Australia’s CPI inflation declines to 4.2% YoY in April vs. 4.4% expected

Australia’s Consumer Price Index (CPI) rose by 4.2% year-over-year (YoY) in April, compared to a 4.6% increase reported in the previous reading, the latest data published by the Australian Bureau of Statistics (ABS) showed on Wednesday.

The market consensus was for 4.4% growth in the reported period.

The RBA Trimmed Mean CPI for April rose 0.3% and 3.4% on a monthly and and annual basis, respectively. The monthly Consumer Price Index came in at 0.4% in April, compared to the previous reading of 1.1%.

AUD/USD reaction to Australia's Consumer Price Index data

The Australian Dollar (AUD) attracts some sellers following the Australia's CPI report. The AUD/USD pair is losing 0.12% on the day to trade at 0.7159, at the press time.

Australian Dollar Price Today

The table below shows the percentage change of Australian Dollar (AUD) against listed major currencies today. Australian Dollar was the weakest against the New Zealand Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.04% | -0.03% | -0.02% | 0.00% | 0.12% | -0.13% | -0.05% | |

| EUR | 0.04% | 0.00% | 0.02% | 0.04% | 0.16% | -0.09% | -0.01% | |

| GBP | 0.03% | -0.01% | 0.00% | 0.04% | 0.13% | -0.08% | -0.01% | |

| JPY | 0.02% | -0.02% | 0.00% | 0.03% | 0.13% | -0.10% | -0.01% | |

| CAD | -0.01% | -0.04% | -0.04% | -0.03% | 0.10% | -0.11% | -0.04% | |

| AUD | -0.12% | -0.16% | -0.13% | -0.13% | -0.10% | -0.21% | -0.12% | |

| NZD | 0.13% | 0.09% | 0.08% | 0.10% | 0.11% | 0.21% | 0.07% | |

| CHF | 0.05% | 0.01% | 0.01% | 0.01% | 0.04% | 0.12% | -0.07% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Australian Dollar from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent AUD (base)/USD (quote).

This section below was published at 19:00 GMT on Tuesday as a preview of the Australia’s CPI inflation report.

- Australia’s Consumer Price Index is expected to have eased in April, but to remain near long-term highs.

- Monthly CPI inflation is expected to have eased amid the Australian government’s fuel excise relief.

- April’s CPI figures are likely to keep pressure on the RBA to tighten monetary policy further.

The highlight in the Australian economic docket this week is the April Consumer Price Index (CPI) figures, which are expected to be released by the Australian Bureau of Statistics (ABS) on Wednesday at 01:30 GMT. Consumer inflation is forecast to slow down to a 4.4% year-on-year (YoY) rate, down from 4.6% in March, yet still at its highest levels since 2023, and well above the Reserve Bank of Australia’s (RBA) 2% to 3% target for price stability.

The Australian government’s decision to halve fuel excise in April might have contributed to taming monthly inflation to 0.6% in April from the previous month’s 1.1% reading. The Trimmed Mean CPI, however, considered more relevant to assess underlying inflationary trends, is expected to have accelerated to 3.4% in the 12 months to April from 3.3% in March and 0.4% monthly from the previous 0.3% rate.

On the whole, these numbers might provide a momentary respite to the RBA, but they do not ease pressure on the central bank to keep tightening borrowing costs. Investors are pricing a pause at the next monetary policy meeting due in mid-June, as the consequences of Iran’s conflict seem to be starting to take a toll on the Australian economy.

What to expect from Australia’s inflation rate numbers?

April’s CPI figures are expected to confirm that the higher energy prices stemming from the Middle East conflict keep boosting consumer prices, although recent reports warn about pass-through effects, with inflationary effects visible on a range of products from food to recreation or building materials.

In this context, the central bank would celebrate some moderation on the CPI growth, especially after the labour data released last week showed that the Unemployment Rate unexpectedly rose to 4.5% in April, its highest level since September..

The RBA, nevertheless, remains focused on inflation as the main target of its monetary policy. The minutes of May’s meeting showed nearly unanimous support for the third consecutive interest rate hike and reflected a hawkishly-leaning stance as the board projects price pressures to remain above target for an extended period.

Analysts from Westpac support that view, as they see Australian inflation peaking at 5% this year, and return to the RBA’s target only in late 2027: “Brent oil is now expected to average $125 per barrel in Q2. Headline inflation is now expected to peak lower at 5.0%yr in Q3 2026, but prove more persistent, ending the year at 4.9%yr and reaching 2.5%yr by end-2027.”

Interest rates, however, are likely to remain steady at June’s meeting, with an August hike on the table. May’s minutes also revealed that most RBA board members consider the current 4.35% Cash Rate target as somewhat restrictive, and that there is now some margin to observe how households and businesses react to the current conditions and to developments in the Middle East. Any sign of inflation moderation, even a mild one, in this case, will support that stance.

How could the Consumer Price Index report affect AUD/USD?

With inflation figures well above target, and the US-Iran conflict in a stalemate, any deviation in the Consumer Price Index data might have a significant impact on the Australian Dollar’s volatility. April’s will be the last CPI release before the RBA’s June monetary policy meeting, and, although it is unlikely to alter expectations of a rate pause, it will provide further insight into the banks’ next steps.

