Yentervention: Will it stick this time?

Japan’s first intervention in the Forex market in almost two years shows that authorities are serious about preventing the sharp depreciation of the Yen. While the move may work in the short term, any significant reversal of the trend is unlikely because Tokyo has little to no control over the factors that are currently weakening the Yen.

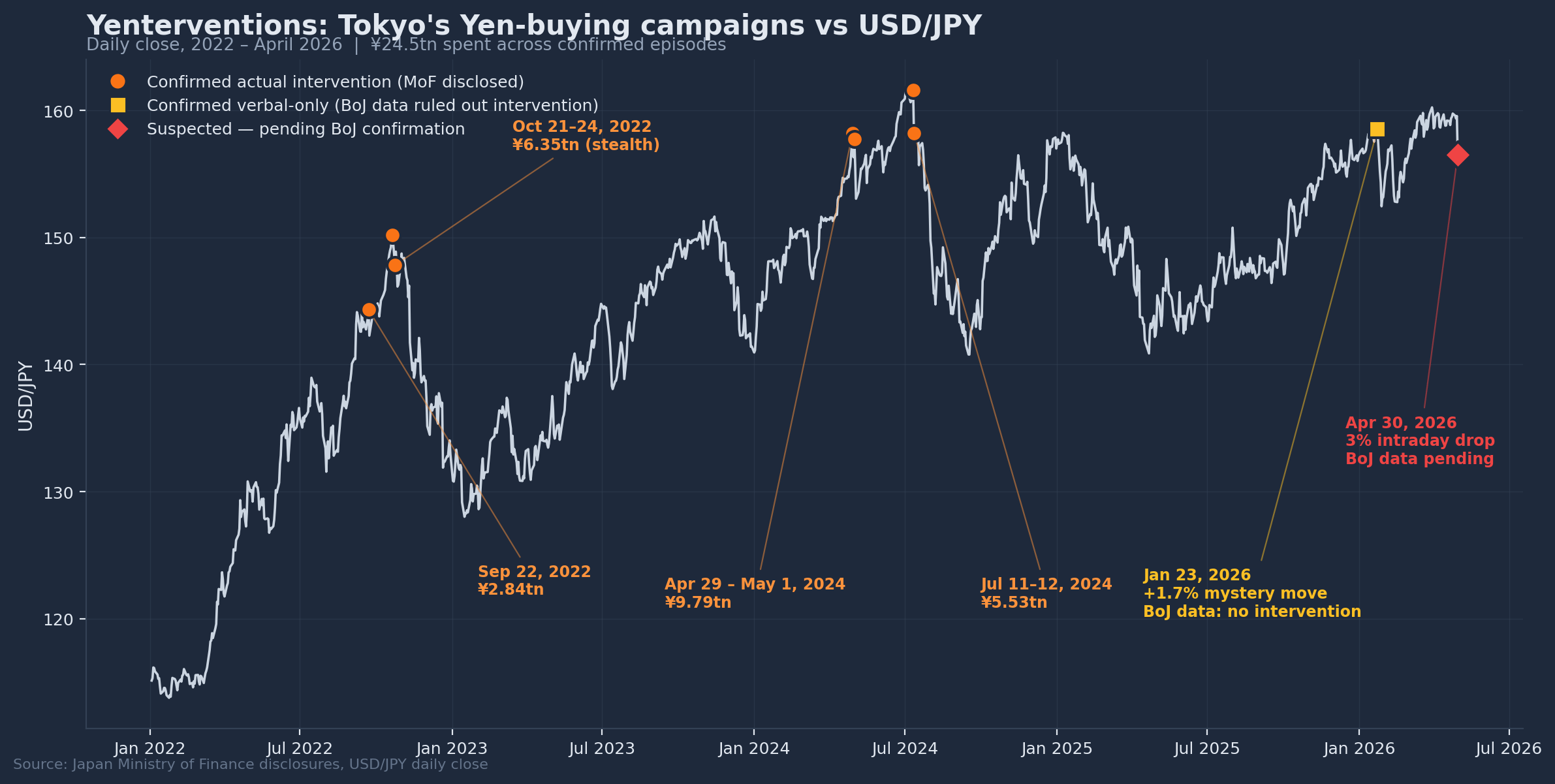

USD/JPY collapsed from intraday highs above 160.00 to a session low near 155.50 on Thursday, a 3% peak-to-trough move not seen in over three years. A Japanese government official confirmed to Nikkei that the Ministry of Finance (MoF) and the Bank of Japan (BoJ) had bought Japanese Yen (JPY) and sold US Dollars (USD) directly on the forex market. The “Yentervention”, the first since July 2024, comes as Tokyo navigates an energy shock driven by the US-Iran conflict. With Japanese government bond (JGBs) at 1997 highs, the BoJ is caught between accelerating imported inflation and a softening national growth outlook.

