- The Federal Reserve’s updated guidance takes a page from its past

- Wage trends will guide the timing of tightening

- Chinese banking reformers should be careful what they wish for

A couple of Sundays ago, I told my daughter that dinner would be ready at six. When the chicken took a little longer in the oven, I told her that I had meant some time around six. She was decidedly unsatisfied with this change in guidance and shot me that “you- are-lame” glare that I see several times daily. She promptly ate five slices of garlic bread and retired to her room, not to been seen again until dessert.

The moral of the story is that sometimes it’s best to be vague. You can’t cook a chicken based solely on time, given uncertainty about the physiology of the bird and the accuracy of the oven thermometer. You simply have to know what to look for in the finished product.

This seemed to be the spirit of the Federal Reserve’s updated approach to communication. The specific employment targets that had been part of its statements since December 2012 were dropped in favor of a return to the more subjective language used in the past. Time will tell whether investors find this new diet sufficiently nourishing.

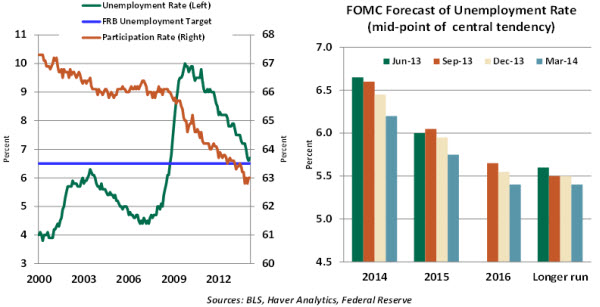

It was widely expected that the Fed would change the formulation of its statement. Unemployment has fallen very close to the 6.5% mark that was identified as a trigger for consideration of interest rate hikes. But we have neared that threshold in a somewhat unsatisfactory manner, with declines in labor force participation and an increased share of part-time hiring accounting for a good deal of the recent improvement in joblessness.

The collated forecasts of Federal Open Market Committee (FOMC) members suggest we have some distance to go before reaching full employment. With unsettled conditions in emerging markets creating downside risks to growth, our sense is that interest rate increases from the Fed remain a long time off.

So the FOMC had essentially two alternatives for updating communication. The first was simply to lower the targeted unemployment rate. But the committee likely struggled to establish a level that conclusively represented strength in labor markets and that would not need to be lowered again at a future date. A serially adjusted promise is not really a promise at all. And so it opted for something much more qualitative.

The Fed’s course for the balance of this year seems locked in. Regular reductions of $10 billion in asset purchases can be expected to follow each of its upcoming meetings, absent a significant change in the outlook. At that rate, additions to the Fed’s balance sheet will end in the fall. Of more interest, then, is what might happen next.  Observers were hoping for more clues on this front during Janet Yellen’s press conference. While she gave a very solid performance, she did momentarily stray from the state-dependent language that has become the Fed’s stock-in-trade. Asked what the lag might be between tapering and tightening, she responded: “This is the kind of term it’s hard to define, but, you know, it probably means something on the order of around six months or that type of thing. But, you know, it depends.”

Observers were hoping for more clues on this front during Janet Yellen’s press conference. While she gave a very solid performance, she did momentarily stray from the state-dependent language that has become the Fed’s stock-in-trade. Asked what the lag might be between tapering and tightening, she responded: “This is the kind of term it’s hard to define, but, you know, it probably means something on the order of around six months or that type of thing. But, you know, it depends.”

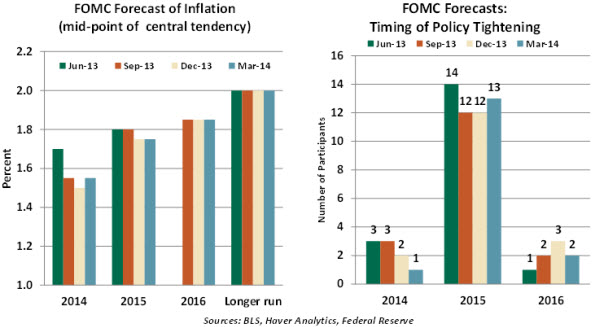

This appeared to be a casual statement that was thoroughly hedged. But some in the markets took the remark to be the product of cold calculus and began fretting about an interest-rate increase next spring. But given the FOMC’s expectations of inflation, one might expect the group’s expectations for a 2015 rate hike would concentrate on the latter part of the year.

