Most people typically don’t think about exchange rates unless they are heading out of the country. My son had never given the subject much thought until we shared a trip to England last month. Now he understands that $10 is equivalent to two pints in a London pub — not the personal finance lesson I was hoping he would learn.

For those of us who pay closer attention, exchange rates have been very much top-of-mind during the past year. The U.S. dollar has strengthened, while many other leading world currencies have fallen. The new equilibrium has the potential to affect economic growth and inflation around the world.

But the relationship among currencies, prices and trade is not a clear one. Imports and exports may not adjust fully or quickly to changes in relative prices, and results for one country depend on the actions and reactions of many others. Those nations hoping to devalue their currencies and ship their way to better health may ultimately be disappointed.

Currency values are established by supply and demand. In theory, demand is based on the strength of a nation’s underlying economy and markets. Strong growth attracts inbound investment, which requires conversion into the local currency to complete. The supply of a currency is typically tied to monetary policy; easier money means a lower exchange rate, all else equal.

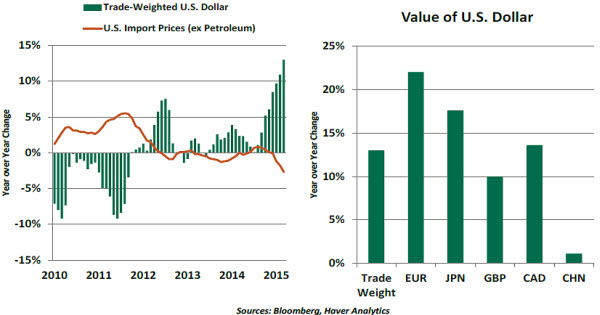

When exchange rates change significantly, they have the potential to affect a country’s trade flows. A stronger currency can make exports more expensive overseas and imports cheaper domestically. We’ve seen this recently in the United States.

To date, falling import prices have had only a very modest impact on U.S. inflation. A large fraction of American imports are priced in dollars, even when oil is excluded. And while the dollar is stronger by 15% overall over the past 12 months, its gains against the Chinese currency have been only 2%. (19% of U.S. imports come from China.) Economists at the Federal Reserve Bank of Cleveland estimate that the dollar’s rise has had an impact of less than 0.1% on the consumer price index.

This illustrates an important aspect of analyzing the relationship between currencies and trade. While certain exchange rates may garner headlines, one must consider a broad basket that reflects the underlying merchandise flows.  Further, the translation of individual currency movements to trade patterns is imperfect and can take a good bit of time to evolve. Exporters may opt to keep their prices unchanged in local currency terms, sacrificing margins to sustain market share. Buyers and sellers often have stockpiles of things they purchase from overseas, while others have contracts to buy things that extend some distance into the future. Forward contracts can lock in exchange rates years ahead, and companies often use these instruments to insulate themselves from currency volatility. So it can take a while before revaluation begins to influence trade prices.

Further, the translation of individual currency movements to trade patterns is imperfect and can take a good bit of time to evolve. Exporters may opt to keep their prices unchanged in local currency terms, sacrificing margins to sustain market share. Buyers and sellers often have stockpiles of things they purchase from overseas, while others have contracts to buy things that extend some distance into the future. Forward contracts can lock in exchange rates years ahead, and companies often use these instruments to insulate themselves from currency volatility. So it can take a while before revaluation begins to influence trade prices.

When prices do adjust, trade flows do not follow automatically. Consumers in some places may not shift from domestic to imported products that easily and may be restrained overall by household debt or a preference for saving. There are some products for which there are no good substitutes and others where the quality or features of one country’s output are seen as superior. In cases where demand is inelastic, exchange rates will have a much smaller impact on trade balances.

And finally, when a spectrum of nations pursues devaluation, relative prices among them may not change all that much. That limits the ultimate impact on exports and economic growth.

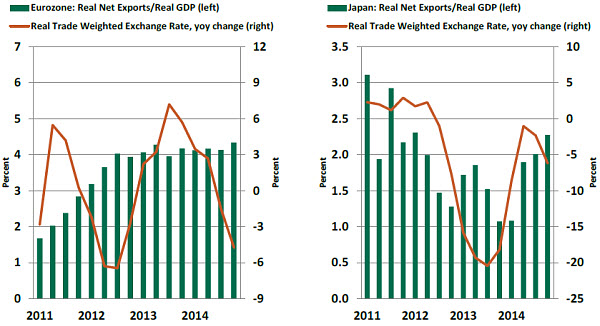

Within the past several years, both the eurozone and Japan have engineered depreciation in their currencies. Neither has yet seen a meaningful improvement in the pace of export growth. Part of the reason is that they have quite a bit of company in the pursuit of this strategy.

