Global futures signal fragile relief as Oil pullback offsets geopolitical risk

Where are market today?

Global equity futures are pointing to a modestly higher open across both U.S. and European markets, signaling a fragile relief bounce after recent downside pressure. U.S. futures are edging higher, with S&P 500 futures up around 0.3%, Nasdaq 100 futures gaining 0.2%, and Dow futures advancing approximately 0.4%, while European futures are also trading slightly positive in early sessions. The primary reason behind this upward bias is the sharp reversal in oil prices overnight, which has eased immediate inflation concerns and provided short-term support to equity valuations. Markets are reacting to a shift in tone, where energy-driven inflation fears are temporarily softening, allowing risk assets to stabilize following multiple sessions of declines.

A key driver behind this rebound is the change in geopolitical narrative, where signs of potential de-escalation in the Middle East are beginning to emerge. Developments suggesting a willingness to reduce military engagement—even without full reopening of the Strait of Hormuz—have helped calm immediate supply disruption fears. Additionally, reports confirming that shipping activity is continuing, combined with no escalation following recent tanker incidents, have reduced the urgency of worst-case energy scenarios. This has directly impacted oil prices, pulling them lower from recent highs and removing one of the main pressures weighing on global equity markets.

Another important factor supporting futures is the interaction between monetary policy expectations and recent market positioning. Recent signals indicating that inflation remains under control and that there is no immediate need for further interest rate hikes have provided reassurance to investors. At the same time, the recent equity pullback—bringing major indices close to correction territory—has created conditions for a technical rebound. Markets are increasingly interpreting the recent decline as a normalization phase rather than a structural breakdown, encouraging selective buying activity, particularly in oversold sectors such as technology.

Despite the positive start indicated by futures, the broader environment remains highly sensitive and fragile. Volatility levels remain elevated, and market direction continues to depend on the consistency of incoming economic data, particularly consumer confidence and labor market indicators. The balance between geopolitical developments, oil price movements, and monetary policy expectations will remain the key driver of short-term direction. Unless there is sustained confirmation of easing inflation pressures and stable geopolitical conditions, this rebound is likely to remain cautious and potentially short-lived rather than the beginning of a strong upward trend.

Major index performance as of Tuesday, 31 Mar 2026

- S&P 500: Trading at 6,343.72, down 0.4%, reflecting continued pressure from inflation concerns and narrow market leadership.

- Nasdaq Composite: Trading at 20,794.64, down 0.7%, as mega-cap technology stocks remain under valuation pressure.

- Dow Jones Industrial Average: Trading at 45,216.14, up 0.1%, supported by relatively stronger performance in defensive and financial components.

- Russell 2000: Trading at 2,414.01, down 1.5%, highlighting ongoing weakness in small-cap and rate-sensitive segments.

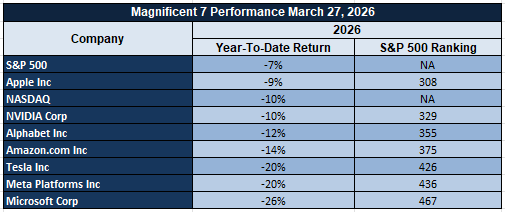

The Magnificent Seven and the S&P 500

The Magnificent Seven — Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla — are increasingly acting as a drag on broader indices. These companies had previously driven a large share of index gains, but are now being repriced as higher interest rates reduce the present value of future earnings. This concentration risk is becoming more visible, with weakness in this group weighing heavily on both the S&P 500 and Nasdaq. Until market leadership broadens, any upside is likely to remain limited and uneven.

Author

Naeem Aslam

Zaye Capital Markets

Based in London, Naeem Aslam is the co-founder of CompareBroker.io and is well-known on financial TV with regular contributions on Bloomberg, CNBC, BBC, Fox Business, France24, Sky News, Al Jazeera and many other tier-one media across the globe.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)