Editor’s Note: This week’s commentary is a collage of brief observations about an eventful first quarter. We’re publishing on Thursday to get in front of the weekend, which we hope is a pleasant one for those of you observing spring holidays.

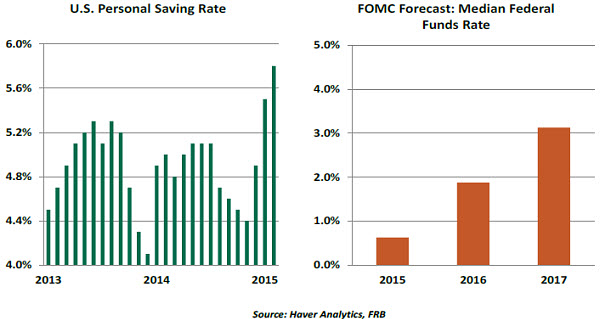

- It was widely expected that U.S. households would spend the dollars saved from lower gasoline prices. But to date, consumers have been thrifty, and the personal saving rate has moved up to 5.8% in February from a low of 4.4% in November.

The key question is whether this is the beginning of a new trend. Many households need to save more to be ready for retirement, but that hasn’t stopped them before from continuing their consumption. Results for the balance of the year will depend critically on whether we’re entering a period of new frugality.

- There are two key takeaways from Federal Reserve Chair Janet Yellen’s recent speech. First, while hinting that a rate hike might be appropriate before year end, she stressed that monetary policy would be tightened gradually. Essentially, policy moves will evolve in a manner consistent with economic progress.

Second, there is no single criterion that must be met to have “reasonable confidence” that inflation will move back to 2.0% over time. In particular, a pickup in either core inflation or wage growth is not a “precondition” for the first rate increase. Improvement toward the Fed’s dual mandate is necessary for the committee to commence tightening monetary policy. - The Greek population favors remaining in the euro by a very wide margin. And outwardly, the new leaders in Greece have said that keeping the common currency is very important to them. But one wonders if the new regime might privately be angling to leave the eurozone and place the blame at someone else’s feet.

At almost every turn, the words and deeds of Greek leadership have seemed designed to provoke the maximum inflammation among the country’s creditors. Their tough reaction may be leading some Greeks to think that the cost of separation would be less than the cost of association. Both sides need to go over their calculations carefully, as do investors trying to position themselves for what might transpire. - The UK Parliament was officially dissolved this week, sparking the start of the election campaign proper. Recent polls suggest neither Labour nor the Conservatives are likely to win a majority, in part due to rising nationalism in Scotland and England. A recent survey of business leaders suggests their main concerns are Labour’s perceived “anti-business” policies and the Conservative’s promise to hold an EU referendum.

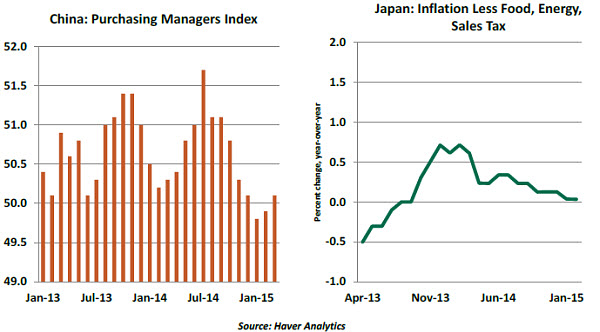

Britain’s traditional three-party system appears to be shaken, and post-election policies will therefore depend on the nature of any agreed coalition. The uncertainty may cloud what has been a terrific economic performance in the United Kingdom over the past several years. - The Chinese government’s growth target of “around 7%” appears increasingly ambitious. The consensus forecast is 6.8% for the year; however, even that figure is at risk. Nearly every economic indicator is pointing to faster-than-expected moderation driven by the slowdown in the property sector. Chinese authorities have been easing some credit conditions in an effort to meet their objectives, but the “new normal” may prove difficult to realize.

