The Dilemma continues, but the Fed has run out of time

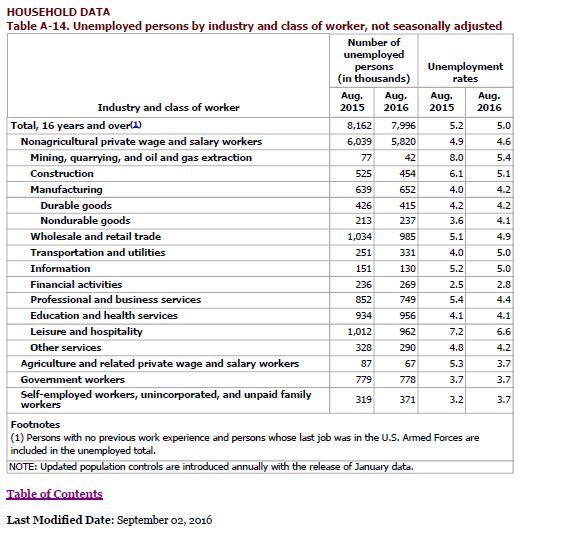

Friday’s job report was supposed to give key figures to investors, to more properly assess chances of a rate hike in September. Instead, numbers added even more uncertainty: 150K new payrolls in August were below average consensus (190k), well below bullish stances (220-230) but definitely not bad enough to completely remove the hypothesis of a move in September. To summarize the other numbers, Unemployment Rate picked up by 0.1% to 4.9% with the Labor Force Participation rate coming in unchanged at 62.8%. Hourly Earnings also increased by 2.4% on yearly basis, continuing with an uptrend in a pickup in earnings that are expected to boost consumer spending and push the economy heading into 2H 2016.

Equity markets reacted positively, in line with a hold on in tightening, but Treasury Yield rose strongly and the US Dollar had mixed reactions, rallying against the Euro and the Japanese Yen, and losing just slightly against commodity currencies. Fed Fund futures also moved marginally, now pricing a 32% chance of a hike in September and 59% in December.

Digging into the numbers, there is definitely a case for keeping ahead with a process of interest rate normalization: With an Unemployment Rate below 5% and Labor Participation Rate stabilizing above 60%, Friday’s numbers show how the US economy, as whole, is still creating jobs. In addition, the most remarkable differences in terms of job creation among different industries have been sensibly narrowing, according to the Bureau of Labor Statistics (BLS) report.

Nevertheless, since the US economy is growing at the slowest pace since almost three years (Actual: 1.2%, Forecasted: 1.8%) it is highly probable that job market will lose track accordingly, receding albeit marginally from its status a fully employed economy. In addition, recent leading economic data in US were modest to weak, the IMF revised down economic growth estimates and in its recent update, before this weekend G20, it painted a gloomy picture at the very least. In such an uncertain global scenario, all relevant central banks are engaging in additional rounds of monetary stimulus (Australia, Canada, United Kingdom, Japan, New Zealand, ECB and Japan) and the remaining are ready to intervene, if necessary.

