Markets 'buy' Trump’s pivot, but caution is warranted

Risk assets are heading into Friday’s European session with considerably more spring in their step than they had at the start of the week.

The dominant narrative remains centred on tensions in the Middle East. President Trump announced he was calling off planned fresh military strikes against Iran after he had vowed to hit Iran ‘VERY HARD’, threatening to seize its oil infrastructure. The strikes were then called off because of progress in negotiations with Iran. But here is the rub: Iran has stated that no final agreement has been approved by its leadership. We have been here before!

Frankly, I suspect I am not alone in having largely stopped taking Trump’s threats at face value. The telling detail is that oil benchmarks were lower when his strike threat first crossed the wires – the market, it seems, reached the same conclusion. Do not get me wrong: I am grateful and relieved that the strikes did not go ahead; the point is that this back-and-forth between maximum-pressure and imminent-deal messages has made trading in the markets very tough indeed.

Markets, for the most part, are taking Trump at his word about a pullback. Following his announcement to call off the attacks, US equity benchmarks rallied strongly, with the Nasdaq 100 adding 3.3% and the S&P 500 jumping 1.8% by Thursday’s close. Today also marks SpaceX’s Nasdaq debut under the ticker SPCX. The implied valuation stands at roughly US$1.77 trillion, with Starlink accounting for around 70% of revenue. The offering was heavily oversubscribed, though the price-to-sales multiple, north of 90 times, has prompted sceptics to question whether the valuation reflects a business or a set of aspirations.

In the fixed-income space, US Treasury yields bull-steepened following Trump’s announcement, with the 10-year yield falling to 4.45%. In FX, as you would expect, the USD unwound safe-haven demand and fell against most of its peers, losing 0.5% against the JPY. Gold, by contrast, attracted bids from the US$4,098 low formed in late March, ending a two-day losing streak.

ECB hikes rates: Lagarde’s language was key

As widely expected by economists and markets, the ECB pulled the trigger and increased all three benchmark interest rates by 25 bps – a move that raises the main deposit rate from 2% to 2.25% and marks the first hike since 2023.

My key takeaway from the event was not the rate increase, but rather ECB President Christine Lagarde’s language in her presser. You will recall that, heading into the decision, a number of desks suggested this could be a one-and-done rate increase – an ‘insurance hike’. Lagarde was pressed on this in the Q&A and rejected this framing, indicating that further policy tightening could be in the cards. However, in the same breath, Lagarde explicitly refused to offer concrete forward guidance and did not veer far from the meeting-by-meeting, data-dependent script.