What Tokyo did, and what it pointedly didn't say

Finance Minister Satsuki Katayama opened Thursday's session by stating the time was drawing near to take "decisive action", her strongest signal yet ahead of the move. Top currency diplomat Atsushi Mimura followed with what he labeled a "final evacuation warning to markets".

The MoF declined to officially confirm the operation, standard practice from Tokyo, but the abrupt collapse from 160.73 to the 155 area within hours, combined with the Nikkei sourcing, leaves little room for doubt. Confirmation of the actual Yen amount spent will come via BoJ daily money market operations data over the next two business days, with the official MoF disclosure due in late May. Katayama also told reporters to keep their smartphones close through next week's Golden Week holiday, a thinly veiled signal that Thursday's operation may not be a one-off. The holiday's notoriously thin liquidity has historically provided convenient cover for follow-up action.

The Iran Oil shock that broke the dam

The intervention came against the backdrop of an unprecedented energy supply disruption. Brent crude briefly touched $126 a barrel intraday Wednesday, its highest level since 2022, before settling above $114 by Thursday's session, while West Texas Intermediate (WTI) Crude Oil traded above $104.

The US and Israel have been at war with Iran since February 28, and the Strait of Hormuz, normally the conduit for around a quarter of seaborne Oil and a fifth of liquefied natural gas, has been choked by a dual US-Iranian blockade since April 13. Goldman Sachs estimates the disruption has removed roughly 14.5 million barrels per day from global supply. For Japan, which imports nearly all of its energy, the math is brutal. Surging crude prices widen the trade deficit and force more Yen-selling in the spot market, a direct mechanical channel for currency weakness that no amount of jawboning can offset.

