Asia closers reducing FX flows

Market Brief

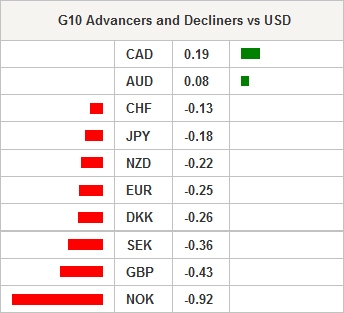

FX markets were subdued in the Asian session. USD was marginal stronger against G10 and EM currencies. The primary trigger was US presidential-hopeful Donald Trump being able to drag Hillary Clinton down into the mud to salvage his campaign (reversing earlier risk rally on decreasing Trump presidential chances due to lewd video).The Hong Kong stock exchanges, Tokyo and Taipei were closed Monday because of a holiday, decreasing trading flow. Currency markets continue to show a heightened sensitivity to US elections. The Shanghai composite rose 1.19% while the rest of Asia was mixed. Despite Deutsche's top people in Washington DC to reach a deal with the DoJ there is yet to be any sentiment. The uncertainty around the final penalty will continue to weigh on equity market sentiment. US crude prices were unable to hold the $50 handle as the US rig count continues to increase and the producer meeting in Istanbul is not expected to result in any production reduction agreement. WTI fell 1.3% to 49.70 brl. The weak crude price sent USDNOK to 8.12 from 8.02. Elsewhere, the PBOC set USDCNY mid-point at 6.7008 against a prior fix of 6.6745 - the lowest level since Sept 2010

In the US, weaker then expected US job data released on Friday was not soft enough to completely remove expectations for a December Fed rate hike. The payroll report indicated that NFP climbed by 156k in September from an increase of 176 in August. The US unemployment rate rose to 5% from 4.9%. Despite the Fed fund probability indicating a 60% probability of a 25bp hike we anticipate that economic data will continue to highlight decelerations, prompting the Fed to delay hikes in 2017. While volatility in FX is rising we expect that any USD rally will be unsustainable, especially against high yielding EM currencies. Polling has Donald Trump at a 20% probability of winning the US elections. As this number shifts a long basket of JPY, USD and short CAD, MXN and CNY will continue to gyrate.

Selling pressure remains steady on the GBP and economic data indicates that the British economy is slowing. In Ireland, construction growth accelerated as new orders rose at the fastest pace in six months. The Ulster Bank Construction PMI, increased to 58.7 in September from 58.4 prior read. While the rhetoric and negative GBP is not completely unfounded, we do anticipate a recovery as investors realize how uncertain the final term of Brexit really can be.

| Global Indexes | Current Level | % Change |

|---|---|---|

| Nikkei 225 Index | 16860.09 | -0.23 |

| Hang Seng Index | 23851.82 | -0.42 |

| Shanghai Index | 3048.14 | 1.44 |

| FTSE 100 Index | 7058.03 | 0.19 |

| DAX Index | 10493.67 | 0.02 |

| SMI Index | 8124.59 | -0.56 |

| S&P future | 2152.8 | 0.29 |

| Global Indexes | Current Level | % Change |

|---|---|---|

| Gold | 1262.36 | 0.43 |

| Silver | 17.67 | 0.7 |

| VIX | 13.48 | 4.98 |

| Crude wti | 49.49 | -0.64 |

| USD Index | 96.71 | 0.08 |

| Today's Calendar | Estimates | Previous | Country/GMT |

|---|---|---|---|

| NO Sep CPI MoM | 0,60% | -0,50% | NOK/06:00 |

| NO Sep CPI YoY | 4,00% | 4,00% | NOK/06:00 |

| NO Sep CPI Underlying MoM | 0,70% | -0,50% | NOK/06:00 |

| NO Sep CPI Underlying YoY | 3,20% | 3,30% | NOK/06:00 |

| NO Sep PPI including Oil MoM | - | -1,80% | NOK/06:00 |

| NO Sep PPI including Oil YoY | - | -4,70% | NOK/06:00 |

| SW SEB Swedish Housing Price Indicator | - | - | SEK/06:30 |

| DE Aug Current Account (Seasonally Adjusted) | - | 1,21E+10 | DKK/07:00 |

| DE Aug Trade Balance ex Ships | 7,50E+09 | 8,20E+09 | DKK/07:00 |

| DE Sep CPI MoM | 0,30% | -0,30% | DKK/07:00 |

| DE Sep CPI YoY | 0,30% | 0,20% | DKK/07:00 |

| DE Sep CPI EU Harmonized MoM | 0,20% | -0,40% | DKK/07:00 |

| DE Sep CPI EU Harmonized YoY | 0,10% | 0,00% | DKK/07:00 |

| SW Aug Household Consumption (MoM) | - | -0,10% | SEK/07:30 |

| SW Aug Household Consumption (YoY) | - | 2,30% | SEK/07:30 |

| SZ 07.oct. Total Sight Deposits | - | 5,17E+11 | CHF/08:00 |

| SZ 07.oct. Domestic Sight Deposits | - | 4,53E+11 | CHF/08:00 |

| EC Oct Sentix Investor Confidence | 6 | 5,6 | EUR/08:30 |

| NZ Sep Card Spending Retail MoM | 0,80% | -0,40% | NZD/21:45 |

| NZ Sep Card Spending Total MoM | - | -0,80% | NZD/21:45 |

Currency Tech

EURUSD

R 2: 1.1616

R 1: 1.1428

CURRENT: 1.1113

S 1: 1.1046

S 2: 1.0913

GBPUSD

R 2: 1.3121

R 1: 1.2857

CURRENT: 1.2448

S 1: 1.2352

S 2: 1.1841

USDJPY

R 2: 107.90

R 1: 104.32

CURRENT: 103.91

S 1: 99.02

S 2: 96.57

USDCHF

R 2: 0.9956

R 1: 0.9885

CURRENT: 0.9825

S 1: 0.9522

S 2: 0.9444

- S: Strong, M: Minor, T: Trendline, K: Keylevel, P: Pivot

Author

Peter A Rosenstreich

Swissquote Bank Ltd

Peter Rosenstreich is Swissquote Bank’s Head of Market Strategy and manages the global strategy desk; he has held various positions in several banking institutions in the United States, Europe & Asia.