then Tuesday, then Thursday, then Friday again. Sandwiched in the middle, the Bank of England (BoE) Monetary Policy Report (MPR) Hearings on Wednesday. That is an unusual cadence, and it is the kind of communication blitz central bankers run when they want to massage market expectations ahead of a meeting that is still six weeks out. The April Monetary Policy Committee (MPC) split 8-1, with the dissent voting to hike. The committee currently leans hawkish in a way the Federal Open Market Committee (FOMC) does not, where the dissents are skewed three-to-one in the opposite direction. The implication, which the consensus has yet to fully digest, is that the structural rate differential between the BoE and the Federal Reserve (Fed) is no longer working against the Pound. If Bailey leans into the hawkish dissent at any point in his quartet, the asymmetric move is up, not down.

NFP Friday is the regime test

The other reason this week's PCE softness landed quietly is that the market has already moved on. Nonfarm Payrolls (NFP) on Friday, June 5 is the more important number, and it arrives at the end of a calendar week stacked with Institute for Supply Management (ISM) Manufacturing and Services Purchasing Managers Indexes (PMIs) on Monday and Wednesday. Powell speaks Sunday night. If the labour market shows the kind of softening that the recent jobless claims trend hints at, the Fed's hawkish bloc loses cover and the December rate path reprices fast. Until then, PCE is filed under "noted."

Trade setup

The daily 200 EMA near 1.3400 has held as the practical floor for three sessions. The 50 EMA near 1.3460 is the immediate ceiling, with 1.3500 the breakout pivot. A reclaim of 1.3500 puts 1.3550 in play and forces a rethink of the sideways drift. Below 1.3400, 1.3350 is the line, and a break exposes 1.3300. The daily Stochastic Relative Strength Index (Stoch RSI) sits close to 30, broadly neutral. The actionable bias into Bailey Friday is range-fade with an asymmetric eye on hawkish surprise.

GBP/USD 15-minute chart

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.