The inflationary delusion

|Major fiscal spending is expected to continue after the election, along with expectations that the Fed will continue to support the economy via its “unlimited” Quantitative Easing (QE) package. You know what this means, inflation! At least that’s what seems to be the consensus among the Wall Street elites and main stream financial media. To me it’s deja vu all over again. We have been here so many times since the Global Financial Crisis of 2008, with the same result, the Fed struggling to hit their 2% inflation target. That’s what made Jay Powell’s comment in August about letting inflation “run hot” so comical. The Fed hasn’t been able to hit their target for 12 years, but will now have the ability to let inflation run above the target they haven’t been able to hit? And bond “experts” are falling into the trap, yet again. But, certainly this time will be different, right?

Just because new “money” is entering the system, doesn’t mean inflation will rise. A lot of it depends on where that new money is being spent. When there are shocks to the system like the one we experienced in March, the economy slows, asset prices fall, and household incomes decline which means less tax revenue for the federal government. In order to avoid cuts in existing federal government programs, the Fed must finance the federal government’s spending by purchasing bonds in the open market (aka QE). A lot of new “money” that is created goes towards the funding of existing programs such as unemployment benefits, education, healthcare, military, etc. Because of this, QE is unlikely to generate inflation in consumer prices on a broad level. When QE finds its way directly into the hands of consumers, via helicopter money, then we are more likely to see inflation in the real economy. This was occurring until July 31st, with extra unemployment benefits, $1,200 stimulus checks, and new federal facilities being setup for business loans. Over the last few months there has been a rise of inflation, in line with consumers directly receiving money. However, this is more aid than stimulus, because the purpose of these temporary loans and payments is to help households and businesses weather the storm more than anything. And given the unprecedented amount of “stimulus” dispersed since March, the rise of inflation and inflation expectations is rather underwhelming.

