USD/JPY Forecast: Ready for another rise with US growth?

|- The USD/JPY continued marching higher amid mixed data and the Abe-Trump Summit.

- The upcoming week features the first read of US GDP and a rate decision in Japan.

- The technical picture is now outright bullish for the pair.

Mixed US data, Mixed geopolitical events

The third week of April had lots of action but little movement in the pair.

Optimistic Fed-speak: John Williams, the incoming President of the New York Fed, expressed optimism on reaching the inflation goal and about growth. He also dismissed worries about an inversion of the yield curve. Similar hawkishness was also voiced by other members such as Governor Lael Brainard, outgoing NY Fed President Bill Dudley and even Neel Kashkari, a dove, seemed less pessimistic.

Mixed US Data: US Retail Sales rose better than expected on the headline but a small downward revision in the Control Group took the sting out of that rise. On the other hand, both Building Permits and Housing Starts beat expectations and also continued advancing.

Trade not that optimistic: After the Trump Administration showed openness to returning to the Trans-Pacific Partnership (TPP) in the previous week, the President returned to his stance of favoring bilateral deals. In the summit with Japanese PM Abe, the differences were clear. Also, the rise in metal prices reminded markets that tariffs have implications and an outright trade war is still an option.

Progress on North Korea: CIA Director and the nominee for Secretary of State Mike Pompeo met North Korean leader Kim Jong-un in Pyongyang, preparing the Trump-Kim Summit. This is another step forward. Japan has some reservations, but the peace process continues.

Syria forgotten again: The week started with the echoes of the airstrikes on Syrian chemical installations. The action by the US, the UK, and France over the weekend did not see any reaction from Syria, Iran and Russia and no follow-through the West. Markets had time to digest the event before the open and then forget about it quickly.

All in all, it was a mixed bag of risk-on and risk-off while the data and the Fed provided reasons to buy the greenback. Nevertheless, the moves were relatively limited.

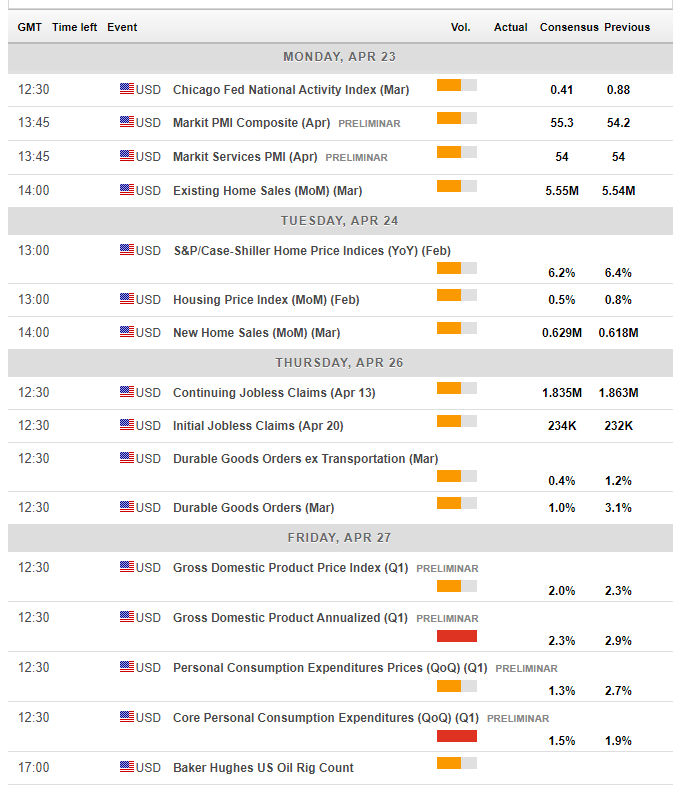

US events: Leading up to the GDP report

The last full week of April's highlight is the first release of US GDP for the first quarter of the year coming on Friday. In several of the past years, the first quarter has been weak, and 2018 will likely be no different. The annualized growth rate is expected to fall to 2.3% in the first estimate, that tends to have the most significant effect on markets. This would be a considerable slide from 2.9% seen in Q4 and levels above 3% in Q2 and Q3 of 2017. The GDP Now projections from the Atlanta Fed have been even weaker: around 2%.

The polar vortex and cold weather, in general, may be blamed for the weakness. Within the components of growth, markets focus on consumption and investment, which are positive contributors, while government spending and inventory buildup are frowned upon. A replenishing of inventories now may result in their depletion and detract from growth later on.

Before Friday's critical release, there are other data points of interest and some feed into the publication. Existing Home Sales are expected to remain almost unchanged at 5.55 million annualized in March, the last month of Q1. The release on Monday will be preceded by Markit's purchasing managers' indexes for April, which do not feed into Q1 but may still move markets.

Tuesday sees the New Home Sales figure. Most of the transactions in the real-estate market are of second-hand, existing homes. Nevertheless, the sales of new units trigger broader economic activity and go hand in hand with economic growth.

