Bank of Japan raises rates to 1%, and will end tapering next year

The Bank of Japan raised its policy rate by 25 bp, with one dissenting vote, while deciding to halt tapering from April 2027. The timing of the next hike should depend heavily on the situation in the Middle East. The possibility of an October hike increases if a long-term peace deal is made soon.

BoJ’s decisions were broadly in line with market expectations

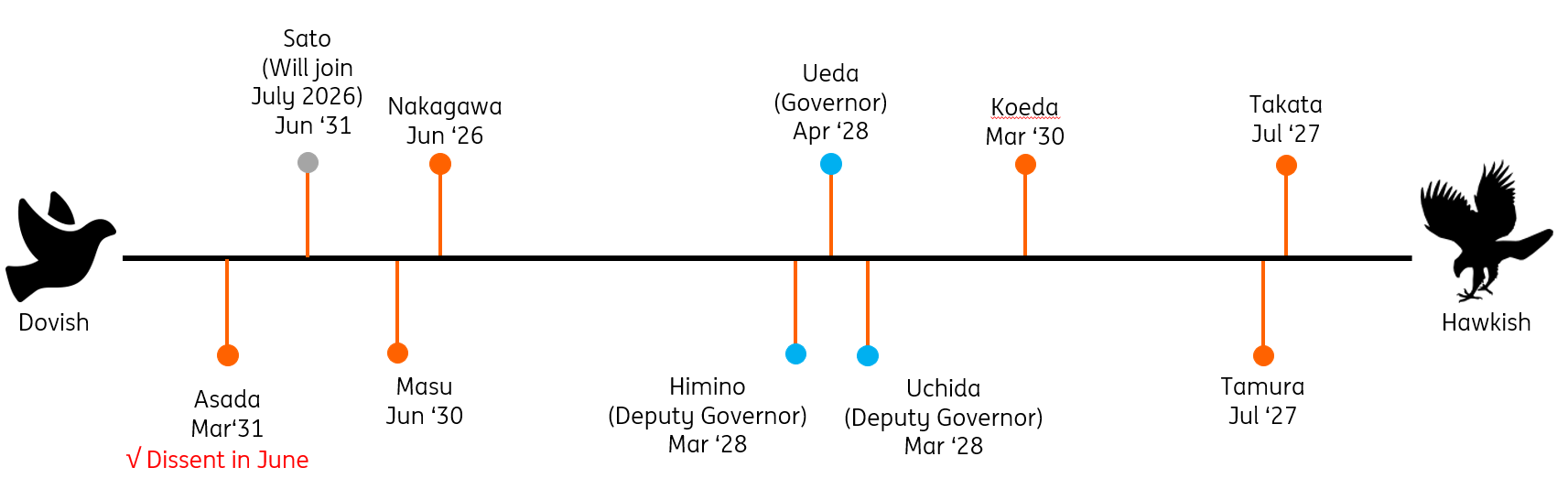

Today’s Bank of Japan rate hike decision was widely expected. With a 7-1 vote, the BoJ highlighted the risk of inflation exceeding the 2% target, while downside risks to the economy have waned. Newly appointed Toichiro Asada cast a dissenting vote. This was not a major surprise given his reflationist stance. He dissented, as he saw that downside risks to production and employment outweighed upside risks to prices. The majority of the board favoured shifting the BOJ's policy focus to inflation risks. From July, another dovish member, Ayano Sato, will join the board. But this will likely leave the board’s dove-hawk balance broadly unchanged. The debates between the hawks and doves are expected to continue in the coming months, and the pace of rate hikes should be only gradual. We’re keeping our base case for the December hike, as the situation in the Middle East remains fluid.

October rate hike is possible if a peace deal reaches soon

At the press conference, Deputy Governor Uchida struck a somewhat hawkish tone in our view. Still, he didn’t give clear guidance on the timing of the next rate hike or the likely terminal rate of the hiking cycle. He spent ample time emphasising upside inflation risks, though, noting that FX pass-through to inflation has increased meaningfully and that the positive wage-price cycle remains firmly in place. He also noted that financial conditions remain accommodative despite rate hikes. He cautioned that the neutral rate is difficult to estimate precisely -- and the wide range of estimates makes it hard to use as a practical policy guide. This ambiguity will likely disappoint market participants.