We have hesitated to call the current state a currency “war,” preferring to reserve that term for situations that are more bellicose. But the “competition” that seems underway has the potential to leave no one better off and some much worse off.  All of this suggests that the search for stronger demand might better begin at home. Japan’s effort to improve worker wages and spending needs additional emphasis. The eurozone needs to embrace structural reform so that its labor markets can realign and allow unemployment to fall. China’s long-term goal of getting domestic spending to rise is still in the very early stages. These endeavors are central to better and more-balanced global growth.

All of this suggests that the search for stronger demand might better begin at home. Japan’s effort to improve worker wages and spending needs additional emphasis. The eurozone needs to embrace structural reform so that its labor markets can realign and allow unemployment to fall. China’s long-term goal of getting domestic spending to rise is still in the very early stages. These endeavors are central to better and more-balanced global growth.

My son was so excited about his learnings on exchange rates that he is anxious to extend them to other jurisdictions. Unfortunately, he posted some of the photos of our journey online, which his mother subsequently saw. As a result, both of us have been grounded, literally and figuratively.

Official Foreign Exchange Reserves: Details Matter

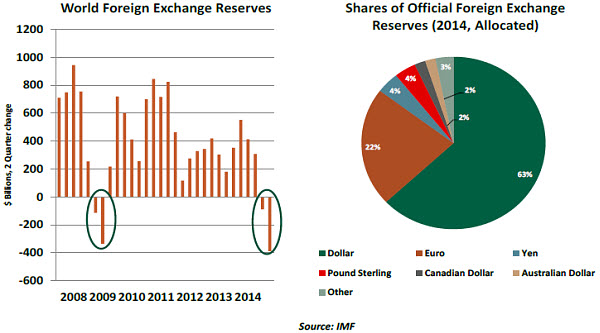

Many of the world’s central banks hold reserves to manage the value of their currencies and to buffer against economic contingencies. The latest International Monetary Fund (IMF) report of official holdings of foreign exchange reserves yields some interesting insights into how these balances are utilized.

The IMF’s latest report indicates that total world foreign exchange reserves fell nearly $390 billion to $11.6 trillion in the second half of 2014, reflecting a decline in foreign exchange reserves of both advanced economies and developing economies.

Declines in holdings of foreign exchange reserves are not frequent, and therefore the recent event drew some attention in the financial press. Digging into the details, one finds that Russia and China were the biggest contributors to the reserve contraction.

Oil prices fell 50% during the six months ended December 2014. Major oil-exporting nations were adversely affected, and they mostly likely reduced their holdings of foreign exchange reserves. As an example, Russia’s official foreign exchange reserves fell $92.6 billion during the second half of 2014. This represents 21% of total reserves, a significant fraction.

China uses its holdings to keep its currency within a designated trading band. The increment it has devoted to sustaining this objective is a modest fraction of its massive foreign reserves. So in all, the decline in global reserves is not necessarily a signal of growing financial distress.

The report also provided a look at the distribution of central bank holdings. The dollar retains its position at the top; the euro’s second place is not a surprise. Although their relative standing has not changed, the composition of foreign exchange reserves shifted a little and warrants careful interpretation.

Dollar holdings in allocated foreign exchange reserves rose to 62.9% from 61.0% in the fourth quarter of 2014. During this period, the share of the euro declined to 22.2% from 24.4%. Further analysis reveals that both advanced economies and emerging and developing economies reduced their share of the euro during this period.  This compositional change raised questions about confidence in the euro. Our research suggests that conclusion is incredibly premature. The dollar’s 13% appreciation vis-à-vis the euro in the second half of 2014 explains a large part of the decline in overall foreign exchange reserves, implying that it is a valuation adjustment and not a behavioral response.

This compositional change raised questions about confidence in the euro. Our research suggests that conclusion is incredibly premature. The dollar’s 13% appreciation vis-à-vis the euro in the second half of 2014 explains a large part of the decline in overall foreign exchange reserves, implying that it is a valuation adjustment and not a behavioral response.

A similar event occurred about six years ago; foreign exchange reserves fell when the dollar rose sharply following the collapse of Lehman Brothers. It is important to note the trend changed soon after.

Observers of central bank investment patterns have also been wondering whether the Chinese currency will ultimately take a greater role in global trade and reserves. At the moment, the yuan accounts for less than 3% of global reserves and less than 20% of international financial transactions. Those levels have grown but remain modest.

