AUD/USD Price Forecast: Sellers eye 0.7100 support as momentum indicators weaken

- AUD/USD trades on the back foot as softer Australian CPI data pressures the Aussie Dollar and dampens RBA hike expectations.

- The US Dollar steadies as traders digest conflicting headlines surrounding a potential US-Iran agreement.

- Technically, AUD/USD remains capped below the 20-day Bollinger SMA as momentum indicators suggest a neutral-to-bearish near-term bias.

AUD/USD attracts sellers on Wednesday as softer-than-expected Australian inflation data weighs on the Australian Dollar (AUD), while persistent uncertainty surrounding a potential US-Iran peace deal keeps the US Dollar (USD) supported. At the time of writing, the pair is trading around 0.7136, down nearly 0.44% on the day.

Data released earlier on the day showed Australia’s Consumer Price Index (CPI) eased to 4.2% YoY in April from 4.6% in March, missing market expectations of 4.4%. Meanwhile, the Reserve Bank of Australia’s (RBA) closely watched Trimmed Mean CPI accelerated to 3.4% YoY from 3.3%, matching market forecasts.

The softer headline inflation reading, along with recent soft labor market data, prompted traders to scale back bets on near-term RBA rate hikes and reinforced expectations of a prolonged pause in the central bank’s tightening cycle.

On the geopolitical front, mixed signals surrounding ongoing US-Iran negotiations continue to keep broader market sentiment cautious, limiting downside pressure on the US Dollar.

Earlier in the day, Iran’s State TV reported that Tehran and Washington had prepared an initial unofficial framework for a memorandum of understanding (MOU). However, the United States later denied the reports, calling the alleged interim peace deal draft “a complete fabrication.”

The US Dollar Index (DXY), which tracks the Greenback’s value against a basket of six major currencies, is trading around the 99.20 mark after briefly slipping below 99.00 earlier in the European session.

Technical Analysis:

