![]() Carl R. Tannenbaum

Carl R. Tannenbaum

Northern Trust

I’ve been back out on the road over the past two weeks, with meetings in Denver, London and Ireland. The challenging tone of the markets has a made a lot of observers more negative on the outlook. At times like these, economists are blamed for the malaise and expected to rectify things – fast.

I am certainly hoping that the negativity among investors diminishes soon. However, another kind of negativity is likely to stay with us for a long time, and intensify before diminishing. The question is whether this particular brand of negativity will yield positive outcomes.

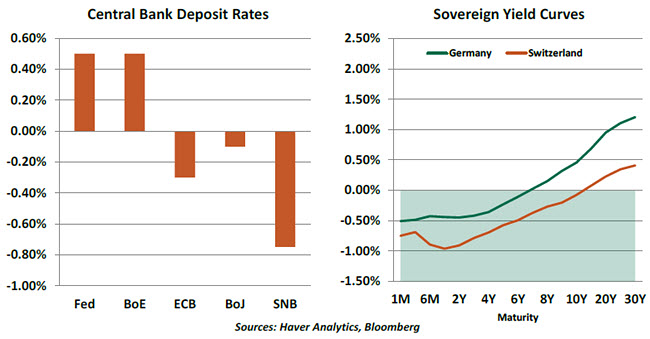

The Bank of Japan (BOJ) surprised markets on Friday by pushing official rates below zero. Many interest rates in Europe have been below zero for quite a while and are poised to fall further. Mario Draghi, president of the European Central Bank (ECB), hinted strongly last week that monetary conditions in the eurozone would be eased further in the months ahead.

The reasons for these actions are clear. Inflation remains stubbornly below the 2% target many central banks set, and unsettling news from Asia could diminish growth prospects. In the wake of spreading investor risk aversion, the euro and the yen have found renewed strength, blunting efforts to promote exports.

Extending or expanding quantitative easing (QE) is an option, but markets have not been responding to that kind of stimulus as powerfully as they used to. In the ECB’s case, the community of assets that it might buy is limited by an aversion to the risk inherent in corporate bonds or equities. So pushing more interest rates more deeply into negative territory seems to be gaining favor.

Once thought impregnable, the zero lower bound on interest rates has proven permeable. Four European central banks have negative benchmark rates, and that has led other interest rates in the same direction. Recent purchasers of Swiss government bonds with maturities all the way out to 10 years are paying for the privilege of making that investment. Ironically, issuing more debt under these conditions is beneficial for fiscal deficits.

In pushing below zero, policymakers hoped to make it expensive for households to be overly frugal, for investors to remain conservative and for banks to lend too conservatively. With inflation falling once again, lowering nominal rates is the only way to keep real interest rates from rising. Rates that are more deeply negative weaken the value of a currency, deterring capital flows seeking safe haven and improving the terms of trade.

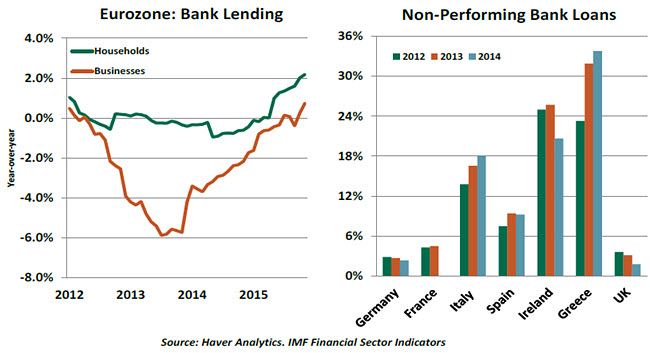

The impact of negative interest rates on bank lending in the eurozone has been modest. Loans increased over the past 12 months, but just barely. Demand for credit is improving, but eurozone households are behind the United States and the United Kingdom in their deleveraging efforts.

The impact of negative interest rates on bank lending in the eurozone has been modest. Loans increased over the past 12 months, but just barely. Demand for credit is improving, but eurozone households are behind the United States and the United Kingdom in their deleveraging efforts.

Europe’s leading financial institutions are healthier than they were after the Global Financial Crisis, but that does not mean they are entirely healthy. Some remain saddled with non-performing loans that require resolution, and others are conserving their capital to meet heightened regulatory standards.

As market interest rates fell, banks reduced the rates on loans and deposits. They reduced deposit prices slowly, and carefully, so as not to be too disruptive to clients who are unaccustomed to paying for the privilege of leaving money in financial institutions.

So far, the spread of negative deposit rates has not prompted banking clients to convert their funds to currency as a store of value. There are several reasons for this. For institutional clients, bank accounts are largely used as a gateway to the payments system. Moving monies electronically carries very low costs and very low risk. Shifting to currency introduces significant frictions to the process that can be very expensive to manage.

For all clients, holding large amounts of cash presents important logistic challenges. Currency is more easily stolen, needs to be recounted when presented for transactions and can degrade over time if not stored properly. In essence, the return on holding currency is slightly negative, with the size of the decrement determined by the cost of securing cash balances.