We’d suspect that speeches from Fed officials in the coming weeks will reinforce the message that rates will remain low for a very long time.

The press failed to ask a couple of questions that might have evoked interesting answers. First, speculation about the tightening phase of Fed strategy has focused on the traditional lever of the federal funds rate. But as we’ve written, the rates on deposits and repurchase agreements where banks place money with the Fed may be a more meaningful indication of restraint. It will be interesting to hear more from the Fed about how it intends to mix the various ingredients.

Second, aside from a question about Ukraine, no one asked whether the FOMC had weighed effects on emerging markets when considering its long-range strategy. News from overseas has not been encouraging so far this year and could have the potential to dampen the outlook and defer the draining of reserves.

The new edition of forward guidance is a bit of a throwback for the Fed. Dropping numeric targets provides the FOMC much more discretion. But increased mystery over the future course of policy may diminish the Fed’s ability to shape market expectations. Acceptance of a vague style depends on its leadership’s credibility with markets. Greenspan had it; Carney has it now; and Janet Yellen hopes to earn it.

Chastened by my chicken fiasco, I am going to switch to slow-cooked food this Sunday. Started early in the afternoon, a soup or stew can be served at almost any time. Hopefully, this will restore my credibility among those who dine at my table.

Quiescent Wage Trends Give Fed Wiggle Room

The Fed’s latest policy statement included a very important addition to forward guidance. Interest rates are likely to stay below their long-run level – which the Fed projects as 4% – even after employment and inflation return to points consistent with the Fed’s mandate. The rationale for this is tied to underlying labor market conditions.

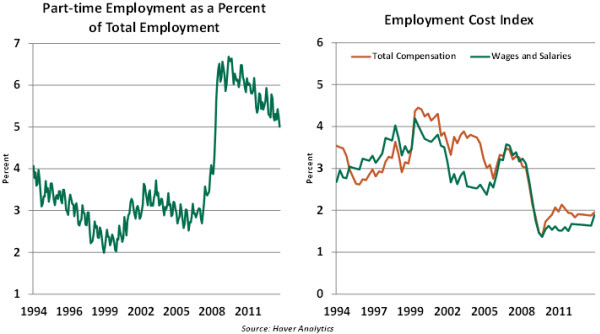

The Fed’s Summary of Economic Projections indicates that the long-run level of unemployment is around 5.4%, which is roughly 1.3% below the current unemployment rate. Under normal circumstances, the long-run unemployment level would be associated with minimum slack in the economy and a whiff of inflation.  The new forward guidance implies that the Fed does not expect this scenario to materialize, despite the likelihood of a reduction in the jobless rate. There are good reasons for this expectation. Although the unemployment rate dropped a little more than a percentage point in the past year to 6.7%, there are 7.3 million people in the United States today who want full-time jobs but are working part-time. They make up 5.0% of total employment.

The new forward guidance implies that the Fed does not expect this scenario to materialize, despite the likelihood of a reduction in the jobless rate. There are good reasons for this expectation. Although the unemployment rate dropped a little more than a percentage point in the past year to 6.7%, there are 7.3 million people in the United States today who want full-time jobs but are working part-time. They make up 5.0% of total employment.

Of the 7.3 million part-time workers, 60% are working part-time because of weak business conditions. Also, part-time employment of the prime-age group (25-54 years) shot up sharply during the Great Recession, and it remains at an elevated level (up about 40% from December 2007 when the recession commenced). Overall, part-time employment numbers send a strong message of significant slack in the labor market.

The picture of labor market slack is more complete when we examine it along with compensation trends. Overall compensation, as measured by the Employment Cost Index, moved up only 1.9% in 2013 – a small increase after holding between 1.5% and 1.6% in the prior three years. Considering that inflation has been running at a little more than 1%, this represents a very modest real increase.

The recent trend in employee compensation is weak and noticeably below the pace seen prior to the recession. If labor markets were tightening, employment compensation would accelerate a bit more. The pool of part-time employees, added to those who have temporarily left the labor force, represents a reservoir of resources that should continue to limit inflation and justify monetary accommodation.

