- USD/JPY forges higher as markets seek dollar balances

- Global demand for safety drives US currency

- Businesses seek cash hedge against economic slowdown

The dollar rally in currency markets this week was propelled by more than its traditional role as the safe-haven of choice as corporations and businesses around the globe sought to amass dollar balances as a hedge against falling revenue and operational and fixed expenses.

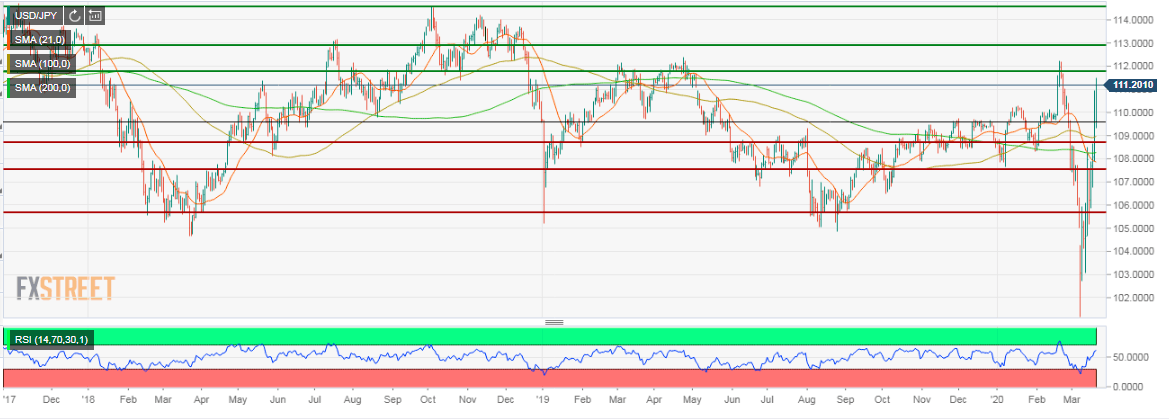

On the week the USD/JPY rose 4.6%, opening at 106.22 on Monday it finished higher each day and was trading at 111.28 near the close on Friday. This put the pair on approach to this year’s high close of 111.97 on February 20th and the 15 month top of 112.12 from April 24, 2019.

Uncertainty about the duration and severity of the economic slowdown that will be caused by the spreading work stoppages and layoffs is the key factor in market calculations. As long as that is true cash and the dollar will remain the twin poles of global markets.

Japanese statistics March 16-20

Monday

The Bank of Japan left its base rate at -0.1% in its meeting which replaced the scheduled Thursday event but doubled the size of its asset purchase program, joining most other central banks in an effort to stem an economic slowdown from the dislocations caused by the Coronavirus.

The bank doubled the purchases of exchange trade funds (ETF) to 12 trillion yen ($112.6 billion) and real estate trust funds (REIT) to 180 billion yen a year until markets stabilize.

“Japan’s economic activity is likely to remain weak for the time being, mainly affected by the coronavirus outbreak,” said the BOJ’s accompanying statement.

The BOJ said it will revert to its original purchase amounts once markets normalize.

The BOJ actions left little imprint on currency markets.

Tuesday

Imports in February fell 14% y/y a bit better than the -14.4% forecast and exports dropped 1%, much less than the -4.3% prediction, reported the Ministry of Finance. It was the 15th straight monthly decline for exports though it was the smallest decrease in that run

Wednesday

National CPI was weaker in February coming in at 0.4% y/y on a 0.8% projection and January’s 0.7% result. Core inflation was lower at 0.6% from 0.8% in January. The forecast was 0.9%.

Thursday

The All Industry Activity Index for January which captures production changes for the whole economy was much stronger than expected at 0.8% after December's flat score.

FXStreet

FXStreet

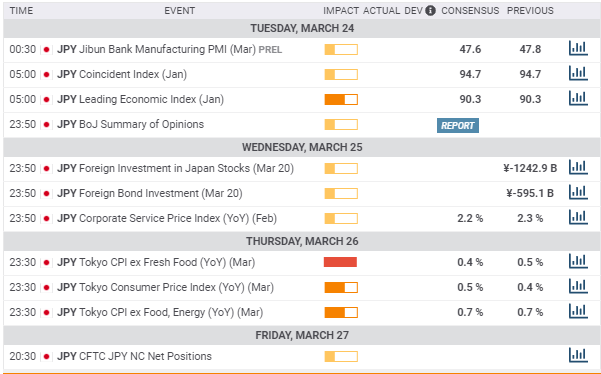

Japan statistics March 23-27

Monday

The Jibun Bank manufacturing PMI for March will provide an early look at the impact of the Chinese quarantines on Japanese manufacturing. It is forecast to slip to 47.6 from 47.8 in February. The index has been below the 50 expansion-contraction division for 10 months with February the low.

Tuesday

The Coincident Index for the whole Japanese economy is forecast to be unchanged for January at 94.7, as is the Leading Economic Index at 90.3.

Thursday

Tokyo CPI is forecast to rise 0.1% in March to 0.5% on the year. Core CPI is expected to be stable at 0.7% y/y.

