USD/JPY Forecast: Can the optimism continue? Powell's power play awaited

|- USD/JPY advanced as China and the US got closer.

- The Fed decision is left, right, and center in the pre-Christmas week.

- The technical picture is mixed for the pair. The FX Poll shows a bullish bias for the short term and a bearish one afterward.

This was the week: Trade improves, fading European risks, OK data

USD/JPY remained a barometer of the global mood in markets, and the atmosphere improved. The world's largest economies got closer as China began buying US soybeans. Despite the small economic impact, farmers are critical to Trump's base.

Moreover, Beijing is reportedly ready to change or postpone its China 2025 program, a thorn for American policymakers. The long-term plan includes Artificial Intelligence and robotics, and Washington is concerned about a loss of its technological hegemony.

Huawei CFO and the only child of the Chinese giant's founder Meng Wanzhou was released on bail in Canada, another positive step. She was arrested upon a request by a US court. However, two former Canadian diplomats were detained in China, serving as a warning sign. All in all, markets advanced on the positive signs, and this weighed on the safe-haven yen.

Late in the week, disappointing economic data from China dampened the mood once again. The slowdown in industrial output and retail sales weighed on stocks but had a limited effect on the yen.

In the UK, the Brexit drama continued with PM May pulling the vote on the deal and winning a leadership challenge. While doubts about the next steps persist, dollar/yen is not moving much on these developments, nor on the Italian crisis, which is seeing progress.

US data was upbeat. Retail sales were robust with the Control Group leaping by 0.9% on top of an upward revision. The good news lift expectations for Q4 GDP. November's inflation figures met expectations. The return of Core CPI to 2.2% YoY is somewhat encouraging for the Fed.

US events: Fed focus

The Fed is set to raise rates for the fourth time this year. Most economic indicators such as growth and employment look good, and inflation is OK. Most importantly, FOMC officials guided markets about the rate hike, and they will not surprise markets.

The more significant question is: what will the Fed do in 2019? The most recent projections for interest rates are from September. The Fed then had a median estimate of three increases next year. The signs of a slowdown and several dovish comments by officials led markets to lower expectations and bond markets are unsure of a single rise next year.

The fresh dot-plot for December will determine the initial market reaction. A downgrade to two rate hikes seems reasonable but markets are more dovish, so the greenback could rally, A cut to only one would send the greenback down. Insisting on three could send the greenback shooting higher.

The focus will then quickly shift to the statement. Back in November, the Fed made a single change, downgrading the assessment of business investment to "moderating." Any comments on inflation and employment will be of interest. The previous decision was unanimous, so any dissent could also gain attention, pushing the USD lower.

Tension will rise once again when Chair Jerome Powell begins his press conference half an hour after the release. Powell tends to be straightforward on monetary policy and could trigger additional market volatility. However, he will likely dodge any questions about trade or political intervention. Trump said that it "would be foolish" of the Fed to raise rates and also said he is not pleased "one bit" from Powell.

Trump's criticism may embolden the Fed to stick to its independence and even adopt a more hawkish tone than it had originally planned.

Other US events

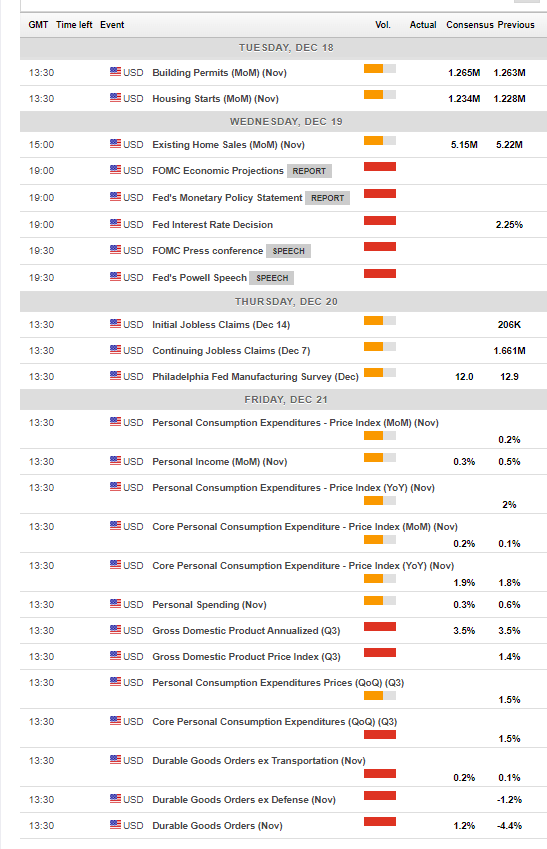

Housing figures kick off the week. Building Permits and Housing Starts are both expected more up marginally in the report for November due on Tuesday. More importantly, Existing Home Sales on Wednesday are of interest after a series of disappointments in this sector.