If final numbers meet market consensus, the impact on the Aussie is expected to be minor, with all eyes on the US-Iran peace process. A lower-than-expected inflation will practically confirm steady interest rates in June, and might cast doubt on an August rate hike, which is highly likely to add bearish pressure on the Australian Dollar (AUD).

The risk, however, is of a strong CPI reading, especially if the yearly inflation accelerates unexpectedly. This would signal stronger-than-expected second-round inflationary effects and increase pressure on the RBA to keep tightening its monetary policy. This option would have a positive impact on the AUD.

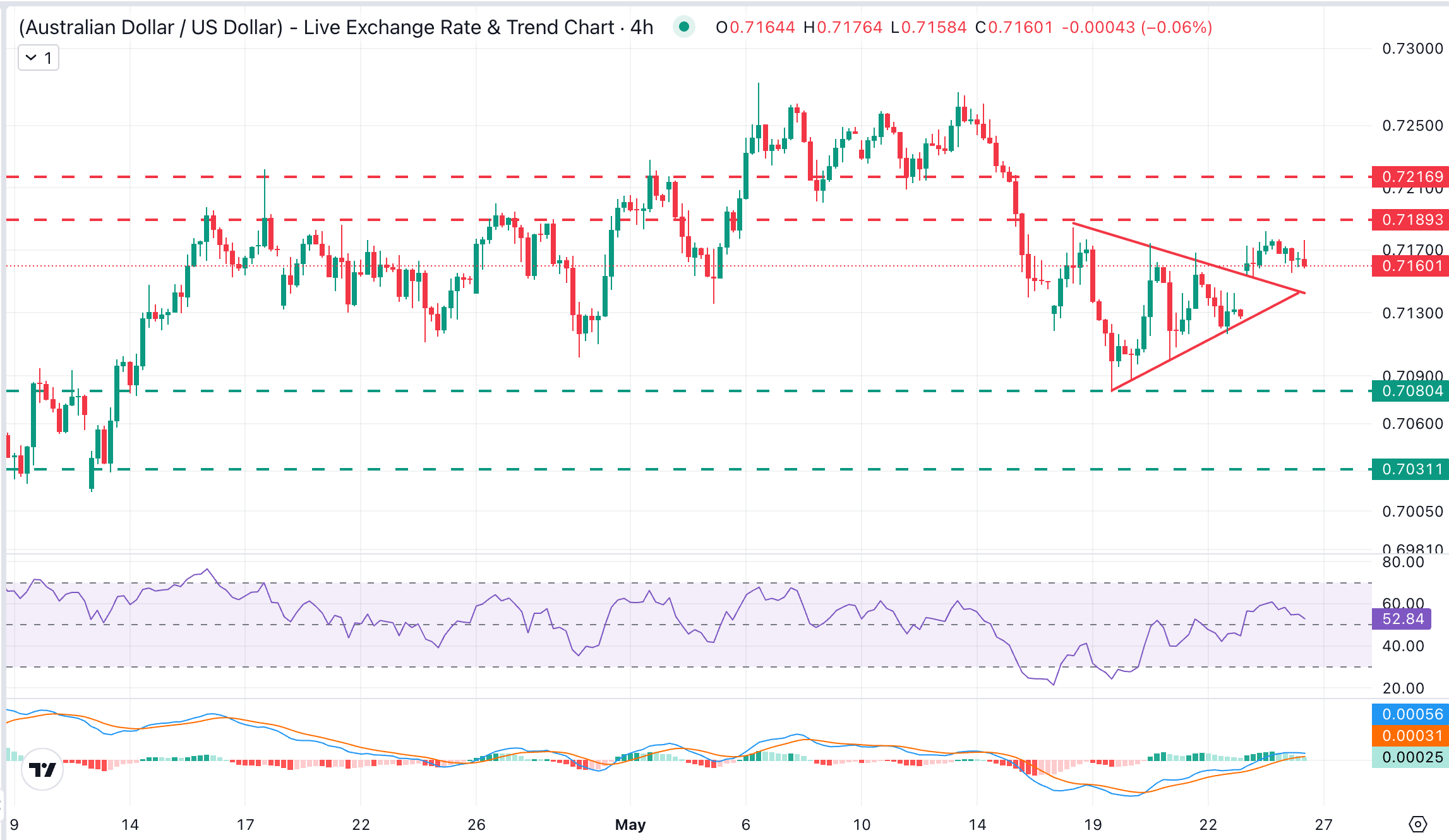

From a technical perspective, the AUD/USD is showing a somewhat stronger stance this week, according to FXStreet Analyst, Guillermo Alcala, although resistance around 0.7190 remains a significant hurdle for bulls: “The pair has broken above the triangle pattern observed last week, but bulls seem to be losing momentum after failing to breach resistance at the 0.7190 area.”

On the downside, Alcala sees key support at 0.7080: “Downside attempts are likely to find support at a reverse trendline, now in the area of 0.7145. Further down, a break of May’s 19 low at 0.7080 would signal the negation of the bullish view and expose the April 13 low, near 0.7030.”

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Author

FXStreet Team

FXStreet

Composed of a group of economic journalists and FX experts, the FXStreet content team produces and oversees all content published on FXStreet. It provides a purely journalistic approach to the Forex market.