Durable Goods Orders on Thursday can already have a substantial impact on the GDP release. After a significant rise of 3.1% in February, headline orders are expected to rise by 1.0% in March. Core orders are even more critical as the Fed watches them carefully. After jumping by 1.2%, a more modest rise of 0.4% is on the cards. A meaningful deviation will reshape GDP forecasts.

As usual with the US, political developments may also have an impact. The US Dollar tends to suffer alongside Donald Trump's troubles and rise when trade tensions wane.

Here are the top US events as they appear on the forex calendar:

{kind=link}

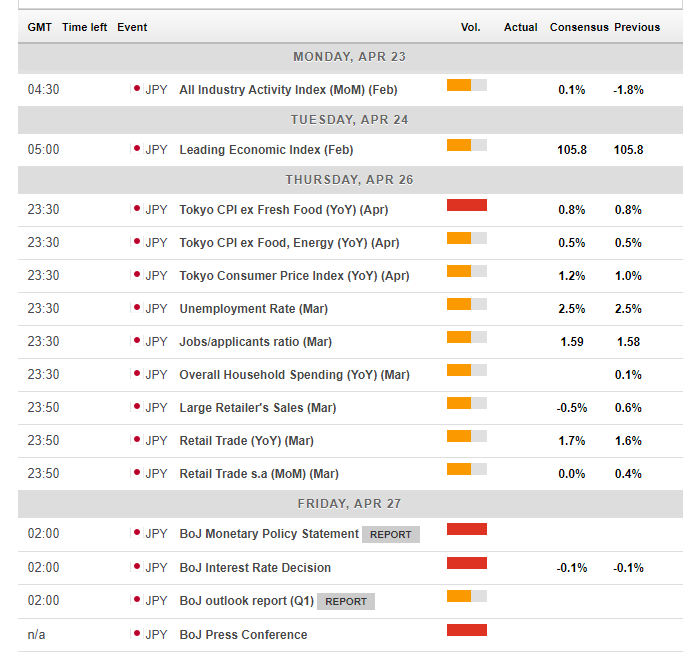

Japan: The BOJ, bad internal politics, and better external ones

The Japanese calendar features two prominent events. The release of the Tokyo Inflation report for April provides an early gauge of inflation. The number to watch is the Tokyo CPI ex Fresh Food. This core number is up only 0.8% YoY, far from the elusive target of 2%. A similar figure is likely now.

The second big event is the rate decision early on Friday. Haruhiko Kuroda celebrates five years at the helm of the Bank of Japan. His QQE program helped stimulate the economy and also sent the Yen lower. However, inflation remains low. Rate decisions are quite frequent in Japan, but this one is higher importance given the anniversary and the release of the BOJ Quarterly Outlook.

Kuroda and co. will likely leave the interest rate at -0.1% and continue pledge to buy bonds to keep the 10-year yield at 0%. Nevertheless, Kuroda may provide surprises in the wake of his second term. He has previously talked about beginning to remove the monetary stimulus in Fiscal Year 2019 which starts in one year from now. These relatively hawkish comments seemed premature, and Kuroda has not repeated them since. If he alludes to a future tightening, the Yen could rise. However, if further measures are introduced to lift inflation, the Yen has room to fall.

Japan's role as a safe-haven currency will also come into play. The progress on North Korea is pushing the pair higher as the safe-haven yen loses its shine. The next big event is the meeting of North Korean Leader Kim Jong-un and South Korea's President Moon Jae-in.

On the other hand, Japan's internal politics support the Yen. Prime Minister Shinzo Abe's approval rating continues falling, and according to some analysts, he may quit in a few months. Abe has spearheaded fiscal and also the monetary stimulus. His departure may halt these efforts.

Here are the events lined up in Japan:

{kind=link}

USD/JPY Technical Analysis: Ready to rise?

The week of consolidation allowed the pair to settle well above the 50-day Simple Moving Average and also see the RSI tick up. Momentum is somewhat lacking, but the general picture is bullish.

¥107.50 is a pivotal line after capping the pair in early April. It is followed by ¥107.80 which was a swing high on April 13th. Further up, we find ¥108.30, a level of support back in late January. The round number of ¥109.00 separates ranges early in the year and is a stepping stone toward the rounder number of ¥110.

¥107.00 worked as resistance in late March. Lower, ¥106.60 capped it earlier that month. The round number of ¥105.00 was a swing low, and the ¥104.63 level is the lowest since 2016.

What's next for USD/JPY?

The US Dollar has good reasons to rise: a bullish Fed, upbeat data, and increasing yields. This has not entirely played out in this pair. An ongoing loose monetary policy in Japan and an OK GDP may be enough to push the pair higher.

The FXStreet FX Poll shows a bullish sentiment in all the time frames. This is similar to the views expressed here.

More: Trading forex in Europe? This is what the new ESMA regulations mean for you

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.