Gold enters credibility test as inflation repricing reaches an inflection point

Key Takeaways

- Gold approaches today’s CPI release after an extended period of yield-driven repricing that has pushed the metal toward key structural support levels.

- The dominant transmission channel remains inflation expectations, real yields and Federal Reserve credibility rather than traditional safe-haven demand.

- Recent price action suggests selling pressure is moderating as markets wait for confirmation from incoming inflation data.

- The CPI report could determine whether the current stabilization phase develops into a broader recovery attempt or extends the prevailing downtrend.

Gold approaches CPI from a position of macro exhaustion

Gold enters one of the most important macro events of the month following a prolonged adjustment in inflation expectations and interest-rate pricing.

Over recent weeks, markets have gradually reassessed the likelihood of rapid monetary easing as economic activity remained resilient and inflation progress appeared less consistent than investors had hoped earlier in the year.

That repricing process has been visible across Treasury markets, the US dollar and precious metals.

For gold, the result has been a persistent decline that pushed the metal toward levels not seen since the previous phase of inflation optimism.

Today's CPI release therefore arrives at a particularly important moment.

The market is no longer debating whether inflation is falling from its peak.

The discussion increasingly revolves around the speed of disinflation and whether price pressures are easing sufficiently to justify a more accommodative policy path.

Gold sits directly at the center of that debate.

As a credibility asset, the metal remains highly sensitive to any information capable of altering expectations for real yields and future Federal Reserve policy.

Inflation remains the dominant transmission layer

The significance of today’s report extends far beyond the headline CPI figure.

Markets will focus on the broader inflation profile and what it implies for monetary-policy flexibility during the second half of the year.

Consensus expectations point to a modest moderation in monthly inflation while annual readings remain elevated.

The key question is whether inflation continues moving toward the Federal Reserve’s objective at a pace that allows policymakers to maintain confidence in the disinflation process.

For gold, this transmission chain remains straightforward.

Inflation data influence Treasury yields.

Treasury yields influence real yields.

Real yields influence the opportunity cost of holding non-yielding assets.

That opportunity cost remains one of the most powerful drivers of gold pricing.

Recent market behavior suggests investors have become increasingly cautious about assuming a rapid decline in rates.

That caution has been reflected in positioning across rates, currencies and precious metals.

Today's CPI report has the potential to reinforce that trend or challenge it.

Positioning remains focused on credibility rather than protection

One of the defining characteristics of recent gold trading has been the market’s emphasis on credibility.

Traditional safe-haven narratives continue playing a role, particularly given ongoing geopolitical uncertainty.

The stronger force, however, has been the interaction between inflation persistence and policy expectations.

Reserve demand remains supportive over the longer horizon.

Central-bank accumulation continues providing an important structural foundation for the metal.

Short-term price behavior, however, remains largely driven by expectations surrounding inflation and rates.

Investors are evaluating whether current economic conditions justify a prolonged period of restrictive monetary settings.

That evaluation continues shaping participation across the gold market.

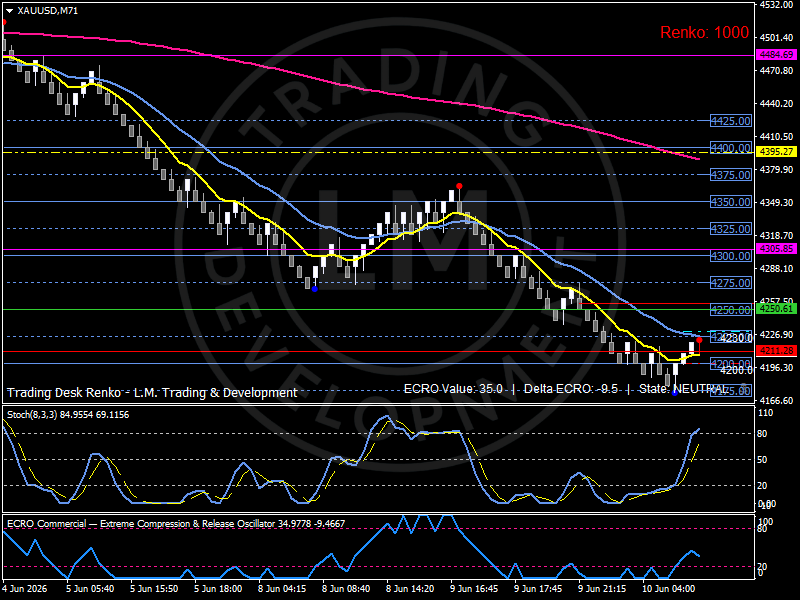

Technical structure: Gold stabilizes after an extended repricing phase

The technical structure reflects a market attempting to stabilize following a significant repricing cycle.

On the H4 timeframe, the broader trend remains negative. Successive downside impulses have dominated recent price action, while recovery attempts have remained relatively limited in scope.

The pace of selling has nevertheless moderated.

That shift is important.

The market is no longer displaying the same degree of directional urgency visible during last week's decline.

On the Renko structure, the 4200 region has emerged as a key stabilization area after absorbing repeated downside pressure.

Recent bricks suggest a tentative recovery attempt is developing, although the broader framework remains below the major participation zones located between 4250 and 4325.

The ECRO indicator has recovered from deeply compressed conditions and now sits near 35, reflecting improving participation after an extended period of weakness.

Momentum has improved.

Conviction remains limited.

Resistance begins around 4250 and strengthens toward the 4325–4350 corridor.

Support remains concentrated around 4200, with the broader stabilization framework extending toward the recent lows.

The overall configuration remains consistent with a market waiting for macro confirmation before establishing its next directional phase.

Bird’s Eye View

Gold currently operates inside a credibility-driven market where inflation expectations and real yields remain tightly interconnected.

Today's CPI release represents the most important catalyst of the week and could reshape expectations for monetary policy, Treasury yields and dollar positioning.

Structurally, the market is attempting to stabilize around the 4200 participation zone, while 4250–4325 defines the first major recovery corridor and 4350 remains the primary upside reference point.

The broader trend remains under pressure.

The immediate structure reflects a market searching for confirmation.

Outlook

Gold enters the CPI release from a position of reduced momentum, improving participation and elevated macro sensitivity.

The dominant question facing investors is whether inflation continues cooling at a pace consistent with greater monetary-policy flexibility.

A softer inflation profile could support a reassessment of real-yield expectations and encourage renewed engagement across precious metals.

A firmer inflation reading would reinforce the credibility repricing that has dominated markets over recent weeks.

Until that uncertainty is resolved, gold is likely to remain primarily driven by the interaction between inflation expectations, Treasury yields and Federal Reserve credibility.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)