GBP/USD Weekly Forecast: More pain in the offing on Fed-BOE contrast

- GBP/USD booked a large weekly loss and closed below 1.2900.

- Fed’s Powell powers the USD, highlights policy imbalance with Bailey.

- Downside bias remains intact, as technical setup keeps favoring bears.

GBP/USD saw a down week and almost tested the 1.2900 threshold, making the previous week’s rebound look like an aberration to an ongoing multi-month downtrend. GBP bulls did try to recapture 1.3100 in the second half of the week but the US dollar demand remained unparalleled. The pair readies for the critical US economic releases in the week ahead while the UK docket appears relatively quiet.

GBP/USD: Sellers returned with a bang

In a quiet start to a week dominated by central bankers, the US dollar reigned supreme, as Treasury yields mooned on the back of hawkish Fed commentary. Markets priced in roughly a 70% chance of double-dose Fed rate hikes in May, as well as, in June after US inflation soared to a four-decade high of 8.5% in March. A lack of progress on the Russia-Ukraine diplomacy front kept investors on the edge while underpinning the dollar’s haven demand.

Meanwhile, Easter Monday-induced thin trading exaggerated the bearish bets on GBP/USD, as the same hawkish Fed narrative extended into Tuesday. The currency pair closed in on the previous week’s low of 1.2973 on Tuesday, as the Fed’s hawkish outlook continued to power dollar bids alongside the yields. St. Louis Fed President James Bullard made a case for a 75 bps rate hike if needed. His comments sent the benchmark 10-year Treasury yield closer to the key 3% level. In the absence of any significant economic releases from both sides of the Atlantic, the sentiment driven by the Fed’s expectations continued to influence cable.

On Wednesday, the major snapped a four-day downtrend and rebounded firmly to 1.3070 after the US dollar corrected sharply, with the yields from two-year highs tracking the quick retracement in the USD/JPY pair. Further, the greenback also took a beating after the euro surged on hawkish remarks from ECB policymaker Martins Kazaks, citing that “a rate hike is possible as soon as July.” The hawkish shift in the ECB policy guidance continued to be voiced by several policymakers on Thursday as well.

The party for GBP bulls, however, crashed after the greenback staged a V-shaped recovery after the yields on US bonds jumped on Fed Chair Jerome Powell’s remarks at the IMF event. Powell endorsed front-loading rate hikes, confirming a 50 bps lift-off in May. Cable ran into offers just below 1.3100 and tumbled towards 1.3000. BOE Governor Andrew Bailey also spoke at an event on Thursday and expressed his concerns over a slowdown in UK economic growth.

Friday’s disappointing UK Retail Sales and S&P Global Services PMI accentuated the BOE’s dilemma, knocking the pound to its lowest level since November 2020 below 1.2900 vs. the dollar. UK Retail Sales dropped -1.4% over the month in March vs. -0.3% expected and -0.5% previous. Meanwhile, the Preliminary UK Services Business Activity Index for April slipped to 58.3 versus March’s 62.6 and 60.0 expected.

The data from the US showed on Friday that the business activity in the private sector expanded at a softer pace than expected in April with the S&P Global Composite PMI dropping to 55.5, compared to analysts' estimate of 58.1. Nevertheless, the dollar preserved its strength and didn't allow GBP/USD to stage a convincing recovery. Finally, BOE Governor Bailey reiterated that inflation in the UK was expected to go higher due to rising energy prices.

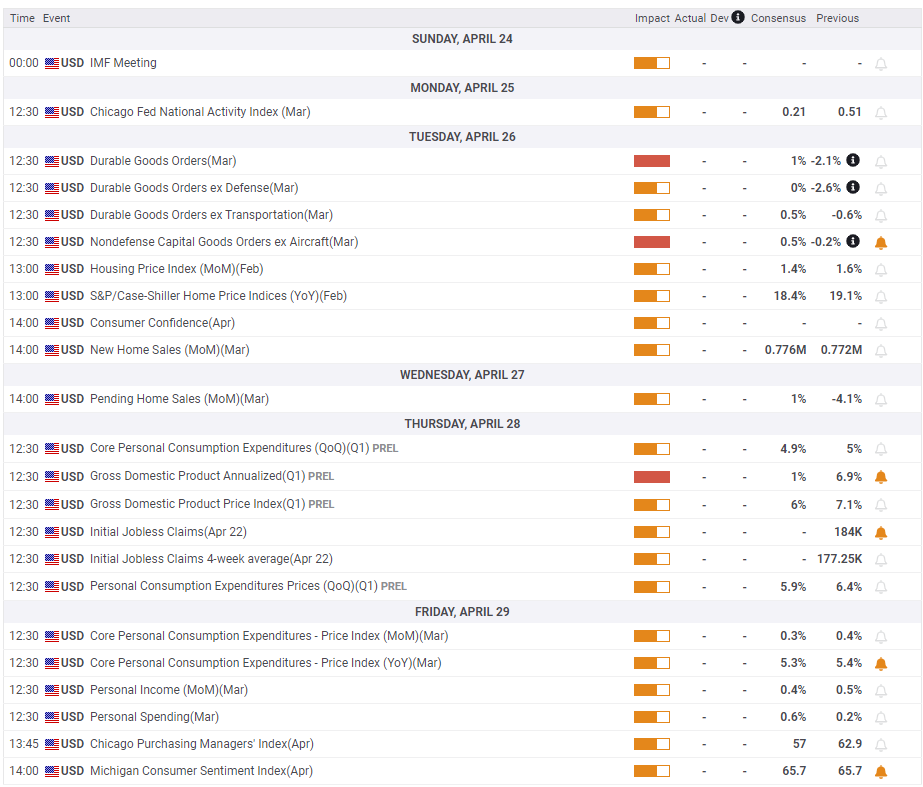

Week ahead: US GDP stands out amid Fed’s ‘blackout period’

There is nothing significant, in terms of top-tier economic releases from the UK in the first half of the week. Therefore, GBP/USD will continue to follow US dollar price action driven by sentiment around the bond market.

