DAX at record highs while Germany struggles: Why the paradox is not what it seems

The German DAX index reached a fresh all-time high of 25,900 on Monday after five consecutive days of gains. The benchmark has rallied more than 4% over the past week and more than 16% since its March low, recorded after the outbreak of the Iran war. At first glance, this performance appears difficult to reconcile with Germany's economic backdrop, which remains characterized by weak growth, a struggling industrial sector and persistently high energy costs.

The divergence raises an obvious question. How can Germany's benchmark equity index continue to reach record highs while Europe's largest economy is still battling weak growth, industrial headwinds and mounting structural challenges? The answer is more nuanced than it may first appear and extends well beyond Germany's domestic economy.

Germany's economy remains under pressure

Germany remains the largest economy in the Eurozone and one of the world's leading industrial powers, but its economic model is facing mounting challenges.

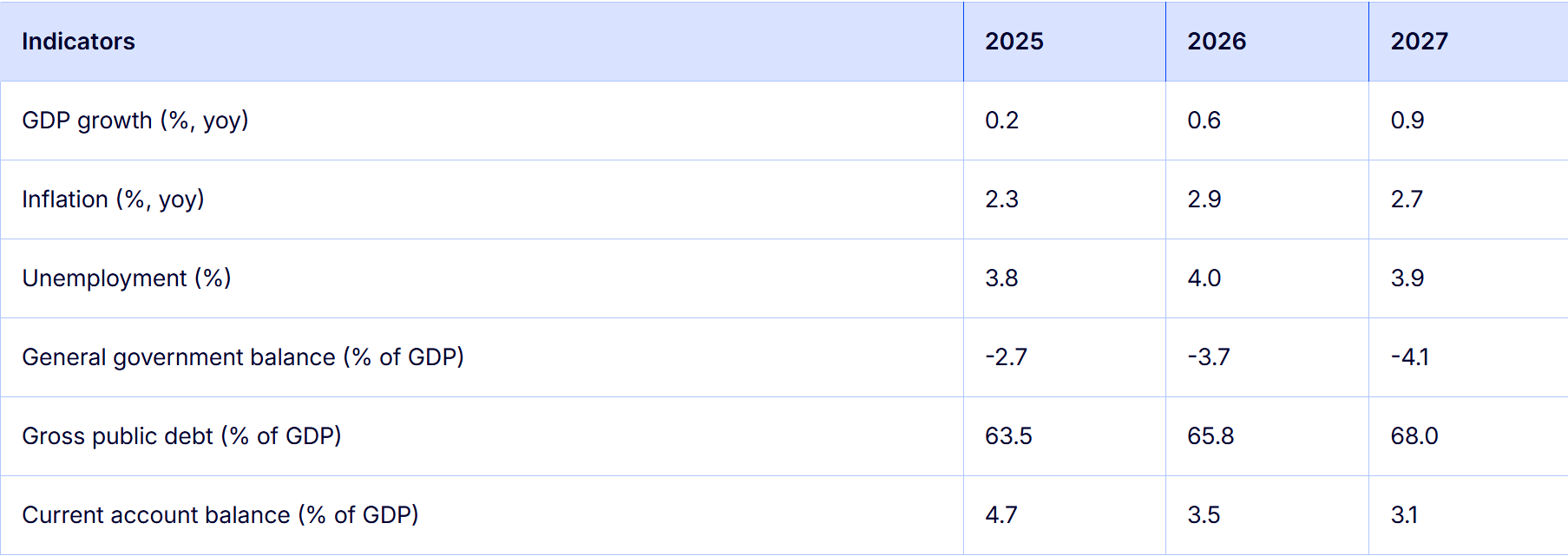

After several years of stagnation, the growth outlook remains modest. The European Commission forecasts Gross Domestic Product (GDP) growth of 0.6% in 2026 and 0.9% in 2027, while several German research institutes lowered their previous forecasts, expecting growth of around 0.5% this year.

The headwinds are well known. Energy costs remain elevated, external demand has softened, exporters face higher US tariffs and Chinese competition is intensifying across sectors where Germany has traditionally excelled, including machinery, capital goods, chemicals and automobiles.

Germany's Mittelstand, the backbone of its industrial economy, has been particularly affected. These mid-sized manufacturers, often highly specialized and export-oriented, are facing increasingly aggressive competition from Chinese firms benefiting from lower production costs and rapidly improving product quality. In several industries, Chinese manufacturers are now offering products comparable to European standards at significantly lower prices.