If interest rates go too deeply into negative territory, it could prompt thinking and investment aimed at making currency viable as a large asset class. Secure warehouses, or even new forms of financial institutions, could be organized to reduce the cost of storage and facilitate the use of cash in large transactions.

Once these structures are in place, they would place a floor under interest rates that would serve as a constraint on central banks. While zero may not be the lower bound on interest rates, that does not mean there is no lower bound at all.

There is another boundary condition that must be respected. As an expanding community of central banks pushes interest rates ever lower, the competition may limit the benefits of the policy. It isn’t possible for everyone to have a weak currency, and a race to the bottom could put even more pressure on emerging markets desperate to sustain global market share.

There is another boundary condition that must be respected. As an expanding community of central banks pushes interest rates ever lower, the competition may limit the benefits of the policy. It isn’t possible for everyone to have a weak currency, and a race to the bottom could put even more pressure on emerging markets desperate to sustain global market share.

Hopefully, modest downward adjustments from the BOJ and the ECB will help growth and inflation get back onto track. But as we’ve written before, a currency war will have no winners. In that case, we’ll be left only with negatives.

Hard Pegs, Soft Pegs and Broken Pegs

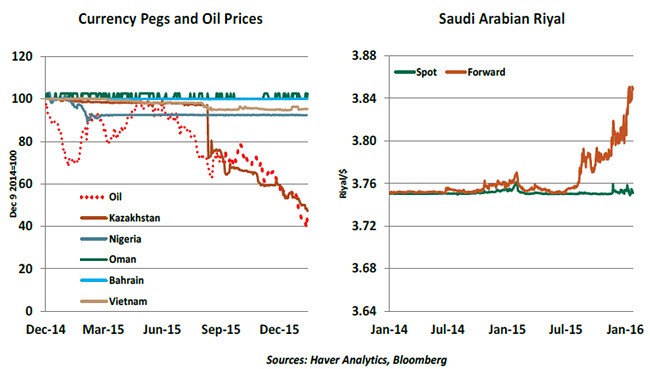

Exchange rates come in different hues, from fixed rates (or pegs) at one end to floating rates at the other end of the spectrum and different types of managed exchange rates that fall in between. The Saudi Arabian riyal is an example of a currency peg, while the U.S. dollar and the pound sterling follow a floating exchange-rate system. Some of the existing exchange-rate arrangements are under pressure as market conditions have become challenging.

The International Monetary Fund notes in its annual report on exchange rates that only “35% of member countries let their currencies float, and only 16% intervened rarely enough for them to classify as freely floating.” The rest of the currencies, from Saudi Arabia’s riyal to the Nigerian naira, are fixed.

In a fixed-rate system, the central bank uses foreign-exchange reserves to maintain the exchange rate within prescribed limits. Stability of an exchange rate reduces uncertainty, promotes trade and foreign investment, and can prevent inflationary circumstances. But at the same time, the central bank loses independence of monetary policy because it is obligated to mirror the strategy underlying the targeted currency.

A country can have a fixed exchange-rate system, free capital flows or an independent central bank, but the three cannot co-exist. It is a “trilemma,” requiring countries to give up one of these three options. As an example, China’s central bank conducts monetary policy and manages the exchange rate to a target but restricts capital flows.

Alternatively, a country can have free capital movements and an independent monetary policy as long it lets markets determine the exchange rate. Most developed economies with a floating exchange-rate system follow this regime. In the United States, capital movements are free and the Federal Reserve conducts monetary policy, but the dollar’s exchange rate is not fixed.

The Swiss National Bank broke its peg with the euro in January 2015 as the Swiss franc became overvalued due to large capital inflows seeking a safe haven during the eurozone crisis. The Mexican devaluation (1994), the Asian crisis (1997), and the Argentinian problem (2001-02) are examples of the inability to have the “impossible trinity” in place at the same time.

The Swiss National Bank broke its peg with the euro in January 2015 as the Swiss franc became overvalued due to large capital inflows seeking a safe haven during the eurozone crisis. The Mexican devaluation (1994), the Asian crisis (1997), and the Argentinian problem (2001-02) are examples of the inability to have the “impossible trinity” in place at the same time.

Oil exporters peg their currency to the dollar because oil is priced in dollars; others fix their exchange rate in terms of a strong currency to earn indirect credibility and contain inflation expectations. Of late, the downward trend of commodity prices and the recent plunge in oil prices have resulted in a few countries abandoning their existing pegged exchange-rate system. These countries stand to lose foreign investment and access to capital markets.

The Kazakh tenge and the Vietnamese dong crumbled under pressure and devalued their currencies last year. The central bank of Nigeria allowed its currency to decline in multiple steps as oil prices fell. Nigeria opted to bridge the gap between export and import revenue rather than let the currency float and find its free-market value.