- The data are clear: Japan has a disinflation problem. It is also clear that energy prices are not the only culprit. Inflation is dismal even when energy is stripped out and the Bank of Japan’s (BoJ) preferred “core-core” measure is used. Sluggish domestic demand a year after the consumption tax increase continues to weigh on prices.

Concerns about disinflation and a flat BoJ Tankan survey point to another boost to the country’s massive quantitative easing program at some point this year. The BoJ has been cautious about reacting too quickly in the past; hence, the expectation is for any changes to occur during the latter half of the year. - Special thanks to our partners in Texas who hosted a series of conversations this week on energy that will fuel our commentaries over the coming weeks. But an added benefit of the trip was the search for the best barbecue. Here’s hoping that journey never ends. I’ll be eating kale salad for the next month, but the binge was worth it.

- The fate of the Trans-Pacific Partnership is now in the hands of the United States. Once thought to be the main drag on progress, Japan has cleared its major hurdle to agreement – agricultural reform – and is now pushing President Barack Obama to lobby Democrats and secure the Trade Promotion Authority (TPA) he needs to push the deal through Congress. Given the present political tone, however, there is a high likelihood that the multilateral trade agreement will be shelved until the next administration takes office.

- Some observers are still disappointed that more forceful action hasn’t been taken to reduce the “too-big-to-fail” problem in the banking system. But subtly, post-crisis regulation is creating incentives for the biggest institutions to go on a diet.

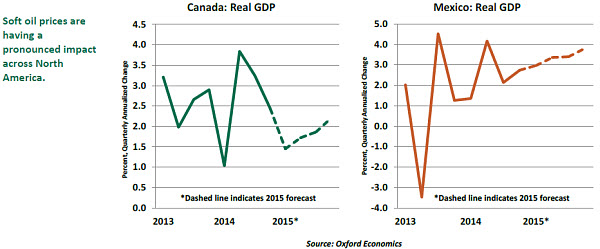

Across developed markets, financial companies are engaging in rationalization exercises, exiting some businesses to focus on others. Higher capital requirements, expanded oversight, and new strictures are all leading bank boards of directors to re-consider their desired mix of activities. The age of global super banks that are all things to all people in all places is likely coming to an end. - Oil-sector weakness is prompting fiscal adjustment in U.S. neighbors and oil exporters Canada and Mexico. In Canada, Alberta province has felt the bite hardest, hammered by a 67% drop in resource revenues. Bank of Canada Governor Stephen Poloz characterized first quarter performance as “atrocious.”

In Mexico, the Ministry of Finance reported oil revenues slumped 46% year-over-year in February, leading to a widening of the budget deficit to 0.8% of gross domestic product (GDP), down from 0.3% of GDP 12 months prior. The government has already announced spending cuts worth 2.6% of total expenditure for 2015, especially for state-owned energy firm PEMEX.

Both economies are hoping that weaker currencies and strengthening demand from the United States, which represents roughly 75% of exports for both countries, will spur a non-oil export recovery in the latter half of 2015. If the expected fillip disappoints, further fiscal adjustment may be necessary. - For those of you who think that economists are among the most confusing people on the planet, a recent series of Dilbert cartoons is right up your alley.

- Talks with Iran have reached a tentative agreement, and now markets are particularly concerned about an overlooked economic aspect of these negotiations – oil prices. Current sanctions place severe restrictions on the oil Iran can put onto the global markets. This is actually supportive of the price of crude, given the current supply glut and OPEC’s resistance to cut production.

The possibility of sanctions relief would send crude prices yet lower in anticipation of more supply in the market. However, a failure to finalize this agreement could trigger yet further sanctions, pressing oil prices noticeably higher. As the situation develops, the oil markets will be very sensitive to any changes in expectations. - With Nigeria’s socioeconomic situation strained to the brink, concerns had risen that the March 28 presidential election could be the final straw that sets off broad-scale social unrest. The contest between President Goodluck Jonathan and Muhammadu Buhari was fraught with tensions, and Nigeria’s tarnished experience with democracy suggested anything less than a conclusive victory for one candidate would create a problem. The country’s substantial oil production was thought to be at some risk.