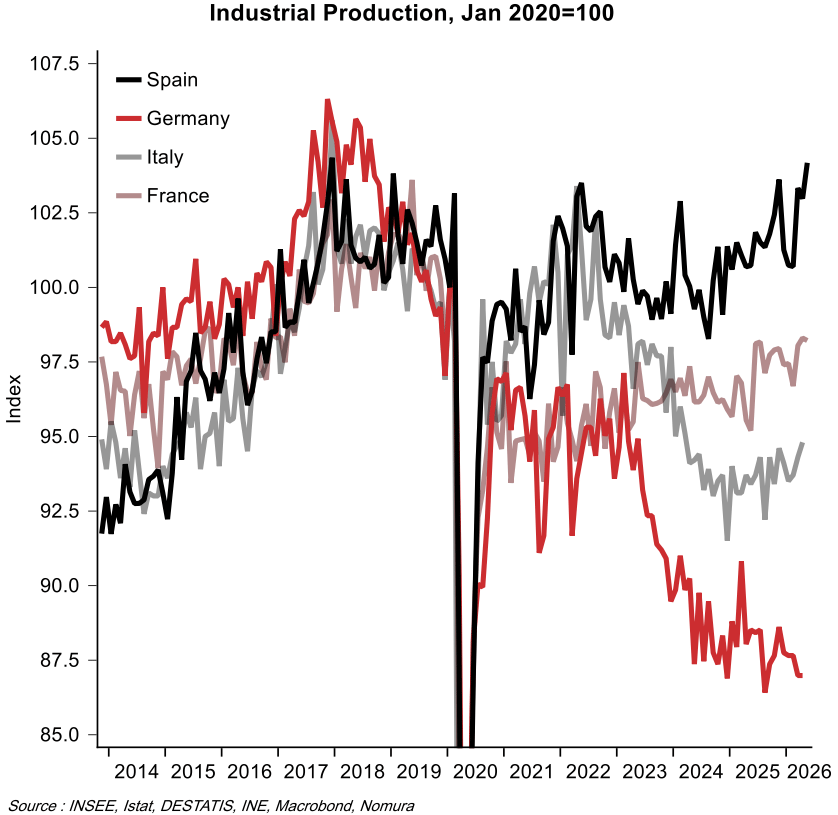

The consequences are becoming increasingly visible through job losses, production relocations and declining competitiveness. According to a Wall Street Journal report citing EY, German industry is losing more than 10,000 jobs every month, while industrial output has declined by around 10% since early 2022, with energy-intensive sectors down by more than 15%. This has reinforced concerns about a structural crisis, even as equity investors are already looking beyond the current economic slowdown.