The Saudi Arabian riyal is the latest currency under pressure. Building a large arsenal of foreign exchange reserves could offer support. Saudi Arabia holds $635 billion in reserves, or the equivalent of 51 months of import cover. The Saudi central bank raised rates after the Fed’s December move, signaling its commitment to the peg, and more hikes are likely this year. The market consensus is that the peg will hold, but the cost of hedging in forward markets has risen sharply.

Currency arrangements are not etched in stone. Policymakers face trade-offs, and each country chooses what it deems appropriate at a given point in time. Changes are bound to occur; hopefully, the consequences of changing are manageable.

Disinflating Expectations

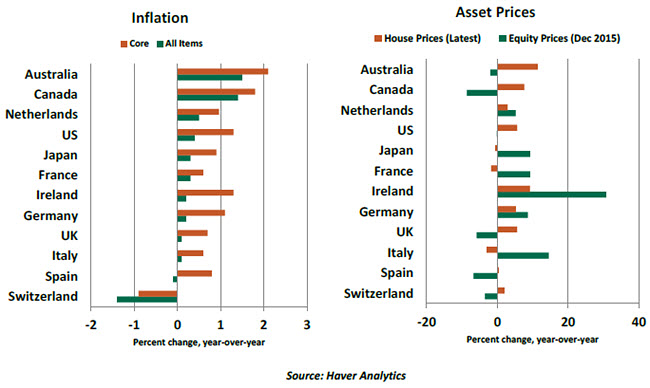

Prices in developed economies are falling or show subdued gains. For the first time since 2009, the threat of deflation is once again a part of policy discussions. The decline in oil prices is exacerbating the problem, but core prices, which exclude food and energy, are also well below the 2.0% level that many central banks target. Canada and Australia are rare exceptions.

The context of these developments is key to understanding if deflation is harmful. On the positive side, productivity and innovation can result in lower prices. Lower prices raise real income and boost consumer spending. But entrenched deflation is problematic: consumer purchases are delayed, business suffers and employment losses occur. Debt service is expensive, as nominal debt-service payments do not change with deflation.

Historically, deflation in the post-war period is rare and brief; Japan’s experience is not the norm. The downward trend of oil prices, unutilized resources and (in some cases) lower food prices are the culprits behind the recent weak inflation picture. Due to base effects, even if oil prices continue to drop in the months ahead, the impact on the year-over-year change in inflation should be much smaller compared with the months when oil prices commenced their downward trend.

Historically, deflation in the post-war period is rare and brief; Japan’s experience is not the norm. The downward trend of oil prices, unutilized resources and (in some cases) lower food prices are the culprits behind the recent weak inflation picture. Due to base effects, even if oil prices continue to drop in the months ahead, the impact on the year-over-year change in inflation should be much smaller compared with the months when oil prices commenced their downward trend.

Excluding the transitory impact of oil prices, a lack of aggregate demand is holding back inflation. The important question is whether inflation will move up after oil prices stabilize. The accommodative monetary policy posture of major central banks supports expectations of higher inflation. Asset prices also play a role in the deflation-aggregate demand story as lower equity and house prices reduce wealth and consumer spending.

House prices versus a year ago dropped in three of the 12 economies shown in the chart above. Equity prices in December fell in six countries from a year ago. The poor start of equity prices in 2016 casts a shadow on the wealth effect of consumer spending. The ingredients for persistent deflation are not in place. But policymakers must be mindful of the vulnerability of soft economic conditions to deflation.

The information herein is based on sources which The Northern Trust Company believes to be reliable, but we cannot warrant its accuracy or completeness. Such information is subject to change and is not intended to influence your investment decisions.

Recommended Content

Editors’ Picks

AUD/USD approaches 0.6900 ahead of Australian inflation

The Aussie is among the best performers against the Greenback this week, trading at fresh 2024 highs, not far from the 0.6900 mark. Australian inflation data taking centre stage in the Asian session.

EUR/USD extend recovery amid persistent USD weakness

The Euro benefited from the broad US Dollar’s weakness on Tuesday, trimming weekly losses and looking to retest the 1.1200 level. Additional gains out of the table amid discouraging European data.

Gold's unstoppable run extends beyond $2,650

Gold price keeps posting record highs on a daily basis, now comfortable above $2,650. Poor United States data fueled speculation the Federal Reserve will trim rates by another 50 bps when it meets in November.

Crypto Today: Bitcoin, Ethereum and XRP consolidate as SUI continues impressive run

Bitcoin traded around $63,600 on Tuesday, as prices appear to be consolidating within the $62,000 and $64,700 key levels. On-chain data shows that the consolidation may be due to profit-taking by holders and mild Bitcoin ETF net inflows of $4.5 million, per Farside Investors data.

RBA widely expected to keep key interest rate unchanged amid persisting price pressures

The Reserve Bank of Australia is likely to continue bucking the trend adopted by major central banks of the dovish policy pivot, opting to maintain the policy for the seventh consecutive meeting on Tuesday.

Moneta Markets review 2024: All you need to know

VERIFIED In this review, the FXStreet team provides an independent and thorough analysis based on direct testing and real experiences with Moneta Markets – an excellent broker for novice to intermediate forex traders who want to broaden their knowledge base.