Gold at $4,217 – Real yield inflection point ahead of US CPI

XAU/USD has staged a modest recovery to $4,216 after printing lows near $4,171 in early Wednesday trade, but the bounce remains shallow and unconvincing against a backdrop of rising real yield expectations. The session's defining question is whether today's US CPI print delivers an inflection point for real rates — the single variable with the most direct inverse relationship to gold's price. Until that data lands at 3:30 PM UTC+3, the metal is effectively in a holding pattern between two well-defined technical boundaries.

Key levels

- Bias: Cautiously Bullish above $4,195 | Bearish below $4,171.

- Support: $4,194 → $4,171 → $4,137.

- Resistance: $4,218 → $4,262 → $4,280.

- Session target: $4,262–$4,280 on soft CPI.

- Invalidation: $4,171 — break reopens $4,137 and $4,120.

The core argument

The mechanism connecting today's CPI data to gold is direct and well-established: headline CPI y/y is forecast to accelerate to 4.2% from a prior 3.8%, while core CPI m/m is expected to decelerate to 0.3% from 0.4%. The divergence between these two readings is itself the critical variable. A hot headline driven by energy and food — rather than persistent core services inflation — would represent a less structurally hawkish outcome for the Fed than the number alone implies. In that scenario, real yields would be unlikely to reprice materially higher, removing the primary headwind that drove Tuesday's breakdown from $4,337.

Gold's selloff from $4,375 to $4,171 over the past 36 hours was not driven by a fundamental deterioration in the macro case for the metal — it was driven by a single data point, ADP employment, which temporarily repriced Fed rate cut expectations. The longer-term structural support for gold remains intact: central bank demand from non-Western reserve managers continues to operate as a price floor, fiscal deficits are running at historically elevated levels, and the US 10-year real yield has not broken materially higher despite the nominal yield holding near 4.47%. When nominal yields rise without a corresponding rise in real yields — as occurred repeatedly in 2024 — gold historically absorbs the pressure and resumes its uptrend.

The Federal Budget Balance data due at 9:00 PM UTC+3 provides a secondary lens on this dynamic. A deficit print near the forecast of -$282.9 billion reinforces the structural case that US fiscal conditions remain gold-supportive over the medium term. Markets increasingly price fiscal sustainability risk into dollar-denominated assets, and gold benefits from that repricing in a way that short-term rate differentials do not fully capture.

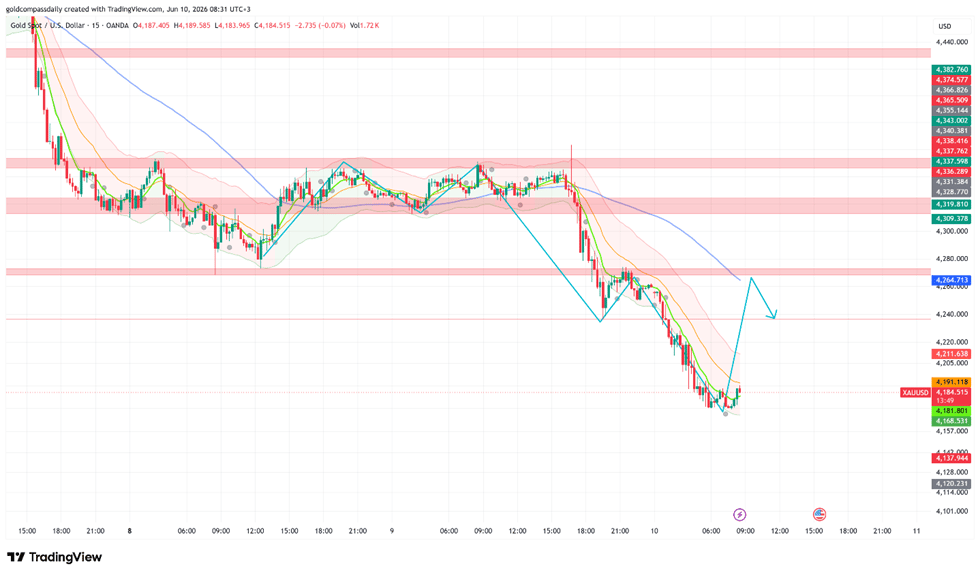

Chart context

The 15-minute chart shows XAU/USD recovering from a low of approximately $4,171 with a sharp V-shaped move higher to the current $4,216 area. Price has reclaimed the $4,194–$4,205 demand zone and is now testing the short-term EMA resistance, which has flattened following the steep decline. The Bollinger Bands are beginning to contract after an extended lower-band run, suggesting momentum exhaustion. The chart's projected path points toward a corrective bounce to $4,262 before another test of support — a structure consistent with a relief rally rather than a trend reversal. Resistance at $4,218 is the first meaningful ceiling; a clean break opens the path to $4,262 and potentially $4,280 ahead of CPI.

Risk scenario

The thesis breaks down if CPI m/m prints at or above 0.5% consensus with core CPI holding at 0.4% — a combination that would signal broad-based inflationary persistence and force a hawkish reassessment of the Fed's timeline. In that scenario, the dollar would likely strengthen materially, real yields would push higher, and gold's $4,171 low would be retested within the session. A sustained break below $4,171 would shift the intraday structure firmly bearish and expose the $4,137–$4,120 demand cluster that represents the next meaningful institutional support area.

Events to watch

Wed 3:30 PM UTC+3 — US Core CPI m/m & CPI y/y: Primary catalyst; determines whether the Fed's rate path accelerates or stabilises, directly driving real yield and dollar dynamics for gold.

Wed 4:45 PM UTC+3 — BOC Rate Decision & Statement: Hold expected at 2.25%; dovish language would pressure CAD and contribute to broader USD sentiment shifts.

Wed 8:01 PM UTC+3 — US 10-Year Bond Auction: Weak demand (rising yield) would add late-session pressure on gold; strong demand would support a continued corrective bounce.

Wed 9:00 PM UTC+3 — US Federal Budget Balance: Deficit data reinforces medium-term structural gold demand thesis through fiscal sustainability risk premium.

Thu — ECB Rate Decision: Potential dovish pivot from Frankfurt would widen the Fed-ECB policy divergence, a medium-term constructive factor for gold via euro weakness and safe-haven demand.

This content was partially created with the assistance of an AI tool. This article is for informational and educational purposes only and does not constitute financial advice.

Author

Tihomir Gospodinov

Independent Analyst

I have been actively following and analyzing financial markets for over nine years, with a primary focus on precious metals, particularly gold and silver, as well as broader macro-driven assets including equities, indices, and cryptocurrencies.