On Tuesday, US Durable Goods Orders and CB Consumer Confidence will be published, although these are unlikely to have any impact on the market’s pricing of the Fed’s tightening plans. The low-impact UK CBI Realized Sales, US Goods Trade Balance and Pending Home Sales will drop in.

Thursday’s Preliminary US Q1 GDP is likely to be the main event risk for the week, as the American economy is seen expanding by just 1% vs. a 6.9% growth reported previously. Slowing growth and softer core inflation, however, may do little to change the aggressive Fed tightening expectations and the demand for the US currency. Besides, the weekly US Jobless Claims will also be published in parallel.

Next of relevance will be the Fed’s preferred inflation gauge – the core PCE Price Index, slated for release on Friday. There will be no speeches from Fed policymakers, as the central bank has entered its ‘blackout period’ ahead of the May 4 Fed decision. The Fed-BOE monetary policy divergence theme and the dynamics of the yields will remain in play.

GBP/USD: Technical outlook

With Friday's sharp decline, GBP/USD pierced through 1.3000 and triggered a technical selloff. The Relative Strength Index (RSI) indicator on the daily chart is within a touching distance of 30. If the RSI drops below that level, a technical correction beyond 1.2900 (psychological level) could be witnessed in the short term but buyers are likely to remain on the sidelines as long as 1.3000 (psychological level, static level, descending trend line) resistance stays intact. Only a daily close above that level could open the door for an extended rebound toward 1.3100 (psychological level, static level).

On the downside, the next bearish target aligns at the 1.2790/1.2800 area (static level from September 2020, psychological level). In case this support fails, additional losses toward 1.2675 (September 23, 2020, low) could be witnessed.

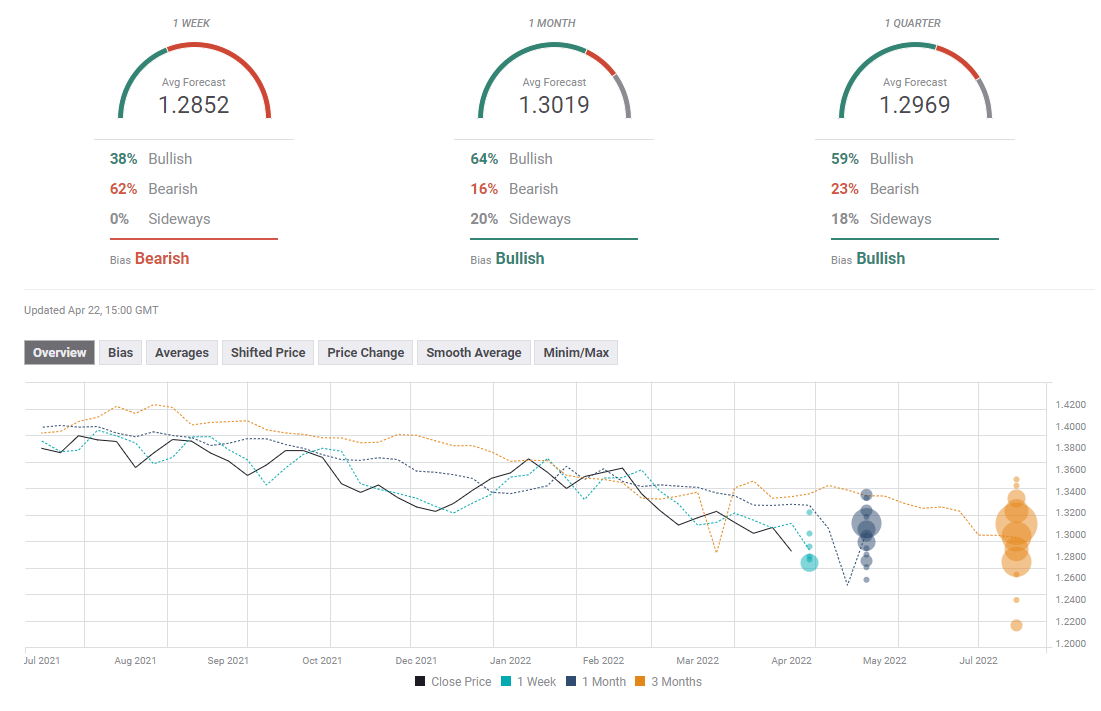

GBP/USD: Sentiment poll

The FXStreet Forecast Poll points to a bearish shift in the near term with several experts seeing GBP/USD trade below 1.2800 on the one-week view. The bullish bias stays intact on the one-month outlook but the average target of 1.3019 suggests that gains are likely to remain limited.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.