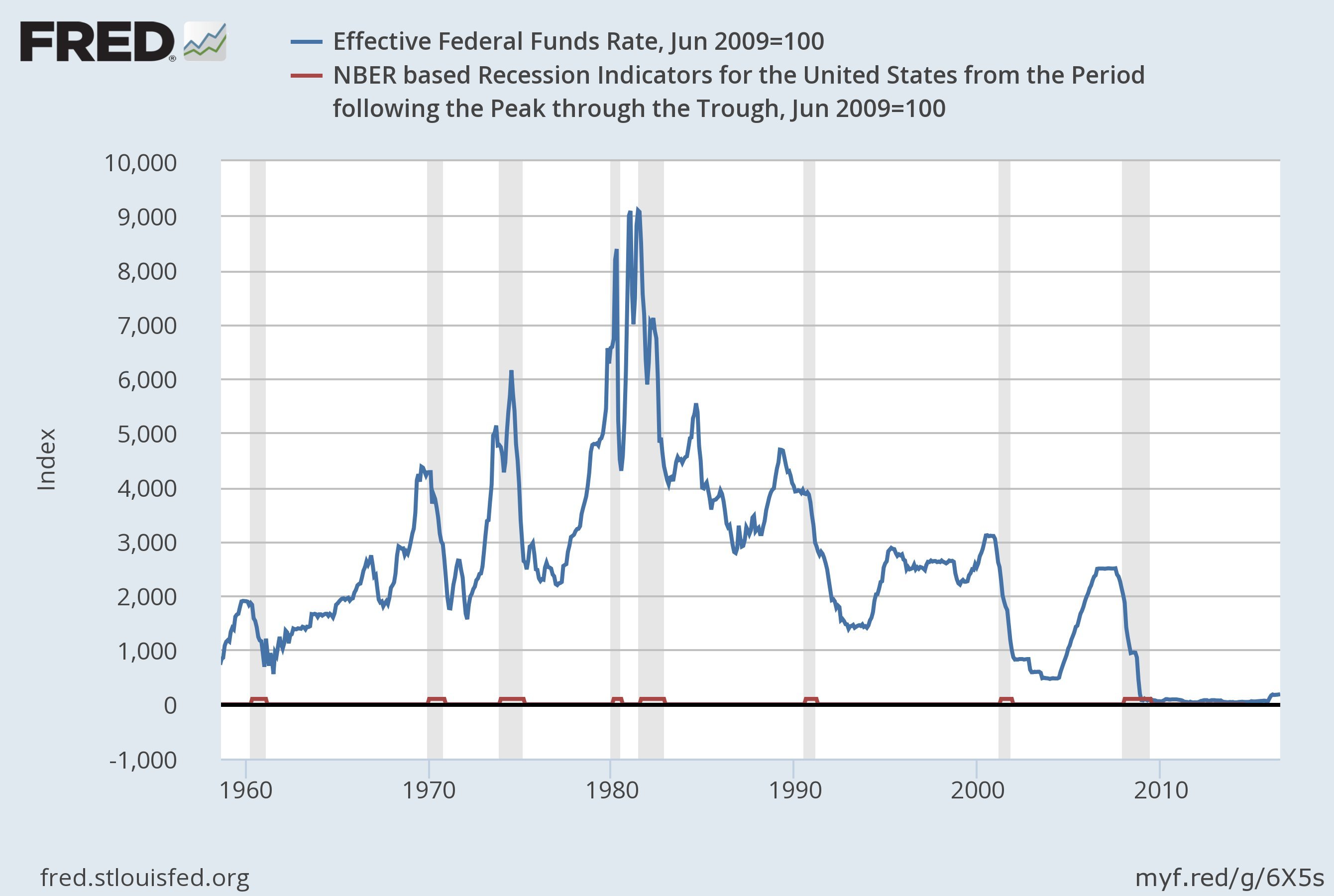

Furthermore, if we extend our view beyond the most recent numbers, we may observe that Fed’s temporal position within the tightening cycle is a key factor that cannot be ignored any longer. Relating the Effective Federal Fund Rate to the evolution of the economic cycle in the US (shaded areas are periods of economic recession), evidently shows how the Fed is clearly too late in the tightening cycle in comparison of where it should be, after six consecutive years of positive economic growth.

In conclusion, the debate on the tightening cycle is likely to continue for a while, but clearly more and more market participants are wondering whether the Fed also would be ready start a new phase of monetary easing, should the global economic scenario turned suddenly to the worse. Going against the tide rarely turns out to be the best solution, even for the Fed.

Author

Edoardo Fusco Femiano, CFTe

Independent Analyst

Edoardo is an independent trader and investment advisor with more than 10 years of experience in Portfolio Management, FX and Equity Trading, Investment Research and Risk Management within primary financial institutions (Vatican B