![]() Arnaud Masset

Arnaud Masset

Swissquote Bank Ltd

Market Brief

The US dollar continued to trade with a positive bias on Monday morning and consolidated last week’s gains as traders brace for this week FOMC and BoJ meetings. The market is not expecting the Federal Reserve to tighten its monetary policy on Wednesday but is definitely awaiting an update on its thinking. On the other hand, market participants anticipate the BoJ will ease further its monetary policy by cutting its policy rate from -0.10% to -0.15%, while the government may also do its bit by delivering fiscal stimulus.

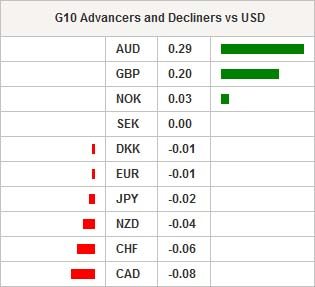

In spite of those expectations, the Japanese yen rallied in Tokyo as traders wondered whether the BoJ would finally deliver the stimulus. USD/JPY erased early session’s gains and returned at around 106 on the European opening. The market will likely wait for the BoJ’s announcement on Friday before selling massively the yen and pushing USD/JPY above the 108 resistance level. Meanwhile, the currency pair should trade sideways between 105.50 and 107.50.

Precious metals had a tough start into the week against the background of a strengthening US dollar. The yellow metal slid 0.38% on Monday and returned towards the $1,300 threshold. Silver was also facing significant selling pressures as it slip 0.70%, down to $19.49 an ounce. On the upside, the $21 resistance still holds, while on the downside a support can be found at around $19 (previous lows).

NZD/USD swung widely on Monday as the currency pair tested the strong 0.70 support level (50dma and psychological level). The Kiwi dropped first to 0.6957 on falling commodity prices before bouncing back at around $0.70. Overall, the bias remains on the downside as the RBNZ is expected to deliver a rate cut at its August meeting.

Asian equity returns were mixed this morning as most equity indices had already returned near 2016 highs. The Nikkei consolidated at around 16,620 points, edging down 0.04% on the session, while the broader Topix index slid 0.19%. In mainland China, the Shanghai Composite fell 0.20%, the Shenzhen one was down 0.37%. Offshore, Honk Kong’s Hang Seng fell 0.24%. Further south, the NZX/S&P was up 1.26%, while Australian equities were up 0.64%. European futures are moving back-and-forth across the neutral threshold and are currently blinking green.

Today traders will be watching IFO business climate from Germany; capacity utilization form Turkey; Dallas Fed manufacturing activity index.

| Global Indexes | Current Level | % Change |

|---|---|---|

| Nikkei 225 Index | 16620.29 | -0.04 |

| Hang Seng Index | 21943.09 | -0.1 |

| Shanghai Index | 3013.381 | 0.02 |

| FTSE futures | 6681 | 0.1 |

| DAX futures | 10156 | 0.19 |

| SMI Futures | 8176 | -0.01 |

| S&P future | 2165.5 | -0.09 |

| Global Indexes | Current Level | % Change |

|---|---|---|

| Gold | 1317.32 | -0.39 |

| Silver | 19.49 | -0.73 |

| VIX | 12.02 | -5.65 |

| Crude wti | 44.12 | -0.16 |

| USD Index | 97.42 | -0.05 |

| Today's Calendar | Estimates | Previous | Country/GMT |

|---|---|---|---|

| NZ RBNZ Governor Wheeler Speaks in Auckland (Not Public) | - | - | NZD/07:30 |

| GE Jul IFO Business Climate | 107,5 | 108,7 | EUR/08:00 |

| GE Jul IFO Current Assessment | 114 | 114,5 | EUR/08:00 |

| GE Jul IFO Expectations | 101,6 | 103,1 | EUR/08:00 |

| SZ Jul 22 Total Sight Deposits | - | 511.0b | CHF/08:00 |

| SZ Jul 22 Domestic Sight Deposits | - | 434.7b | CHF/08:00 |

| UK Jul CBI Trends Total Orders | -6 | -2 | GBP/10:00 |

| UK Jul CBI Trends Selling Prices | - | 1 | GBP/10:00 |

| UK Jul CBI Business Optimism | -15 | -5 | GBP/10:00 |

| BZ Jul 22 FGV CPI IPC-S | 0,35% | 0,41% | BRL/11:00 |

| BZ Jul FGV Consumer Confidence | - | 71,3 | BRL/11:00 |

| BZ Central Bank Weekly Economists Survey (Table) | - | - | BRL/11:25 |

| TU Jul Real Sector Confidence SA | - | 104,3 | TRY/11:30 |

| TU Jul Real Sector Confidence NSA | - | 106,8 | TRY/11:30 |

| TU Jul Capacity Utilization | - | 76,10% | TRY/11:30 |

| BZ Jun Federal Debt Total | - | 2879b | BRL/12:30 |

| CA Jul 22 Bloomberg Nanos Confidence | - | 57,3 | CAD/14:00 |

| US Jul Dallas Fed Manf. Activity | -10 | -18,3 | USD/14:30 |

Currency Tech

EURUSD

R 2: 1.1428

R 1: 1.1186

CURRENT: 1.0966

S 1: 1.0913

S 2: 1.0822

GBPUSD

R 2: 1.3981

R 1: 1.3534

CURRENT: 1.3136

S 1: 1.2851

S 2: 1.2798

USDJPY

R 2: 109.14

R 1: 107.90

CURRENT: 106.17

S 1: 103.91

S 2: 99.02

USDCHF

R 2: 1.0328

R 1: 0.9956

CURRENT: 0.9886

S 1: 0.9764

S 2: 0.9685

- S: Strong, M: Minor, T: Trendline, K: Keylevel, P: Pivot

This report has been prepared by Swissquote Bank Ltd and is solely been published for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any currency or any other financial instrument. Views expressed in this report may be subject to change without prior notice and may differ or be contrary to opinions expressed by Swissquote Bank Ltd personnel at any given time. Swissquote Bank Ltd is under no obligation to update or keep current the information herein, the report should not be regarded by recipients as a substitute for the exercise of their own judgment.

Recommended Content

Editors’ Picks

EUR/USD edges lower toward 1.0700 post-US PCE

EUR/USD stays under modest bearish pressure but manages to hold above 1.0700 in the American session on Friday. The US Dollar (USD) gathers strength against its rivals after the stronger-than-forecast PCE inflation data, not allowing the pair to gain traction.

GBP/USD retreats to 1.2500 on renewed USD strength

GBP/USD lost its traction and turned negative on the day near 1.2500. Following the stronger-than-expected PCE inflation readings from the US, the USD stays resilient and makes it difficult for the pair to gather recovery momentum.

Gold struggles to hold above $2,350 following US inflation

Gold turned south and declined toward $2,340, erasing a large portion of its daily gains, as the USD benefited from PCE inflation data. The benchmark 10-year US yield, however, stays in negative territory and helps XAU/USD limit its losses.

Bitcoin Weekly Forecast: BTC’s next breakout could propel it to $80,000 Premium

Bitcoin’s recent price consolidation could be nearing its end as technical indicators and on-chain metrics suggest a potential upward breakout. However, this move would not be straightforward and could punish impatient investors.

Week ahead – Hawkish risk as Fed and NFP on tap, Eurozone data eyed too

Fed meets on Wednesday as US inflation stays elevated. Will Friday’s jobs report bring relief or more angst for the markets? Eurozone flash GDP and CPI numbers in focus for the Euro.