Are Cocoa prices poised to rise or fall for the second part of 2024?

Cocoa beans are a fundamental component of the global food industry. While often consumed indirectly through chocolate products, cocoa is a versatile ingredient with far-reaching applications. But the global cocoa market is characterised by volatility, with prices fluctuating dramatically, especially in 2024. These price swings can ripple through the supply chain, impacting the cost and size of our favourite chocolate treats. For businesses and investors, the cocoa market dynamics are complex, bringing both challenges and opportunities. Let's take a closer look.

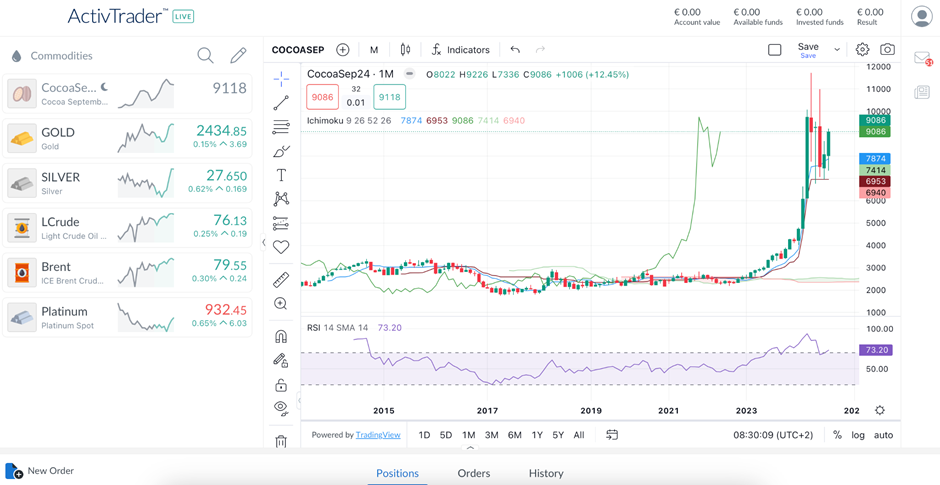

Cocoa prices have had a bumpy ride in 2024 so far

The price of cocoa has skyrocketed in 2024, rising by more than 90% so far. This comes after it increased by a hefty 45% in 2023. According to data provided by ActivTrades, this exceptional surge peaked in April 2024, when prices reached a historic high of $11,776 per tonne, which represents a stunning 175% gain from the beginning of the year until then.

Monthly Chart of Cocoa (Futures on September 2024 Delivery) - Source: ActivTrader

Why did Cocoa prices spike?

The unprecedented surge in cocoa prices is primarily driven by a widening gap between supply and burgeoning demand.

Global consumption of cocoa products is accelerating rapidly. According to Mordor Intelligence, the cocoa beans market is projected to grow at a robust CAGR of 6.81% from 2024 to 2029, reaching a value of USD 23.97 billion by 2029 (up from an estimation of 17.24 billion in 2024).

This growth seems to be fueled by a rising appetite and demand for diverse chocolate products, from milk and dark chocolate to brownies and functional beverages.

Moreover, the industrial chocolate market is experiencing significant expansion. Research and Markets estimates a CAGR of 4.5% between 2023 and 2030, with the market reaching US$81.8 billion by 2030.

This growth is attributed to increasing consumer demand for confectionery, the thriving bakery industry, and the growing popularity of premium and organic chocolate options. The expanding middle class in emerging economies, coupled with technological advancements in chocolate production, is further propelling market growth.

These factors collectively underscore the robust and expanding market for cocoa and chocolate products, intensifying pressure on cocoa supply, which is becoming tighter, as cocoa production has struggled to keep pace.

The global cocoa market has been grappling with a severe supply deficit since 2020. West Africa, the epicentre of cocoa production, accounting for 70% of global output, has been disproportionately impacted.

Climate change has wreaked havoc on cocoa-producing regions, with erratic weather patterns such as droughts, floods, and extreme temperatures disrupting crop cycles and reducing yields. To compound the issue, pests and diseases, notably the Cacao swollen shoot virus, have ravaged cocoa plantations, further limiting production.

The severity of the situation has worsened in the 2023/24 season. According to the May 2024 Quarterly Bulletin of Cocoa Statistics from the International Cocoa Organization, the deficit is now projected to be even larger than initially anticipated.

Major cocoa producing countries have experienced significantly lower cocoa harvests, exacerbating the supply shortage. As a result, global cocoa production is forecast to plummet by 11.7% to 4.461 million tonnes, while cocoa grindings, a measure of chocolate production, are expected to decline by 4.3% to 4.855 million tonnes.

What could be the reasons behind recent Cocoa price jumps?

As demand seemed to be rising while the supply seemed to be slowing down at the time, cocoa prices spiked in April. They have since then lost ground after reaching their record high.

The sharp decline in cocoa prices observed in June 2024 was likely mostly influenced by reports of favourable weather conditions in key cocoa-producing regions, which fostered optimism about the upcoming 2024/25 main crop. This positive outlook tempered market concerns about ongoing supply shortages, according to the ICCO.However, it's important to consider the role of speculative trading in driving price volatility. The rapid price surge in April 2024, as highlighted by Bloomberg, underscored the market's susceptibility to speculative activities. In June, traders may have capitalised on the price increase by adopting a short-selling strategy, contributing to the price decline.

This is supported by the occurrence of backwardation during this period, where future prices of cocoa contracts were lower than current spot prices, indicating market expectations of lower prices in the future.

What should traders expect now?

Over the past two months, prices have rallied by approximately 20%, flirting with April’s closing prices. As we’ve seen, the underlying catalyst for this surge is a record-breaking global cocoa deficit of 475,000 tons projected for the 2023/24 season, primarily attributable to production challenges in West Africa, according to Reuters.

While the market anticipates a return to surplus conditions in the subsequent season, experts predict a gradual price normalisation within a still historically elevated range of $4,000 to $6,000 per ton over the next year and a half, as forecasted by Citigroup. Despite this outlook, the ongoing supply constraints, coupled with robust demand suggest that prices will remain significantly higher than historical averages for the foreseeable future.

These market dynamics present both challenges and opportunities for traders. While the potential for further price increases is evident, the market's volatility underscores the importance of a cautious approach when using specific financial products to take advantage of all market conditions such as Contracts for Difference (CFDs). Leveraged products like CFDs can amplify gains but also magnify losses. Therefore, a deep understanding of market dynamics and risk management strategies is crucial for navigating this complex landscape.

Stay up to date with what's moving and shaking on the world's markets and never miss another important headline again! Check ActivTrades daily news and analyses here.

Author

Carolane de Palmas

ActivTrades

Carolane graduated with a Masters in Corporate Finance & Financial Markets and got the AMF Certification (Financial Markets Regulator in France). Afterward, she became an independent trader, investing mostly in European and American stocks/indices.