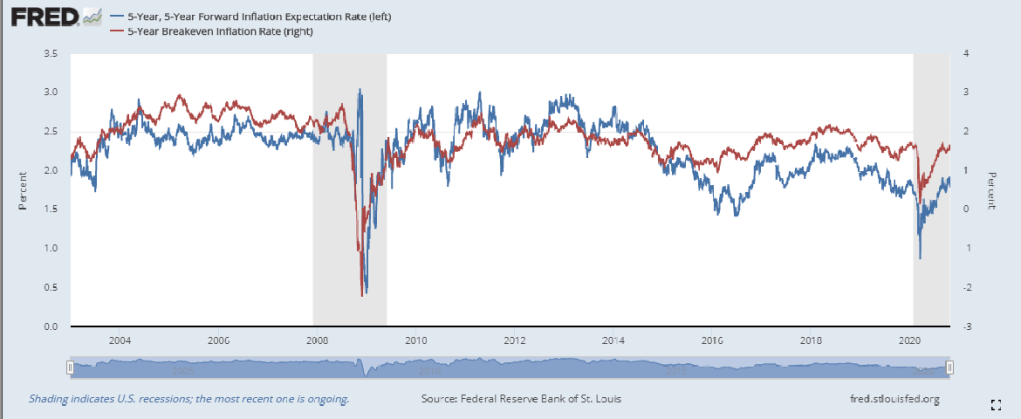

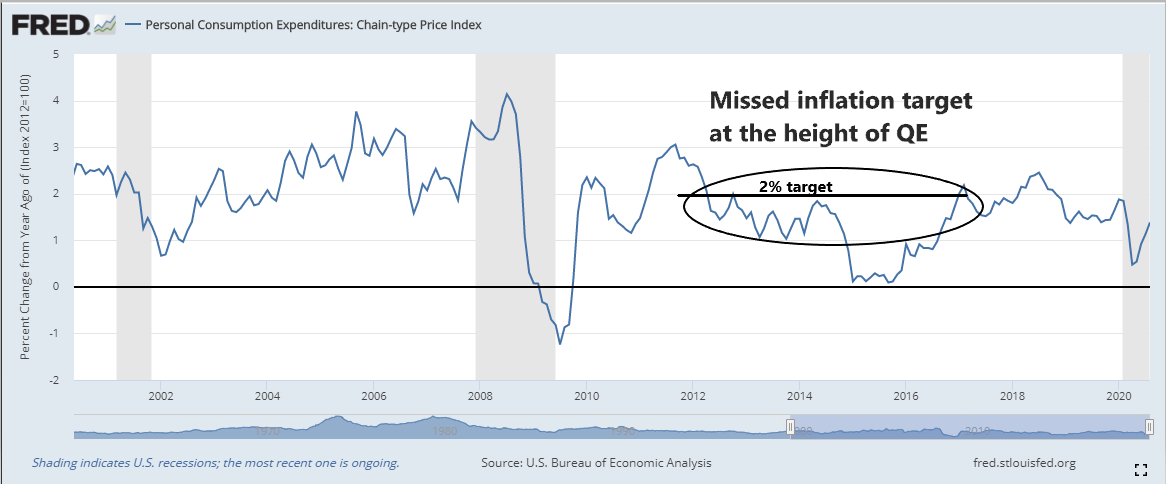

If we look (below) at the 5-year break-even inflation rate and the 5-year forward inflation expectation rate we can see the last time there was some sustained inflation at pre-2008 crisis levels was in the early post-recession years as the market believed that QE would work. However, if you look at the PCE (Personal Consumption Expenditure, 2nd chart below) you can see that the Fed failed to achieve their 2% target for most of that duration, which was at the height of QE. Seems that the market thought QE would work in generating inflation more than it was actually capable of doing.

{kind=link}

{kind=link}

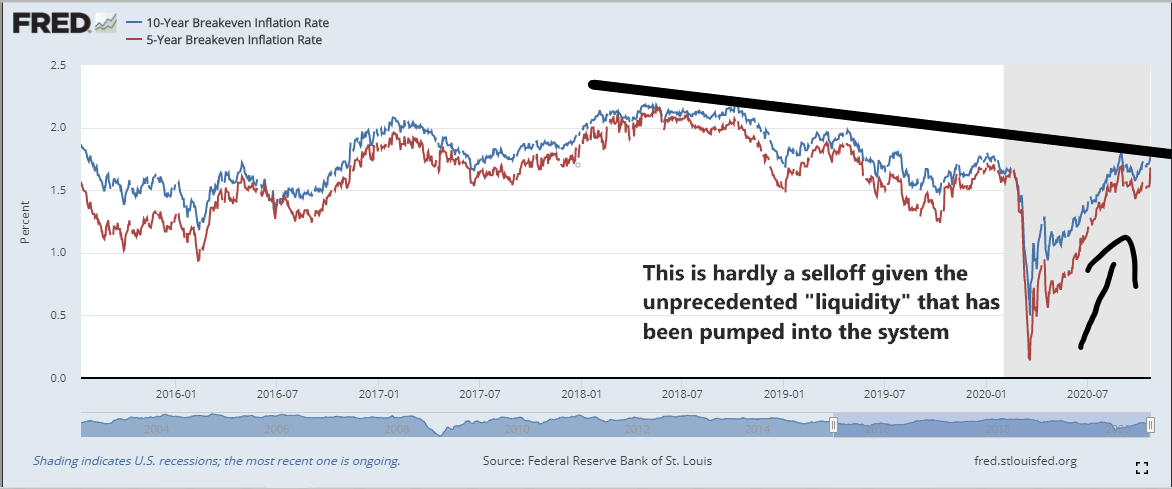

The last time there was this much talk about inflation being on the horizon was in 2017 going into 2018. About halfway through 2018 the unemployment rate fell below 4% for the first time since April of 2000. Many economic experts, including those at the Fed, believed this to be a “tight” labor market (it wasn’t as the participation rate said otherwise), indicating runaway inflation if there was no intervention. The Fed’s response was two rate hikes, one in September and another in December of 2018. Also, during 2018 the consensus among bond “experts” was that interest rates had nowhere to go but up and that a selloff in bond prices was imminent. Inflation, inflation expectations, and interest rates all peaked (above chart) in the middle of 2018, before beginning their descend, all the while the Fed was raising rates and the bond “experts” were calling for a massive correction in bond prices. They got it wrong, every which way you slice it. The Fed finally listened to what the bond market was telling them and began easing again in August of 2019 with its first of 5 rate cuts over the next 7 months. It was too late, because at this point they were just trying to undo the mess they made. Don’t forget, the stock market corrected 20% as a result of these poorly timed rate hikes at the end of 2018.

Now, here we are in 2020 with unprecedented amounts of “stimulus”, but with no changes from 2008. What I mean by ‘no changes’ is that the Fed is not doing anything differently than they have been since 2008, yet people are expecting different results? Fed is doing more QE. Nothing new. Federal Funds Rate is already at the ELB (effective lower bound). I suppose they could go negative, but you can ask Japan just how well that has worked. The Bank of Japan has forgotten how to spell inflation at this point. QE clearly doesn’t work, the bond market has been telling us that for about a decade now. Interest rates have been telling the Fed what to do, not the other way around which many believe is the case. But, here we are with Wall Street and the like, thinking, yet again, that rates have nowhere to go but up and inflation is coming. They will argue that the amount of “liquidity” that has been pumped into the economy via QE, with more on the horizon, will certainly generate inflation this time. I will argue the fact that the Fed has continuously had to use QE more and more and in bigger and bigger quantities proves that it hasn’t worked, it isn’t going to work, and has fallen short in everything it has tried to accomplish. The proof is right in the bond market.