FXStreet

Japan statistics conclusion

Vital insight into the viral impact on the Japanese economy is limited. February’s much smaller than anticipated drop in exports at -1% will be superseded by the March number.

In the week ahead only the Jibun manufacturing PMI will provide relevant information about the cost of the viral pandemic to the Japanese economy.

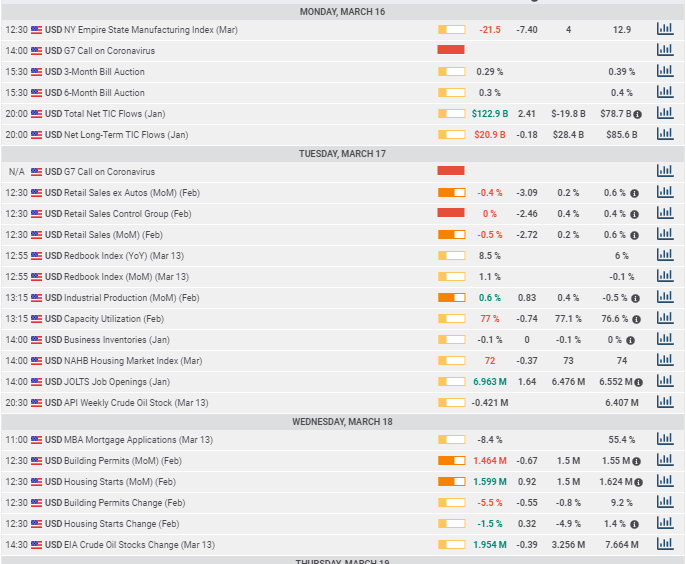

US statistics March 16-20

Monday

The Empire State manufacturing index for March from the New York Fed was far worse than expected at -21.5 for a forecast of -7.4. While New York is not a major manufacturing state the plunge was one of the largest single month drops on record and the weakest reading since March 2009.

Tuesday

Retail sales in February fell 0.5% missing the 0.2% prediction and the control group slipped 0.4%, well under its 0.2% forecast. The January results for both were revised substantially higher, sales to 0.6% from 0.3% and control to 0.4% from 0%.

Industrial production in February rose 0.6%, beating its 0.4% estimate.

Job openings in January, the JOLTS survey from the Bureau of labor Statistics, were 6.963 million, more than the 6.476 million estimate and December’s 6.552 million, confirming what has become passé, the US had an excellent job market before March.

Wednesday

Building permits and housing starts in February were about as predicted, 1.464 million in permits on and 1.599 million starts, both annualized numbers, on identical 1.5 million predictions.

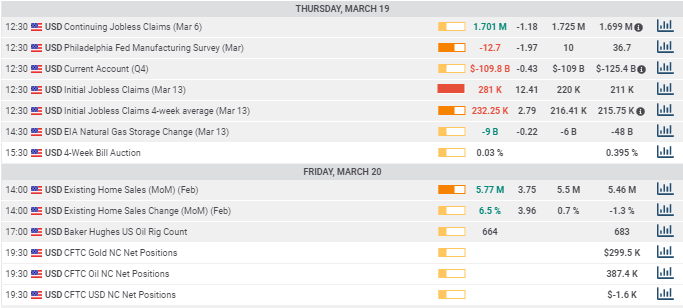

Thursday

In the most relevant figure of the week, initial jobless claims soared in the March 13 week to 281,000 from 211,000. It was the highest weekly total since early September 2017 and the largest one week jump since November 2012.

Initial claims numbers are released every Thursday at 8:30 am EDT for the previous week and will be watched closely as they are expected to surge from the multiplying business closures.

The Philadelphia Fed manufacturing survey for March, like its Northeast counterpart in New York fell precipitously from 36.7 in February to -12.7 a month later. It was the lowest score since June 2012 and the steep drops is indicative of the widespread concern in the business sector.

Friday

Existing home sales, the largest category of the housing market, registered a 5.77 million annualized rate in February, slightly better than the 5.5 million projections and yet another statistic that confirms the buoyant US economy before the epidemic.

FXStreet

FXStreet

US statistics March 23-27

Tuesday

The Redbook Index of same store sales for the week of March 20 which rose 1.1% the prior week, will be watched for weakness in the retail sector. In the general absence of March information this second tier series gains significance.

The Richmond Fed manufacturing index, another regional activity survey, for March is expected to rise to 9 from -2 in February.

Wednesday

Durable good for February are forecast to fall 0.9% after January’s 0.2% drop. The ex-transport figure is thought to decrease 0.2% after a 0.8% gain in January. Non-defense capital goods, the business investment proxy rose 1.1% in January. These numbers will be largely read forward into March, with any unexpected losses given greater note.

Thursday

Initial jobless claims for the March 20 week is the key statistic. The consensus estimate of 214,000 is clearly out of date and a result above the prior week’s 281,000 is likely.

The third and final revision of fourth quarter GDP is expected to be unchanged at 2.1%.

The Kansas City Fed manufacturing activity survey for March, like those of New York and Philadelphia is a regional, normally second level statistic. In the current situation these early reading take on greater importance. The index is expected to drop to 2 in March from 8 in January. It was -4 in January, -3 in December and -5 in November.