On March 31, Buhari was announced the winner and President Jonathan conceded defeat, bringing the presidential elections to a surprisingly peaceful end and sweeping away a significant amount of uncertainty from Nigeria’s near-term outlook. However, President-elect Buhari now has to face up to a weak fiscal situation, a poor economic outlook and the continuing problem with Boko Haram rebels. Stabilizing Nigeria’s socioeconomic problems will be very difficult, but at least Buhari will be able to enjoy a brief period of political stability. - It’s hard to be disappointed by the U.S. Congress, given that expectations are so low. But the polarization between parties has now been complemented by polarization within parties as the 2016 presidential campaign starts to simmer. The petty battles we’ve seen over little issues so far this year do not bode well for successful consideration of some of the bigger economic issues facing the nation.

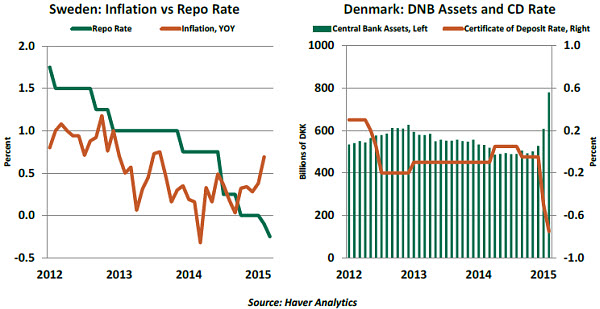

Retirement, health care, immigration, energy, trade and the national debt are all areas that deserve reasoned attention from our elected officials. Delay might seem like a low-cost strategy, but waiting can be very expensive in the long term. The country and the global investment community may not hide their frustration forever. - The Swedish and Danish central banks have both taken their key interest rates to historic lows this year, based on concerns about persistently low inflation and to maintain a long-standing currency peg, respectively. The question for the remainder of 2015 is how low can they go? Both banks are similar in their apparent unwavering “whatever-it-takes” attitude to achieve their goals.

The Riksbank has cut rates twice since January despite inflation ticking up slightly, the reasoning being to “support” the upturn. The Danish Nationalbank’s sole mandate is to maintain the peg, and it has assured markets it will do so at all costs, accumulating massive currency reserves in the process. Given the resoluteness of both central banks, further cuts are possible if events don’t go their way.

- The Aussies may have triumphed on the cricket field, but the Kiwis may have the last laugh in the exciting world of economic indicators. New Zealand is expected to register stronger growth and lower unemployment in 2015 than its bigger neighbor. For now, though, we doubt anyone in Australia is bothered about that.

Recommended Content

Editors’ Picks

EUR/USD holds below 1.0750 ahead of key US data

EUR/USD trades in a tight range below 1.0750 in the European session on Friday. The US Dollar struggles to gather strength ahead of key PCE Price Index data, the Fed's preferred gauge of inflation, and helps the pair hold its ground.

GBP/USD consolidates above 1.2500, eyes on US PCE data

GBP/USD fluctuates at around 1.2500 in the European session on Friday following the three-day rebound. The PCE inflation data for March will be watched closely by market participants later in the day.

Gold clings to modest daily gains at around $2,350

Gold stays in positive territory at around $2,350 after closing in positive territory on Thursday. The benchmark 10-year US Treasury bond yield edges lower ahead of US PCE Price Index data, allowing XAU/USD to stretch higher.

Bitcoin Weekly Forecast: BTC’s next breakout could propel it to $80,000 Premium

Bitcoin’s recent price consolidation could be nearing its end as technical indicators and on-chain metrics suggest a potential upward breakout. However, this move would not be straightforward and could punish impatient investors.

US core PCE inflation set to signal firm price pressures as markets delay Federal Reserve rate cut bets

The core PCE Price Index, which excludes volatile food and energy prices, is seen as the more influential measure of inflation in terms of Fed positioning. The index is forecast to rise 0.3% on a monthly basis in March, matching February’s increase.