{kind=link}

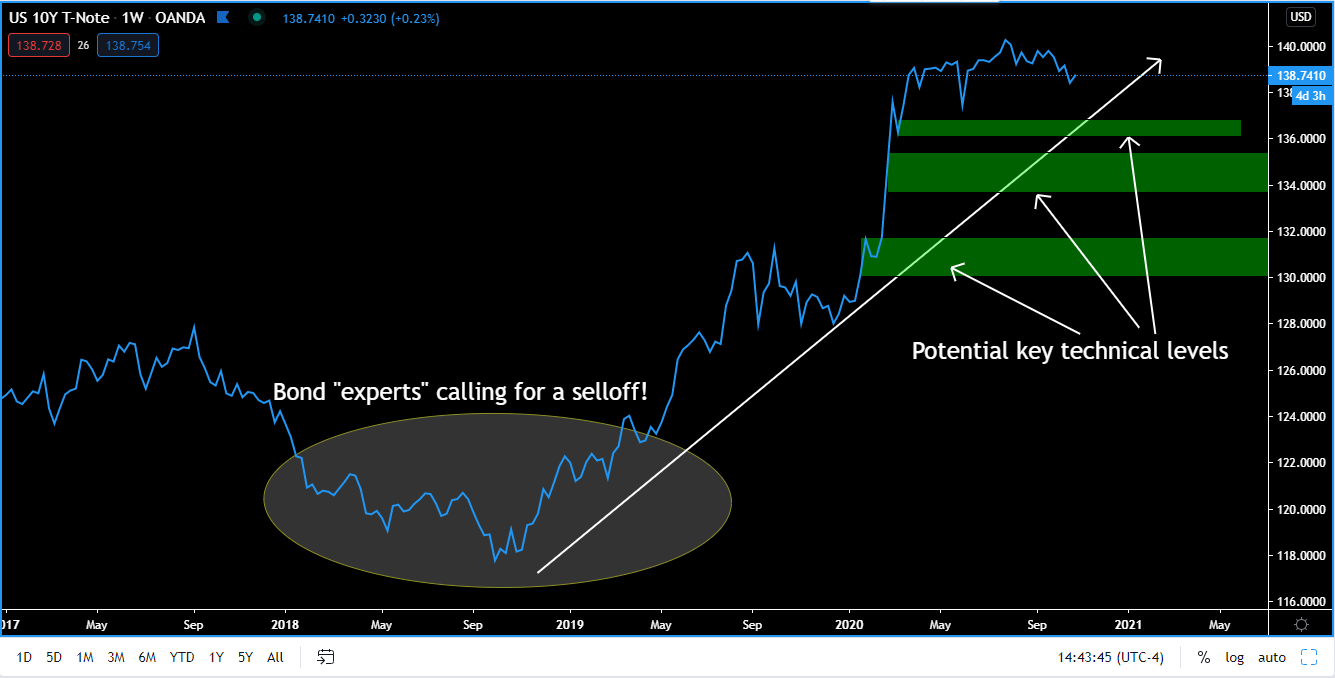

Take a look (below) at the 10-Year Note, and you can see just from 2018 what has happened in bond prices and thus yields. Despite bond “experts” predicting a collapse in bond prices, higher yields, and rising inflation—bond prices have risen and yields have fallen. This same phenomena took place shortly after the GFC as well. This isn’t anything new. But, again, here we are in 2020 with similar headlines and more predictions of higher yields and rising inflation. After the election there will likely be another large “stimulus” package. So, I wouldn’t be surprised if we see some short-term downside in bond prices and higher yields, as expectations of inflation rise. But, without some systemic changes, these moves will be short lived, as we have seen over the past decade. That is why I drew out a few key technical levels on the 10-Year Note which could trap some bond bears.

{kind=link}

Once inflation fails to sustain any of its upside momentum and bonds have their pullback and start to rise again, causing yields to fall, that would normally be detrimental for the local (US) currency. Capital flows where it is treated best – where it will receive the highest return. Now, this isn’t a US specific phenomena, the same things have been happening around the globe. Which means that, in the future, if things get rockier, capital is going to flow to where it is safest, sacrificing yield. I believe that the safest place will be the US, like we saw after the March meltdown. Capital will flow into the dollar and dollar-denominated assets, because despite things looking bleak in the US, they will likely be worse everywhere else.

If you are in the camp that government stimulus and QE is going to be successful this time around in generating inflation, just ask yourself a question: why is this time different than all of the others? I think if you do that you will come to the inevitable conclusion that it is not, and any moves up in rates will not be sustained. In the near-term, I think there will be some quality buying opportunities in the bond market as rates move higher, creating some false breakouts. Because, again, systemically nothing has changed and the tools being used by the Fed to generate inflation have failed for the past 12 years, and there is zero reason to think they will work this time around.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.