Therefore, it is understandable that the Fed crafted a form of forward guidance that addresses soft spots in the labor market. The Fed has room to complete its asset purchase program and then watch and wait until labor market conditions improve.

Disintermediation and Deregulation

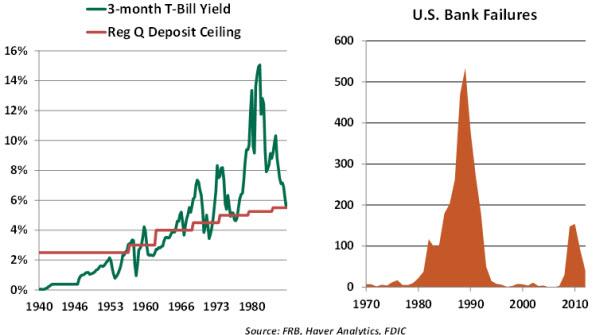

It may seem difficult to comprehend today, but federal law used to limit the rates that American banks could pay their depositors. These caps were repealed a generation ago, as the industry attempted to keep pace with investment products offered by non-banks.  For nearly the same reasons, China recently announced it would gradually remove the interest rate ceilings imposed on its banks. But as the transition approaches, Chinese banking authorities would do well to study the American experience.

For nearly the same reasons, China recently announced it would gradually remove the interest rate ceilings imposed on its banks. But as the transition approaches, Chinese banking authorities would do well to study the American experience.

Regulation Q was enacted during the Depression and included ceilings on bank deposit rates. The intent was to constrain both costs and competition in banking, as part of a broad effort to rehabilitate the industry. Between 1930 and 1933, 10,000 U.S. banks closed their doors.

What followed was a period that some call the “Great Moderation.” The American economy grew, and so did bank profitability. An average of only five banks failed yearly between 1940 and 1980.

But after the oil shocks of the 1970s, market interest rates soared. Depositors flocked to the better returns available in non-bank vehicles like money market mutual funds. Banks clamored for the opportunity to compete and were granted it under the Depository Institutions Deregulation and Monetary Control Act of 1980.

Almost immediately, banks had cause to regret what they had wished for. They did a better job of keeping their deposits, but the cost of doing so skyrocketed. Many firms held long-term home mortgages, whose yields remained low while funding costs increased. Others made riskier loans with higher expected returns to sustain profitability but ended up suffering substantial losses when borrowers defaulted.

More than 1,000 U.S. banks failed during the decade of the 1980s, and the nation’s savings-and-loan sector required a $160 billion bailout from American taxpayers. The banking industry ultimately regained its footing and thrived, but it also became far more concentrated and complicated. These two qualities were not helpful in 2008.

Chinese authorities are great students of history. Hopefully, they can learn from our painful lesson in deposit deregulation.

Recommended Content

Editors’ Picks

EUR/USD edges lower toward 1.0700 post-US PCE

EUR/USD stays under modest bearish pressure but manages to hold above 1.0700 in the American session on Friday. The US Dollar (USD) gathers strength against its rivals after the stronger-than-forecast PCE inflation data, not allowing the pair to gain traction.

GBP/USD retreats to 1.2500 on renewed USD strength

GBP/USD lost its traction and turned negative on the day near 1.2500. Following the stronger-than-expected PCE inflation readings from the US, the USD stays resilient and makes it difficult for the pair to gather recovery momentum.

Gold struggles to hold above $2,350 following US inflation

Gold turned south and declined toward $2,340, erasing a large portion of its daily gains, as the USD benefited from PCE inflation data. The benchmark 10-year US yield, however, stays in negative territory and helps XAU/USD limit its losses.

Bitcoin Weekly Forecast: BTC’s next breakout could propel it to $80,000 Premium

Bitcoin’s recent price consolidation could be nearing its end as technical indicators and on-chain metrics suggest a potential upward breakout. However, this move would not be straightforward and could punish impatient investors.

Week ahead – Hawkish risk as Fed and NFP on tap, Eurozone data eyed too

Fed meets on Wednesday as US inflation stays elevated. Will Friday’s jobs report bring relief or more angst for the markets? Eurozone flash GDP and CPI numbers in focus for the Euro.