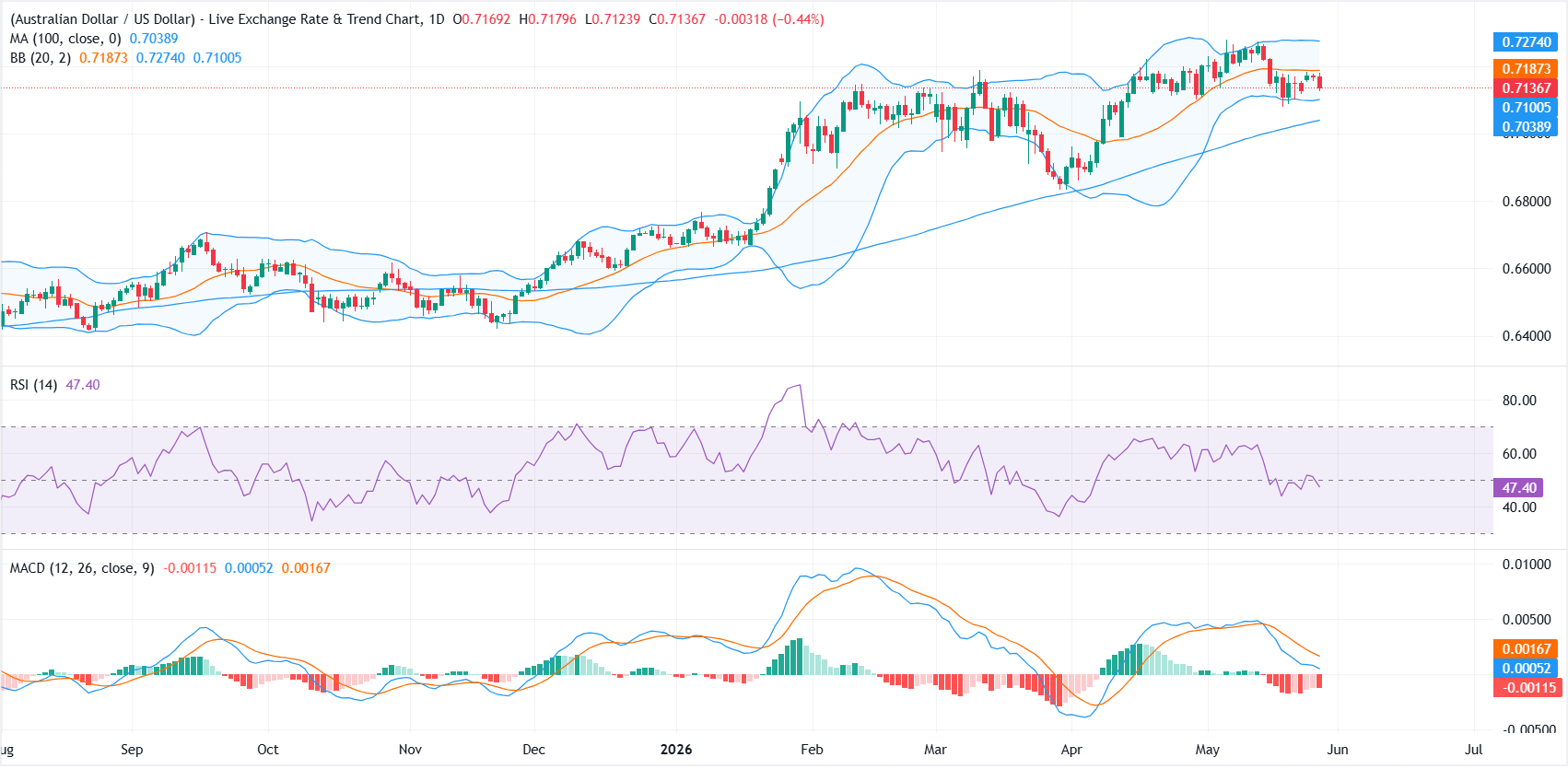

On the daily chart, AUD/USD holds under the 20‑day Bollinger Simple Moving Average (SMA) at 0.7187, leaving near‑term price action capped inside the upper half of the recent volatility envelope, while still holding above the 100‑day moving average (MA) at 0.7038.

This configuration, combined with a Relative Strength Index (RSI) easing toward the mid‑40s and a slightly negative Moving Average Convergence Divergence (MACD) reading, suggests fading upside momentum and a neutral to mildly bearish bias as buyers lose traction below short‑term dynamic resistance.

On the topside, initial resistance is located at the 20‑day Bollinger SMA around 0.7187, with a break higher exposing the upper Bollinger band near 0.7274 as the next hurdle.

On the downside, the lower Bollinger band around 0.7100 offers immediate support; a sustained move beneath this area would likely draw AUD/USD back toward the 100‑day MA near 0.7038, where broader trend support is expected to attract dip‑buyers on a first test.

(The technical analysis of this story was written with the help of an AI tool.)

RBA FAQs

The Reserve Bank of Australia (RBA) sets interest rates and manages monetary policy for Australia. Decisions are made by a board of governors at 11 meetings a year and ad hoc emergency meetings as required. The RBA’s primary mandate is to maintain price stability, which means an inflation rate of 2-3%, but also “..to contribute to the stability of the currency, full employment, and the economic prosperity and welfare of the Australian people.” Its main tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will strengthen the Australian Dollar (AUD) and vice versa. Other RBA tools include quantitative easing and tightening.

While inflation had always traditionally been thought of as a negative factor for currencies since it lowers the value of money in general, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Moderately higher inflation now tends to lead central banks to put up their interest rates, which in turn has the effect of attracting more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in the case of Australia is the Aussie Dollar.

Macroeconomic data gauges the health of an economy and can have an impact on the value of its currency. Investors prefer to invest their capital in economies that are safe and growing rather than precarious and shrinking. Greater capital inflows increase the aggregate demand and value of the domestic currency. Classic indicators, such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can influence AUD. A strong economy may encourage the Reserve Bank of Australia to put up interest rates, also supporting AUD.

Quantitative Easing (QE) is a tool used in extreme situations when lowering interest rates is not enough to restore the flow of credit in the economy. QE is the process by which the Reserve Bank of Australia (RBA) prints Australian Dollars (AUD) for the purpose of buying assets – usually government or corporate bonds – from financial institutions, thereby providing them with much-needed liquidity. QE usually results in a weaker AUD.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the Reserve Bank of Australia (RBA) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the RBA stops buying more assets, and stops reinvesting the principal maturing on the bonds it already holds. It would be positive (or bullish) for the Australian Dollar.

Author

Vishal Chaturvedi

FXStreet

I am a macro-focused research analyst with over four years of experience covering forex and commodities market. I enjoy breaking down complex economic trends and turning them into clear, actionable insights that help traders stay ahead of the curve.