The standing of China’s currency remains limited by the fact that it does not float on world markets and because China does not borrow much. There are simply fewer Chinese bonds in circulation, limiting their place in portfolios.

Taken together, all of these factors suggest that the recent change in holdings of foreign exchange reserves is not the beginning of a cyclical or secular transformation.

Who Pays for Low Gas Prices?

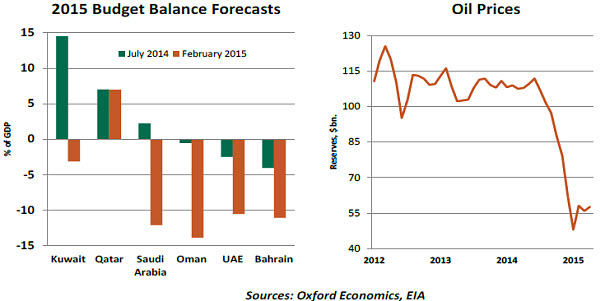

Amid discussion about the energy dividend provided by the dramatic fall in oil prices, it is worth examining just who is paying for this economic windfall. On the other side of the situation, the oil-producing Gulf States now carry budget deficits and have been forced to reduce the largess of years past. And if OPEC keeps oil prices low in the name of reclaiming market share, some of these countries may not be able to endure the prolonged austerity.

OPEC’s strategy appears to be simple: Bring oil prices down and force out higher-cost producers while giving global demand a chance to rebound. The cartel is playing the long game, acknowledging that oil prices could be depressed even into next year, which is necessary to reclaim market position. Oil sectors everywhere are feeling the pinch, but cheap oil is dramatically affecting the Gulf region.

The important distinction between the oil-producing Gulf region and other major oil producers is economic breadth. Oil production and processing can account for 90% of exports in Persian Gulf countries, with hydrocarbon taxes providing the majority of government revenue. When oil prices were above $100 per barrel, large trade surpluses built international reserves, and budget surpluses funded massive sovereign wealth funds. Over the past year, public finances have seen black ink turn red, with stagnating international reserves and free-spending monarchies cutting back on expenditures across the board.

The important distinction between the oil-producing Gulf region and other major oil producers is economic breadth. Oil production and processing can account for 90% of exports in Persian Gulf countries, with hydrocarbon taxes providing the majority of government revenue. When oil prices were above $100 per barrel, large trade surpluses built international reserves, and budget surpluses funded massive sovereign wealth funds. Over the past year, public finances have seen black ink turn red, with stagnating international reserves and free-spending monarchies cutting back on expenditures across the board.

Some countries such as Saudi Arabia and Kuwait can access offshore sovereign wealth funds and easily tap international capital markets, but this is not the case in most other countries. Secondary producers such as Bahrain and Oman have limited resources to utilize and severe deficits to fund. Also, pockets of unrest throughout the region are forcing a sharp increase in defense budgets during a time of austerity, creating more issues for governments already facing a wealth of troubles.

OPEC is very much set on its mission of market reclamation and is expected to keep production levels steady at its June meeting. This means further economic and fiscal hardships for most of the Gulf economies, and talk will turn toward which countries are not well-positioned to endure further weakness in the oil market.

Recommended Content

Editors’ Picks

USD/JPY holds above 155.50 ahead of BoJ policy announcement

USD/JPY is trading tightly above 155.50, off multi-year highs ahead of the BoJ policy announcement. The Yen draws support from higher Japanese bond yields even as the Tokyo CPI inflation cooled more than expected.

AUD/USD extends gains toward 0.6550 after Australian PPI data

AUD/USD is extending gains toward 0.6550 in Asian trading on Friday. The pair capitalizes on an annual increase in Australian PPI data. Meanwhile, a softer US Dollar and improving market mood also underpin the Aussie ahead of the US PCE inflation data.

Gold price keeps its range around $2,330, awaits US PCE data

Gold price is consolidating Thursday's rebound early Friday. Gold price jumped after US GDP figures for the first quarter of 2024 missed estimates, increasing speculation that the Fed could lower borrowing costs. Focus shifts to US PCE inflation on Friday.

Stripe looks to bring back crypto payments as stablecoin market cap hits all-time high

Stripe announced on Thursday that it would add support for USDC stablecoin, as the stablecoin market exploded in March, according to reports by Cryptocompare.

Bank of Japan expected to keep interest rates on hold after landmark hike

The Bank of Japan is set to leave its short-term rate target unchanged in the range between 0% and 0.1% on Friday, following the conclusion of its two-day monetary policy review meeting for April. The BoJ will announce its decision on Friday at around 3:00 GMT.