A big bulk of data is due on Friday. The final version of US Q3 GDP growth will likely confirm the annualized growth rate of 3.5% reported previously. In this case, any change in the composition of growth will be eyed. Inventories contributed a hefty 2.27% to the 3.5% growth rate. The massive contribution of replenishing inventories could backfire if they are depleted, as often happens, in the following quarter. Personal consumption and exports are also of high interest.

Durable Goods Orders for November could have a greater say in market movements as the data is fresher and contributes to Q4 GDP. Headline orders fell sharply in October and probably bounced back. An increase is also expected in the core figure, which tends to carry more weight.

Last but not least, the Core PCE is the Fed's preferred measure of inflation. After Core CPI increased from 2.1% to 2.2% in November, Core PCE is projected to followed suit and tick up to 1.9%. However, the impact may be limited as it comes after the Fed decision and also amid other economic releases.

Here are the top US events as they appear on the forex calendar:

{kind=link}

Japan: A barometer for the mood and also a rate decision

The Japanese yen remains, as usual, the ultimate safe-haven currency. Its correlation with global stock markets and especially the S&P remains prevalent.

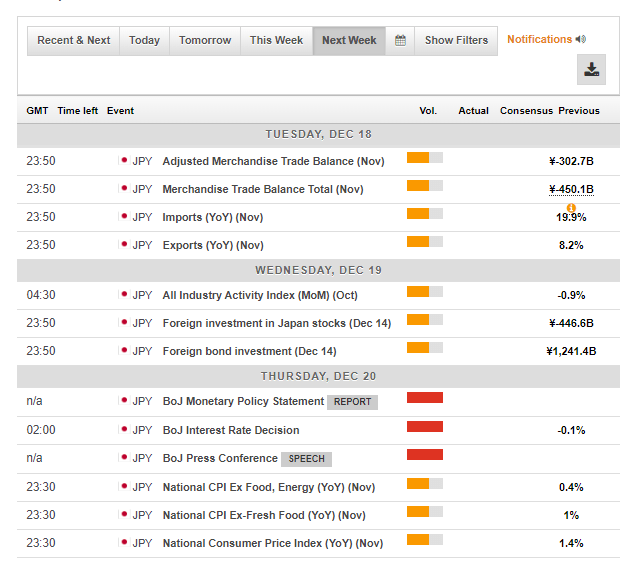

The pre-holiday week includes several economic releases and one event of more significance: the rate decision by the Bank of Japan. The Tokyo-based institution held to its title as the most dovish central bank in the developed world, sticking to negative interest rates and depressing bond yields. Governor Haruhiko Kuroda and his colleagues are unlikely to stay away from this policy in the last meeting of the year.

A surprising expansion of the band around the 10-year yield target may push the currency higher, but the BOJ may prefer to wait for more data early next year. Core inflation remains subdued in the Land of the Rising Sun.

National inflation figures for November are due after the decision. However, we already know that prices are going nowhere fast according to the early release for the capital region.

All in all, the Japanese yen will likely serve as a gauge of fear, maintaining its inverse correlation with equities.

Here are the events lined up in Japan:

{kind=link}

USD/JPY Technical Analysis

The big picture for dollar/yen is that it is leaning lower, setting lower highs and lower lows, albeit in a broad range. The thick black lines on the chart illustrate the broad trend. On the other hand, the pair trades above the 50-day and 200-day Simple Moving Averages. Momentum turned positive but it remains weak. The Relative Strength Index is stable around 50.

The picture can be described as mixed.

Support awaits at 113.15 that supported USD/JPY in mid-December. Further down, 112.60 was a low point in November and also in September. The recent trough of 112.20 seen in December is next down the line. 111.80 worked as support in November and resistance in September. 111.40 was a swing low in late October.

113.70 capped the pair's advance in mid-December. 114.05 was a peak in November. 114.25 held USD/JPY down earlier that month. The 2018 high of 1.1455 is a critical upside cap.

USD/JPY Sentiment

The Fed may be slightly more hawkish than markets expect, at lease bond markets predicting rate moves. While this may push the greenback higher, a potential risk-off sentiment could limit the Dollar's gains against the yen. A lot depends on the reaction of the stock markets, which also depend on developments around trade. All in all, it's complicated.

The FXStreet forex poll of experts shows a bullish move in the short term but falls later on. The average levels have not moved that much from last week's forecasts. It seems that recent ranges have depressed expectations for significant movements.

Related Forecasts

- EUR/USD Forecast: Fed expected to hike and pause, sealing USD fate for Q1 2019

- GBP/USD Weekly Forecast: Fed outlook may save Sterling as Brexit Status Quo sings: “Down, down, deeper down”

- USD/CAD Forecast: Packed pre-Christmas week as the pair continues climbing

- AUD/USD Forecast: China still the center of the universe for the Aussie

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.