Listening to Uchida's remarks, the timing of the next rate hike will likely depend on how quickly energy supply disruptions are resolved. The focus seems to be on the possible impact on growth rather than on inflation. If geopolitical risks subside and downside risks to growth ease further, we expect a majority of board members to support another hike. The BoJ is likely to focus less on headline inflation and more on its new price measure. It features core inflation, while stripping out distortions from government measures. As such, it should better capture underlying inflation. The BoJ's preferred inflation measure should stay well above 2% amid firm wage growth, second-round effects from oil price hikes, and a weak JPY.

End of tapering likely to improve market stability

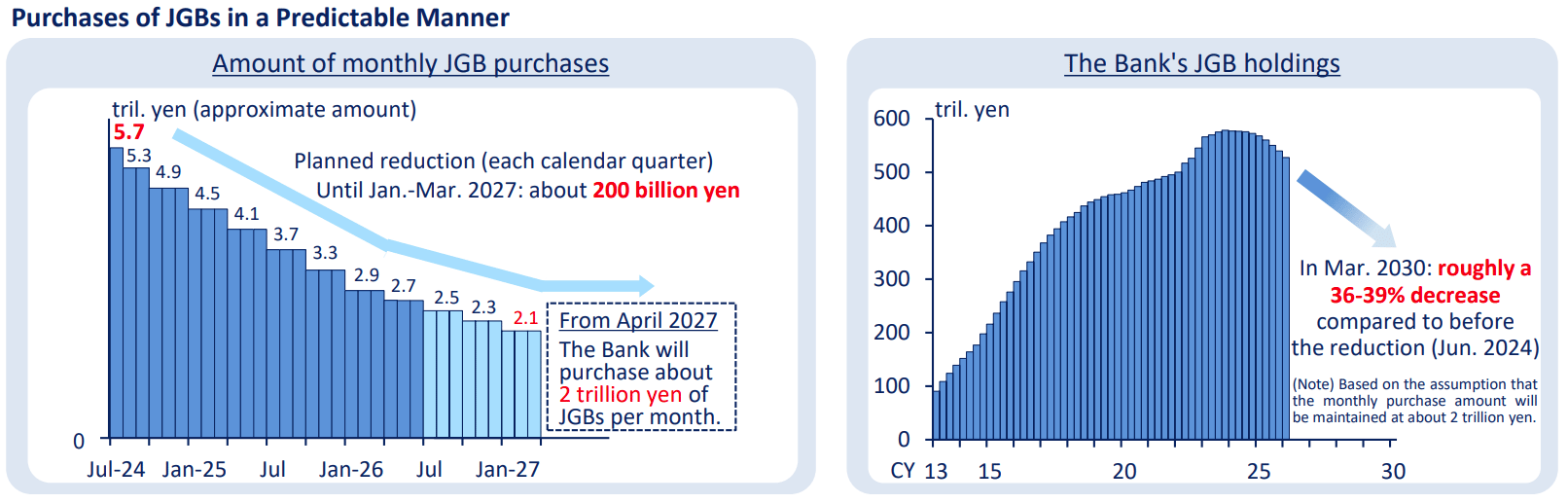

The BoJ decided to halt tapering from April 2027, keeping monthly Japanese government bond (JGB) purchases steady at around JPY 2tn thereafter. It projects its JGB holdings will fall by roughly 40% by March 2027 compared with June 2024.

When the BoJ began tapering back in 2024, it argued that yield-curve control (YCC) and quantitative easing had significantly impaired JGB markets. It held that a gradual reduction in purchases would help restore market-based price action. Since then, the BoJ’s influence over rate markets has weakened substantially. Despite tapering being set to end, its balance sheet should continue to shrink as large redemptions roll off. As market-based pricing has improved, we believe the BoJ now prioritises market stability. This should eventually support further rate hikes in the coming months. Also, it would be easier for the BOJ to convince Prime Minister Takaichi not to oppose rate hikes if the JGB market shows stability. We expect 10-year JGB yields to rise further toward 3.0% and, early next year, even temporarily touch 3.10%. While the BoJ continues to deliver rate hikes, the yield pickup should be much more moderate than it has been over the past year.

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.