Manufacturing in the Kansas Fed district is a much larger part of the local economy and this index will have much more in common with national measures than either the New York of Philadelphia surveys.

US statistics conclusion

The paucity of up-to-date information on the impact of the viral epidemic is one of the biggest problems for all markets. In the absence of fact, speculation, which naturally trends to the defensive extreme has ordered market levels. Statistics from February will be read forward mainly for what they may tell about March.

In the week just ended initial jobless claims and the New York and Philly Fed surveys, all much worse than anticipated and where they would have been absent current circumstances, seemed to confirm the radical nature of the economic shock.

Next week the Tuesday releases of the Redbook Index of retail sales and the Richmond manufacturing survey will provide timely information on nationwide consumption and regional business activity. Wednesday's durable goods orders for February may offer insight into business spending, poorer than expected readings especially in the non-defense capital goods category will suggest worse in March.

Thursday's initial jobless claims will again be the most important number of the week. With layoffs expected to rocket higher the range of expectation for this figure is unusually wide. The Kansas Fed survey will give good idea of the state of business activity and attitudes in the middle of the country.

USD/JPY technical outlook

The relative strength index has lifted this week from modestly oversold to nearly overbought by virtue of the dollar yen's five figure rise from Monday's 106.22 close to 111.28 on Friday. Four days ae not quite enough to bring the index to the top of its range but if the pair sustains it will likely be there by the end of the coming week.

The same brevity applies to the three moving averages, 21-day, 100-day and 200-day. None have reversed higher and the two week decline from February 21 to March 5 has left the 21-day average below both its longer term siblings.

Resistance: 111.82, 112.92, 114.58

Support: 108.75, 107.65, 105.68

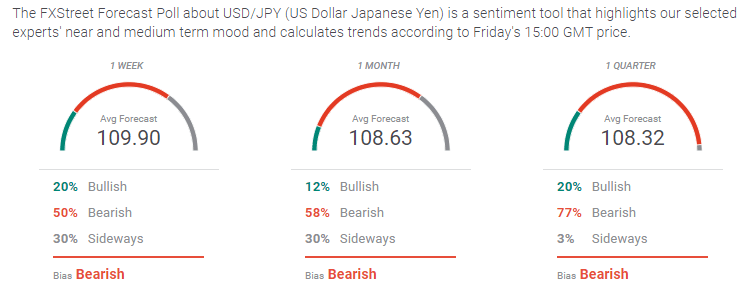

USD/JPY sentiment poll

The ascent of the dollar as the safety currency of choice overwhelmed the yen's regional role for Asia and left the sentiment bearish across all three time frames. The reality of the current situation puts the mean-reversion tendency of most indicators at the mercy of the more emotional reactions of the markets.

The one week view is slightly less bullish, 20% vs 22%, substantially more bearish 50% vs 21% and less undecided 30% vs 57%. The 109.90 forecast is midway between last week's 107.39 and the Friday trading level of 111.16.

The one month view is much weaker for the bulls, 12% vs 61%, decidedly bearish 58% vs 26% and more neutral 30% vs 13%. The forecast at 108.63 from 107.66, is a technical retrace not a fundamental judgement.

The one quarter outlook is far less bullish, 20% vs 70%, highly bearish 77% vs 23% and marginally neutral 3% vs 7%. The forecast of 108.32 mirrors the one month view of technical of technical reversion from last week's 107.73.

As we saw last week the market action and directions of the past two weeks have not run their fundamental course. Until they do technical traders should operate with clear warnings in mind at all times.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

USD/JPY holds near 155.50 after Tokyo CPI inflation eases more than expected

USD/JPY is trading tightly just below the 156.00 handle, hugging multi-year highs as the Yen continues to deflate. The pair is trading into 30-plus year highs, and bullish momentum is targeting all-time record bids beyond 160.00, a price level the pair hasn’t reached since 1990.

AUD/USD stands firm above 0.6500 with markets bracing for Aussie PPI, US inflation

The Aussie Dollar begins Friday’s Asian session on the right foot against the Greenback after posting gains of 0.33% on Thursday. The AUD/USD advance was sponsored by a United States report showing the economy is growing below estimates while inflation picked up.

Gold soars as US economic woes and inflation fears grip investors

Gold prices advanced modestly during Thursday’s North American session, gaining more than 0.5% following the release of crucial economic data from the United States. GDP figures for the first quarter of 2024 missed estimates, increasing speculation that the US Fed could lower borrowing costs.

FBI cautions against non-KYC Bitcoin and crypto money transmitting services as SEC goes after MetaMask

US FBI has issued a caution to Bitcoiners and cryptocurrency market enthusiasts, coming on the same day as when the US Securities and Exchange Commission is on the receiving end of a lawsuit, with a new player adding to the list of parties calling for the regulator to restrain its hand.

Bank of Japan expected to keep interest rates on hold after landmark hike

The Bank of Japan is set to leave its short-term rate target unchanged in the range between 0% and 0.1% on Friday, following the conclusion of its two-day monetary policy review meeting for April. The BoJ will announce its decision on Friday at around 3:00 GMT.