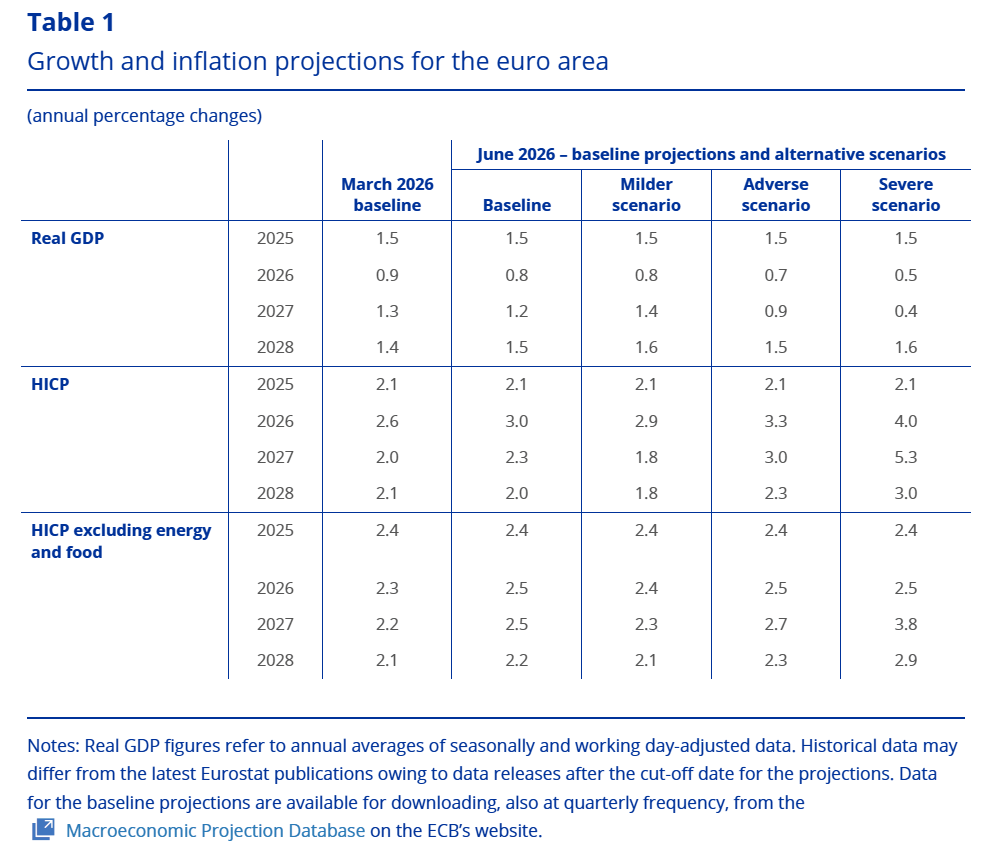

The accompanying projections, as shown above, indicate that inflation is expected to remain around 3% this year (up from 2.6% in the March baseline), before easing to 2.3% in 2027 and reaching the ECB’s 2% target in 2028. In terms of GDP growth, the projection was revised down to 0.8% this year, from 0.9%, with 2027 projected at 1.2% (versus 1.3% in March).

In a nutshell, the ECB is raising rates amid elevated price pressures and slowing growth. For the EUR, while policy tightening generally bolsters the currency, headwinds from meagre growth will simultaneously limit upside potential, leaving the currency in a challenging stagflationary position. Following the recent decision, markets are pricing in 42 bps of further tightening by year-end – meaning two more rate increases could be on the table. This is down from around 65 bps just a week ago.

US PPI: Hot headline but nuanced details

Stateside, the US May PPI inflation data also dropped yesterday, showing that wholesale headline inflation rose 1.1% MM versus the 0.7% forecast, lifting the YY print to a whopping 6.5%, which was slightly higher than the 6.4% consensus and up from April’s reading of 5.7% (revised).

Unsurprisingly, while energy prices drove the bulk of the gains, it is important to note that core PPI – excluding food and energy – came in below expectations, at 0.4% MM versus a 0.5% forecast, and 4.9% YY versus a 5.4% forecast. That is a material miss and suggests the inflation-broadening story beyond energy is not yet running away. It is also worth noting that initial jobless claims came in at 229,000, above the 219,000 forecast, which is a subtle but genuine crack in the labour market narrative that the Fed will not ignore entirely.

Whatever way you swing it, the Fed is in a bind. On one side of the fence, we have a resilient labour market, headline consumer price inflation above 4%, and a PPI pipeline that – even accounting for the softer core print – is running uncomfortably hot.

On the other hand, core CPI is a relatively benign 2.9%, initial jobless claims are creeping higher, and the energy shock driving the headline numbers could deflate rapidly if a deal with Iran materialises. That is precisely the problem: the Fed cannot cut because inflation is too visible politically, and it cannot hike without risking a growth shock on top of a war. Kevin Walsh chairs his first FOMC meeting next week and inherits a mandate that is pulling in two directions.

Day ahead

The University of Michigan releases its preliminary June consumer sentiment reading today at 2 pm GMT, with consensus pencilling in a modest improvement to 46 from 44.8 in May. Given sustained pressure from elevated fuel costs, a miss here would provide meaningful context for how the situation in Iran is landing with ordinary Americans – and, by extension, the political pressure on the White House to close a deal.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,