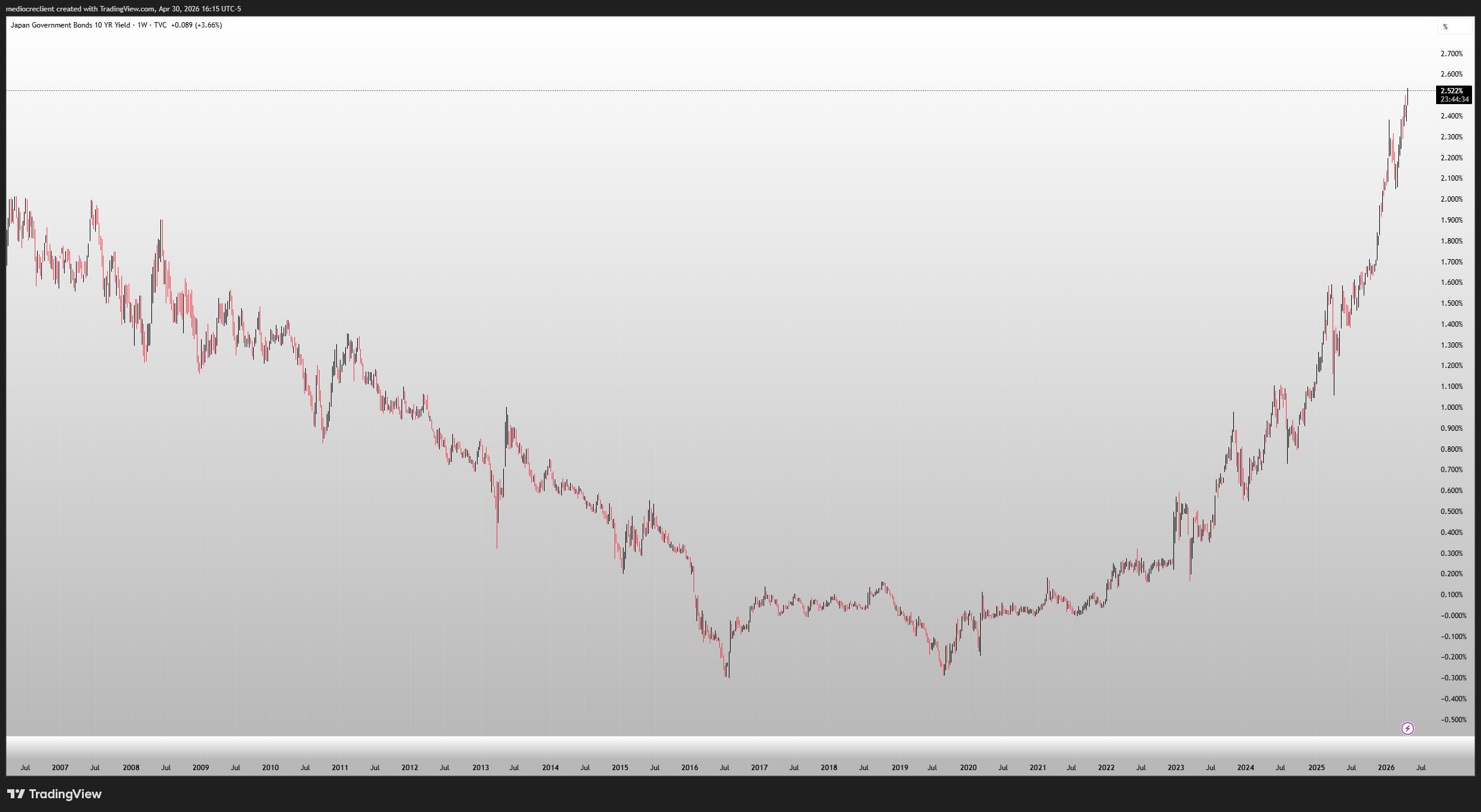

JGB market screams stagflation

Domestic bond markets are flashing the loudest warning. The 10-year JGB yield climbed to 2.535% on Thursday, the highest level since June 1997, as inflation expectations repriced higher. Earlier in the week, the BoJ held its policy rate at 0.75% in a hawkish-leaning 6-3 split vote, with three of nine board members favouring an immediate hike to 1%, the most divided the board has been under Governor Kazuo Ueda. The central bank simultaneously raised its core inflation forecast for fiscal 2026 to 2.8% from 1.9%, while cutting growth to 0.5% from 1%.

The juxtaposition tells the story plainly: imported energy inflation is winning the fight against a still-fragile domestic demand picture, and bond markets have noticed.

The Takaichi paradox tightens

Prime Minister Sanae Takaichi, in office since October 2025 with a ¥21 trillion fiscal stimulus push, openly favoured a weaker Yen on entry. The political logic of that stance has now collided with the Iran reality.

Yen weakness is no longer simply a competitiveness story for exporters; it is an inflation pass-through story for households facing rising fuel and food costs. Moody's Analytics economist Stefan Angrick framed the bind as elevated inflation colliding with softer growth, leaving policymakers with only difficult trade-offs. Tighter BoJ policy supports the Yen and curbs imported inflation but punishes small-and medium-sized enterprises and households dependent on bank credit. Looser policy invites more Yen weakness and more inflation. There is no costless path, and intervention is the one lever that buys time without forcing the choice immediately.

Why is this fight harder than 2024?

Tokyo has now intervened across five confirmed Yen-buying episodes since 2022. The 2022 campaign totaled around ¥9 trillion across two direct interventions with USD/JPY in the 145.00-150.00 range. The 2024 campaign added roughly ¥15.3 trillion across three interventions between 157.00 and 162.00. Thursday’s intervention adds an as-yet-unknown sum to the running tally.

The 2024 fight was, in a sense, straightforward: a Federal Reserve-driven US Dollar story that eventually corrected on its own as Fed rate cuts came into view. 2026’s setup is structurally different; the Yen is weak because Crude Oil is expensive, and Crude Oil is expensive because the Strait of Hormuz is shut, and the shuttering of the Strait is a function of a war Tokyo has no influence over.

Intervention can drain speculative positioning and buy time, but it cannot fix imported inflation from rising energy prices. Talks between Katayama and US Treasury Secretary Scott Bessent in mid-April established Washington’s tacit support under last September’s bilateral FX agreement, so Tokyo at least has the permission slip to continue spending. The harder question is whether the next trillion-plus Yentervention finds enough buyers to dent a structural energy bid, or whether each successive defense simply marks a higher line for speculators to test later.

Has Tokyo bought a few weeks of relief, or just funded an expensive fade?

Japanese Yen FAQs

The Japanese Yen (JPY) is one of the world’s most traded currencies. Its value is broadly determined by the performance of the Japanese economy, but more specifically by the Bank of Japan’s policy, the differential between Japanese and US bond yields, or risk sentiment among traders, among other factors.

One of the Bank of Japan’s mandates is currency control, so its moves are key for the Yen. The BoJ has directly intervened in currency markets sometimes, generally to lower the value of the Yen, although it refrains from doing it often due to political concerns of its main trading partners. The BoJ ultra-loose monetary policy between 2013 and 2024 caused the Yen to depreciate against its main currency peers due to an increasing policy divergence between the Bank of Japan and other main central banks. More recently, the gradually unwinding of this ultra-loose policy has given some support to the Yen.

Over the last decade, the BoJ’s stance of sticking to ultra-loose monetary policy has led to a widening policy divergence with other central banks, particularly with the US Federal Reserve. This supported a widening of the differential between the 10-year US and Japanese bonds, which favored the US Dollar against the Japanese Yen. The BoJ decision in 2024 to gradually abandon the ultra-loose policy, coupled with interest-rate cuts in other major central banks, is narrowing this differential.

The Japanese Yen is often seen as a safe-haven investment. This means that in times of market stress, investors are more likely to put their money in the Japanese currency due to its supposed reliability and stability. Turbulent times are likely to strengthen the Yen’s value against other currencies seen as more risky to invest in.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.