Why the DAX continues to rally

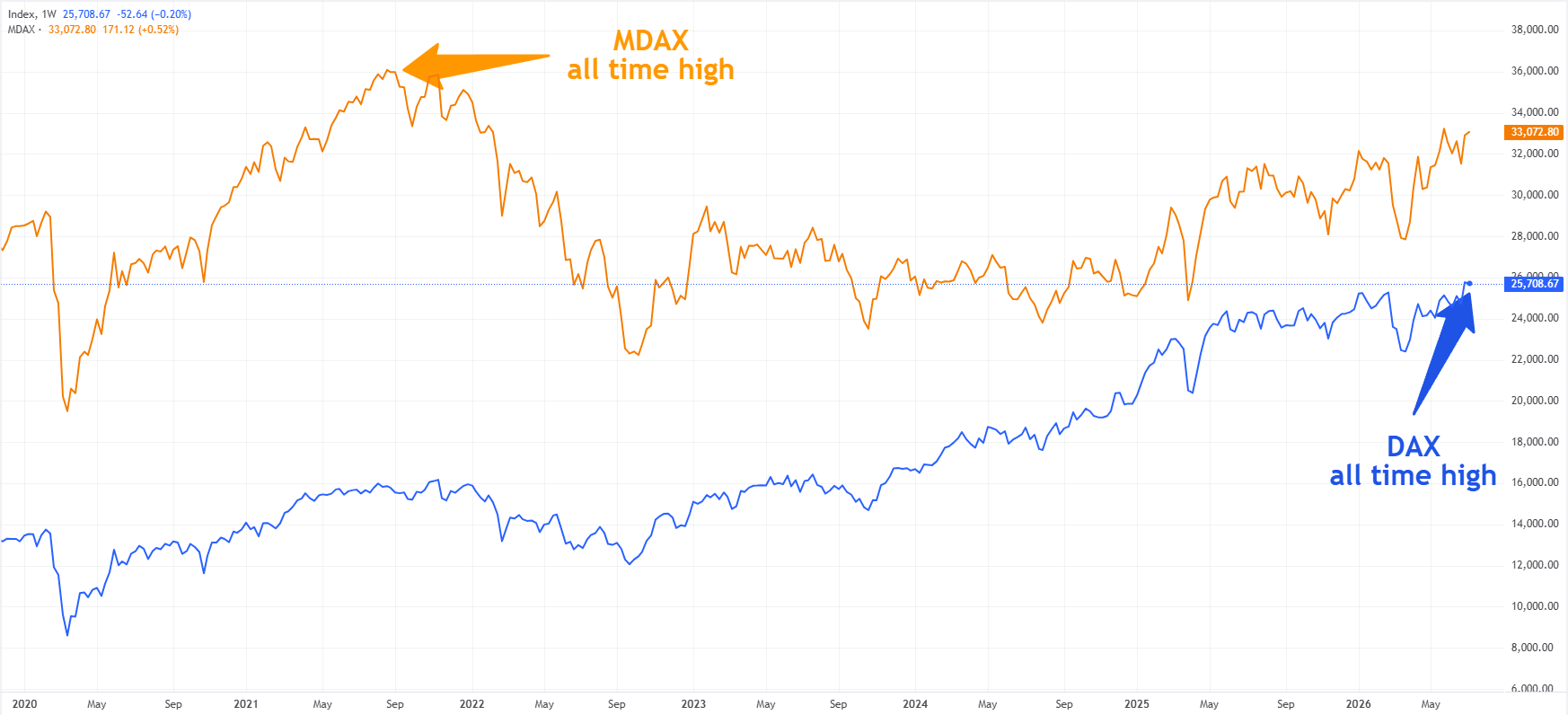

The first explanation lies in the composition of the index itself. The 40 companies included in the DAX generate the majority of their revenues outside Germany. Their performance therefore depends far more on global demand, international profit margins, artificial intelligence, defense spending, financial services and healthcare than on German domestic consumption.

The divergence with the MDAX illustrates this point clearly. The MDAX, which has greater exposure to medium-sized companies and the domestic economy, remains more than 9% below its all-time high reached in September 2021, while the DAX continues to set fresh records. This gap highlights that Germany's global champions tell a very different story from companies that are more closely tied to the domestic economic cycle.

The second driver of the rally is the improving perception of Germany's economic policy. Chancellor Friedrich Merz's government has unveiled one of the country's largest reform packages in decades, covering taxation, pensions, labor market flexibility and deregulation.

According to Deutsche Bank economist Marion Mühlberger, the package demonstrates that the coalition partners are willing to compromise and intend to implement structural reforms before the end of the year. She believes this should improve business sentiment and supports the bank's expectation that economic growth will accelerate during the second half of the year.

Markets are betting on reforms and fiscal expansion

Investors are not simply reacting to reforms that have already been implemented. More importantly, they are pricing in the prospect of a structural turnaround. Germany has reformed its constitutional debt brake while creating large special funds dedicated to infrastructure, defense and the energy transition. This represents a significant shift for a country long associated with strict fiscal discipline.

Fiscal expansion is gradually feeding into the economy. Defense spending is increasing sharply, infrastructure investment is expected to accelerate, and public procurement should encourage private companies to expand production capacity.

Deutsche Bank expects German fixed investment to gain momentum during the second half of the year before increasing by almost 4% in 2027. The bank forecasts GDP growth of 0.5% in 2026 and 1.3% in 2027, supported by government consumption, investment spending and positive spillover effects into the private sector.

Financial markets therefore appear to be focusing less on current economic weakness than on the possibility of an inflection point. As Deutsche Bank's Jim Reid notes: "There appears to be growing optimism that Germany’s recent reform announcements may finally translate into something meaningful, particularly when combined with the significant fiscal stimulus unveiled last year. Enthusiasm for the German trade faded towards the end last year, with the Iran conflict adding another layer of uncertainty. However, some green shoots of optimism now seem to be re-emerging."

The limits of the equity market rally

That does not mean the challenges have disappeared. The announced tax cuts remain relatively modest and will only take effect from 2027 onward. The gradual increase in the retirement age, labor market reforms and efforts to reduce bureaucracy may improve Germany's long-term growth potential, but their economic impact will take time to materialize.

Germany also continues to face a structural competitiveness challenge linked to energy costs since cheap natural gas supplies from Russia were cut. Without more affordable energy, energy-intensive industries remain vulnerable. The Iran war has once again highlighted how exposed Germany's economic model remains to commodity price shocks and geopolitical disruptions.

Chinese competition represents another structural challenge. European trade defense measures may slow the pressure, but they are unlikely to restore competitiveness unless Germany also modernizes its industrial base, infrastructure, public administration and investment environment.

Record highs do not yet signal an economic renaissance

The DAX reaching new record highs does not necessarily mean Germany's economy is performing strongly. Rather, it suggests that investors believe Germany's largest multinational companies can continue creating value despite domestic economic weakness, while also betting that Berlin is finally beginning to address the country's structural problems.

The record highs therefore represent less a verdict on current economic conditions than a wager on Germany's future. Investors are betting on a country becoming more willing to spend, more committed to structural reforms and more capable of transforming fiscal commitments into investment, productivity gains and stronger long-term growth.

For that optimism to translate into a genuine economic recovery, however, the improvement will need to extend well beyond the large multinational companies that dominate the DAX. A more convincing recovery would require Germany's Mittelstand, private investment, construction activity and industrial exports to begin participating in the rebound.

For now, Germany continues to present two contrasting realities. Financial markets are looking ahead to a cycle of reforms and fiscal expansion, while the real economy remains constrained by high energy costs, demographic challenges, bureaucracy and intensifying Chinese competition. The DAX is already celebrating a recovery scenario, but the German economy still needs to deliver it.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.