Rising long-term interest rates: A relatively good point for the Eurozone

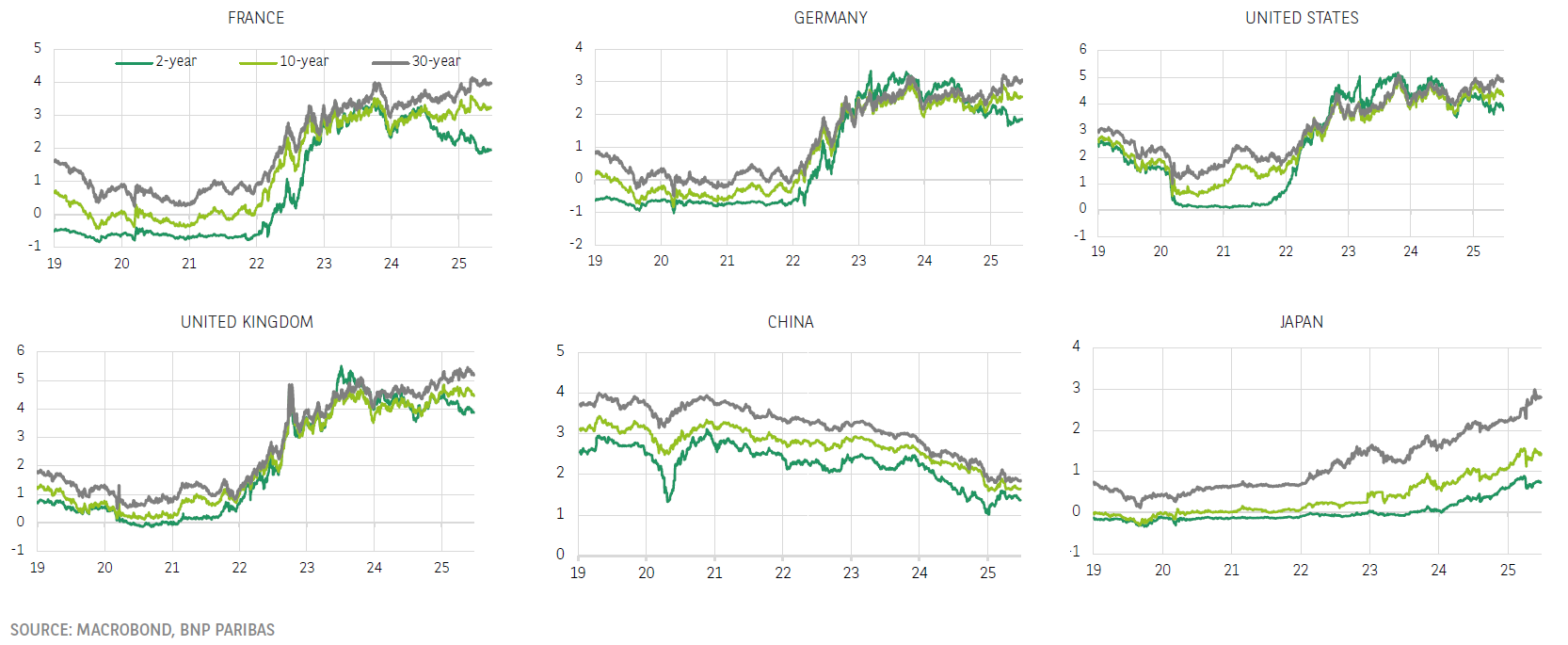

|The rise in interest rates seen in the advanced economies since the end of Covid has been continuing in scattered order. Long-term interest rates have generally been on the rise, but with significant divergences. The general situation of uncertainty and the undeniably upward trajectories of public debt in advanced countries are having negative repercussions on the bond markets, which are likely to have a similar impact on the financing of the economy.

Evolution of 2-year, 10-year, 30-year yields (%)

2-year rates are good indicators of current and future monetary policy. They have fallen sharply in the Eurozone, where disinflation is most advanced. The more erratic movements in the United States underline the consequences of uncertainties about the macroeconomic outlook and therefore about the Fed's rate path.

In terms of long-term rates, the Eurozone has been doing better than the United States and the United Kingdom

The 10-year rate is important as it is the benchmark rate, and because it is often close to the average maturity of public debt. The 30-year rate, on the other hand, reflects investors' expectations of debt sustainability. The 10-year rate has been broadly stable in the Eurozone over the past year, while the 30-year rate has risen moderately (the spread between the two is back to its pre-Covid level). Conversely, both have been rising in the United States and the United Kingdom. U.S. Treasuries are suffering from concerns about the United States' fiscal path, as illustrated by a number of failed auctions. The movement has been even more marked in the United Kingdom, against a backdrop of difficult fiscal consolidation. On the other hand, membership of the Eurozone seems to be protecting member countries with rising debt, such as France, from a sharper rise in long-term rates. This shows that markets are confident in the Eurozone and illustrates the benefit of being part of it.

Japan stands out on the negative side

Yields have been rising across the board, especially as maturities lengthen. Monetary policy is playing a role on all parts of the curve, with the gradual tightening of monetary policy, while the BoJ is gradually reducing its rate of securities purchases, projecting a halving between Q1 2024 and 2027 (to JPY 2.1 trn per month). At the same time, the stagflationary economic situation and the lack of any prospect of fiscal consolidation are not helping. As a result, the spread between the 10-year and the 30-year has reached an all-time high, a sign of deep-rooted concern over Japanese debt.

China offers an entirely different perspective, despite a high level of debt (close to 90% of GDP) that is continuing to grow

The dynamics underpinning its bond market (in particular the smaller presence of non-residents) and its economic environment are very specific: China is characterised by very low inflation and a bias towards monetary easing, two phenomena that are set to last in the short to medium term, hence the decline observed across all maturities and the moderate spread between short and long rates.

{kind=link}

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.